November 2021

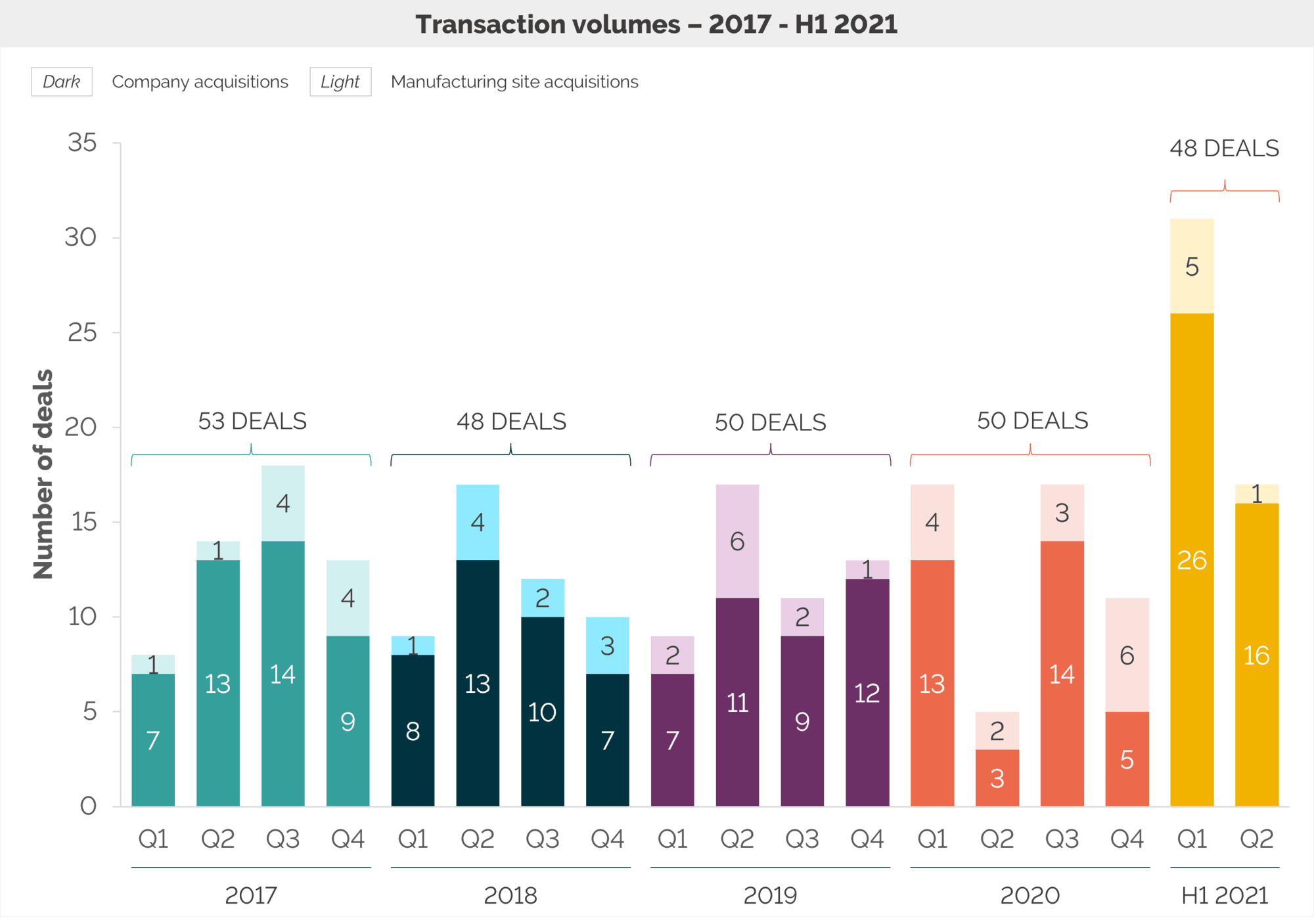

M&A activity in the CDMO sector has been steady over the past few years at around 50 transactions completed annually

Covid-19 had a noticeable impact on deal activity in Q2 of 2020, as companies needed to focus on the challenge of keeping manufacturing sites operational with the added pressure of increased demand from global health systems which left no bandwidth for corporate development activities

H1 2021 has been an exceptional start to the year. Q1 saw the highest level of deal activity recorded in any three-month period.

This was partly driven by deal backlog unwinding and partly by increased acquirer interest in the sector

Deal momentum has remained strong through the summer, and we do not expect to see a slowdown in M&A activity in the near-term

Source: Results Healthcare market analysis; Data based on majority acquisitions only – Does not include minority acquisitions, fundraises or acquisitions of pharma manufacturing facilitiesQ2 2021 transactions until 18th June

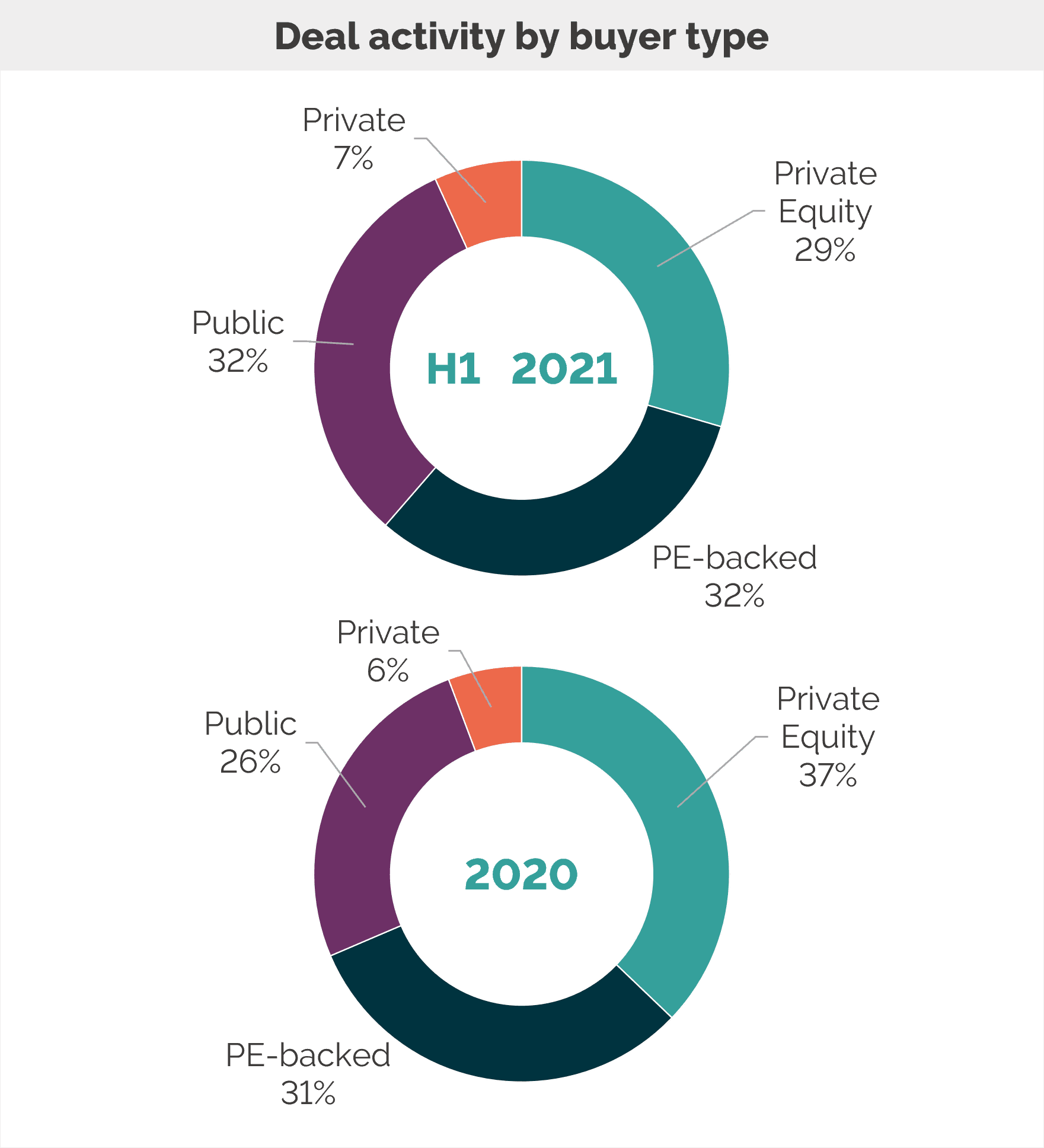

Deal activity in the CDMO sector is largely driven by private equity either through direct investments or portfolio companies that are pursuing a consolidation strategy

We are seeing a similar trend across the wider pharmaceutical services sector, as private equity continue to the view the space as an attractive investment proposition due to high margins, strong underlying market growth and higher barriers to entry

Private equity continue to sit on record levels of dry powder, which has been exasperated by the slow down of deal activity in 2020. Funds have been eager to deploy capital since debt markets recovered in Q3 2020 to bring their investment pace back on track

We expect investor interest to continue to increase as the pandemic has caused a ‘flight to quality’, with the pharmaceutical sector and manufacturing in particular viewed as a recession-proof segment with strong growth potential

Increasing financial investor activity over the past 5 years has been a significant driver of valuation multiple inflation through increased competition, especially for high quality, scale assets – Valuations in the CDMO sector are currently at record levels

Sources: Public data, CapitalIQ, Mergermarket. Mar-21 deals represent closed transactions to 04/03/2021

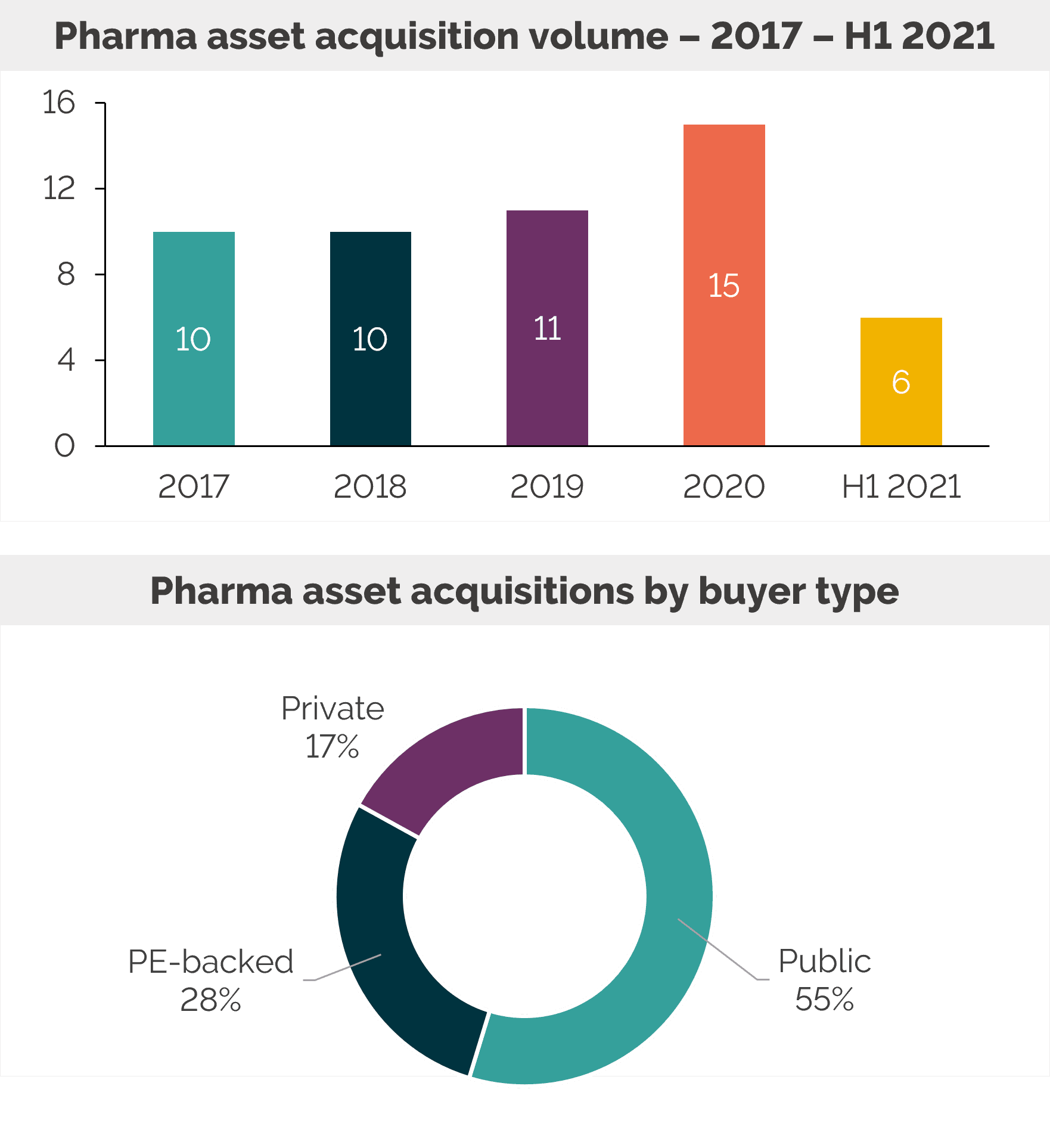

Pharma companies are continuing to divest manufacturing assets in an effort to reduce their networks and fixed cost base – Activity in 2021 to date has been broadly in line with previous years

2020 was a particularly strong year despite the pandemic, as pharma companies continued to push forward with their long-term corporate development strategies

In contrast to company acquisition, most pharma assets are being acquired by public CDMOs such as Catalent, Recipharm and Lonza that have been major consolidators in the sector for a number of years. Pharma companies view these companies as attractive acquirors due to their scale and robust balance sheets

Private CDMOs are also more strongly represented as pharma assets present an opportunity to acquire scale, capabilities and high-quality assets as at a lower upfront purchase price compared to corporate acquisitions

Sources: Public data, CapitalIQ, Mergermarket. Mfg = manufacturing.

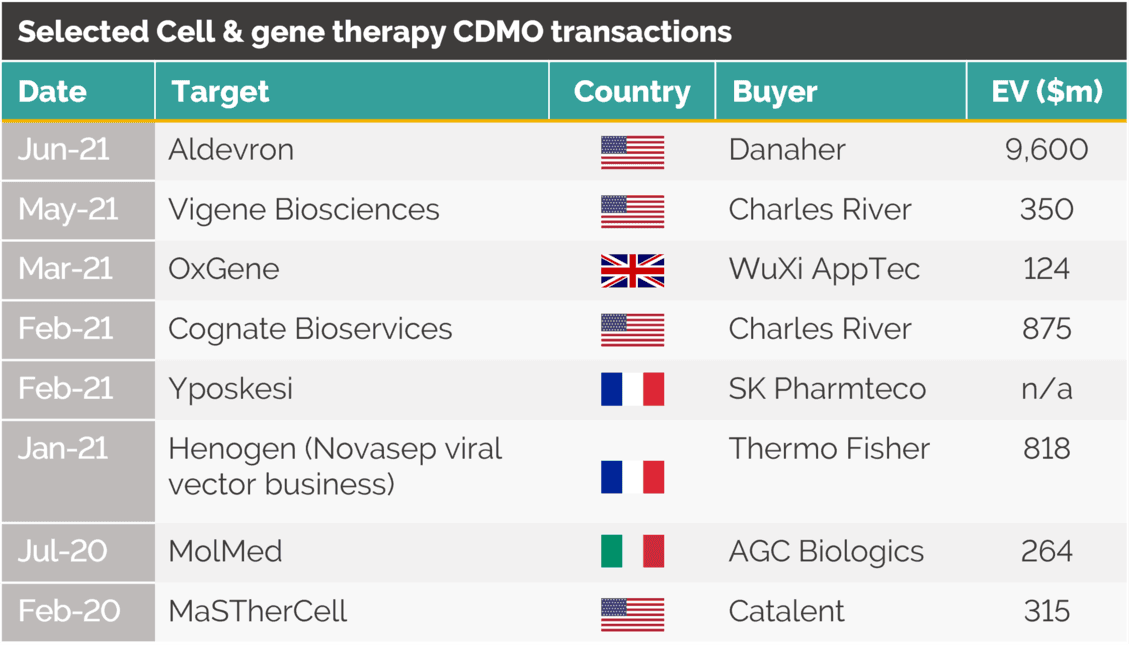

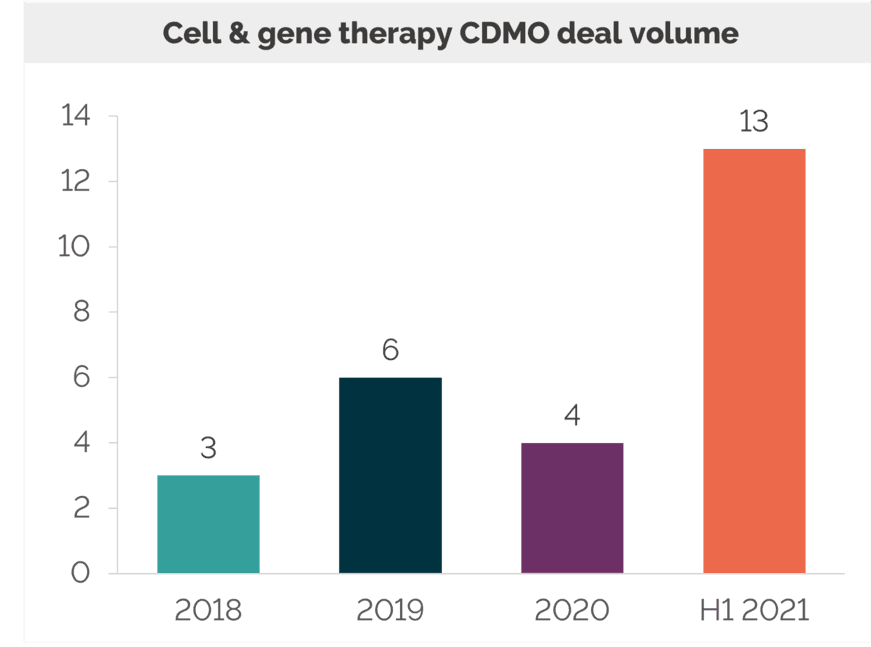

H1 2021 has been a bumper period for M&A in the cell & gene therapy space with as many acquisitions completed in the six months as in the previous three years combined – This activity is supplemented with heavy investments in organic expansion to satisfy capacity demands from customers

This is driven by the growing cell and gene therapy pipeline and increasing number of products that are moving into late-stage development and towards commercialisation. As a result, we expect the cell and gene therapy space to be the fast-growing CDMO segment over the coming years

We have also seen some significant recent activity in the materials supplier sector through the acquisitions of Sirion Biotech by Perkin Elmer and CellGenix by Sartorius

Sources: Public data, CapitalIQ, Mergermarket. Mfg = manufacturing

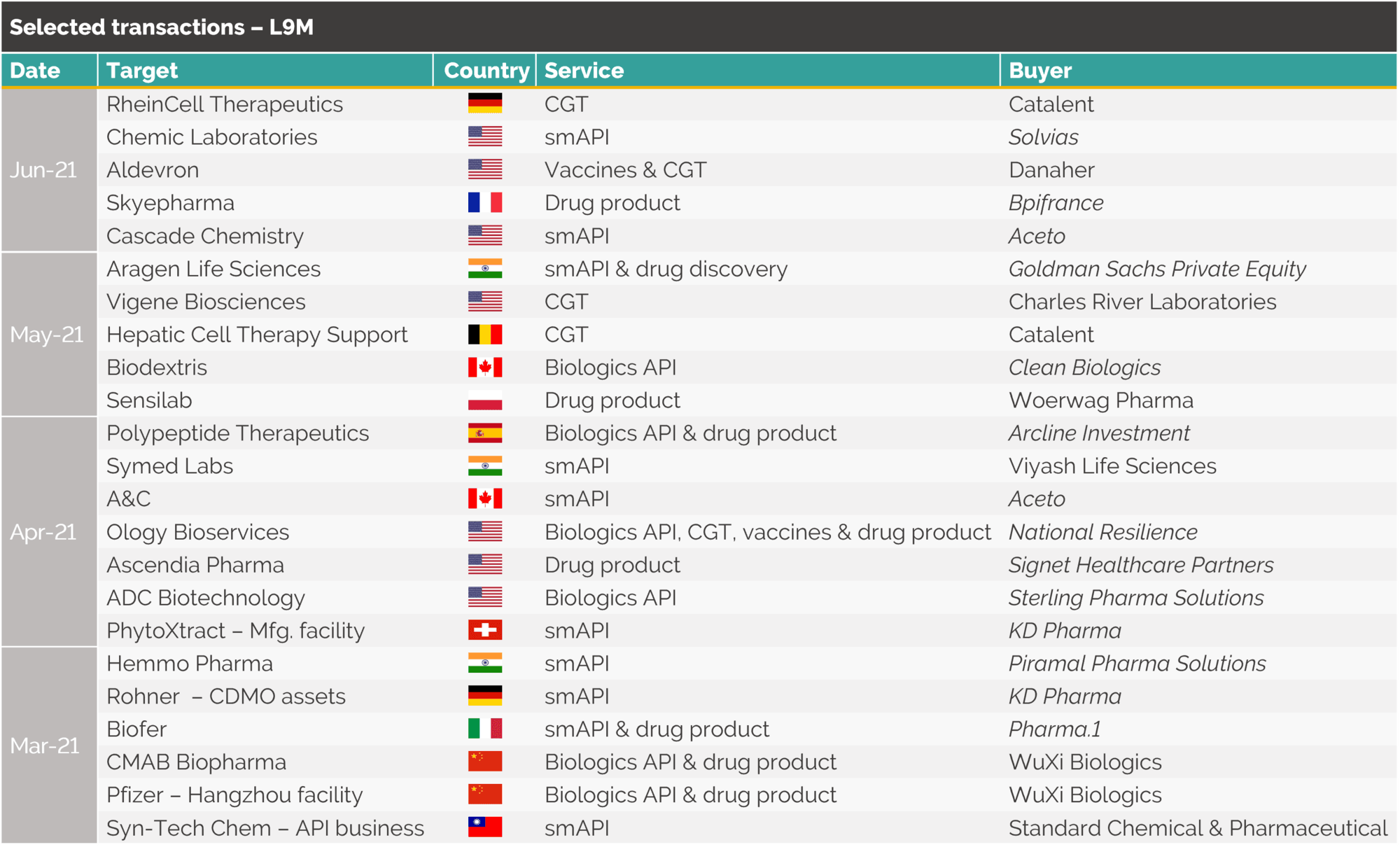

Deal activity during Q2 remained strong after the record-breaking volume in Q1

A standout deal was Danaher’s $9.6bn acquisition of Aldevron, a manufacturer of plasmids, mRNA and recombinant proteins

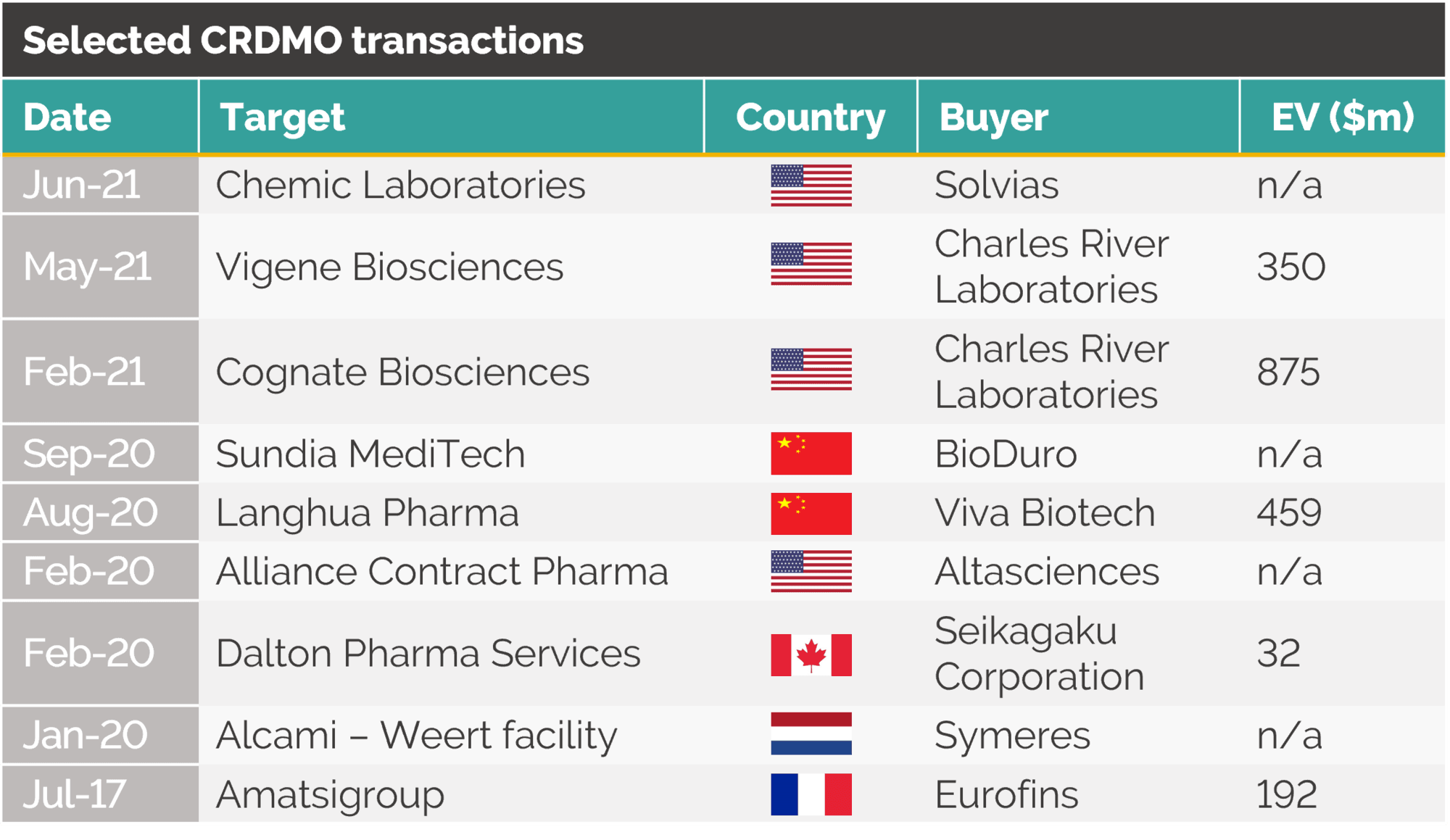

Companies in italics represent private equity firms or private equity-backed companies. Sources: Public data, CapitalIQ, Mergermarket

We recorded an extraordinary level of completed transactions during Q1 of this years

This was in part driven by the unwinding of deal backlog from 2020 and partly by increased buyer appetite

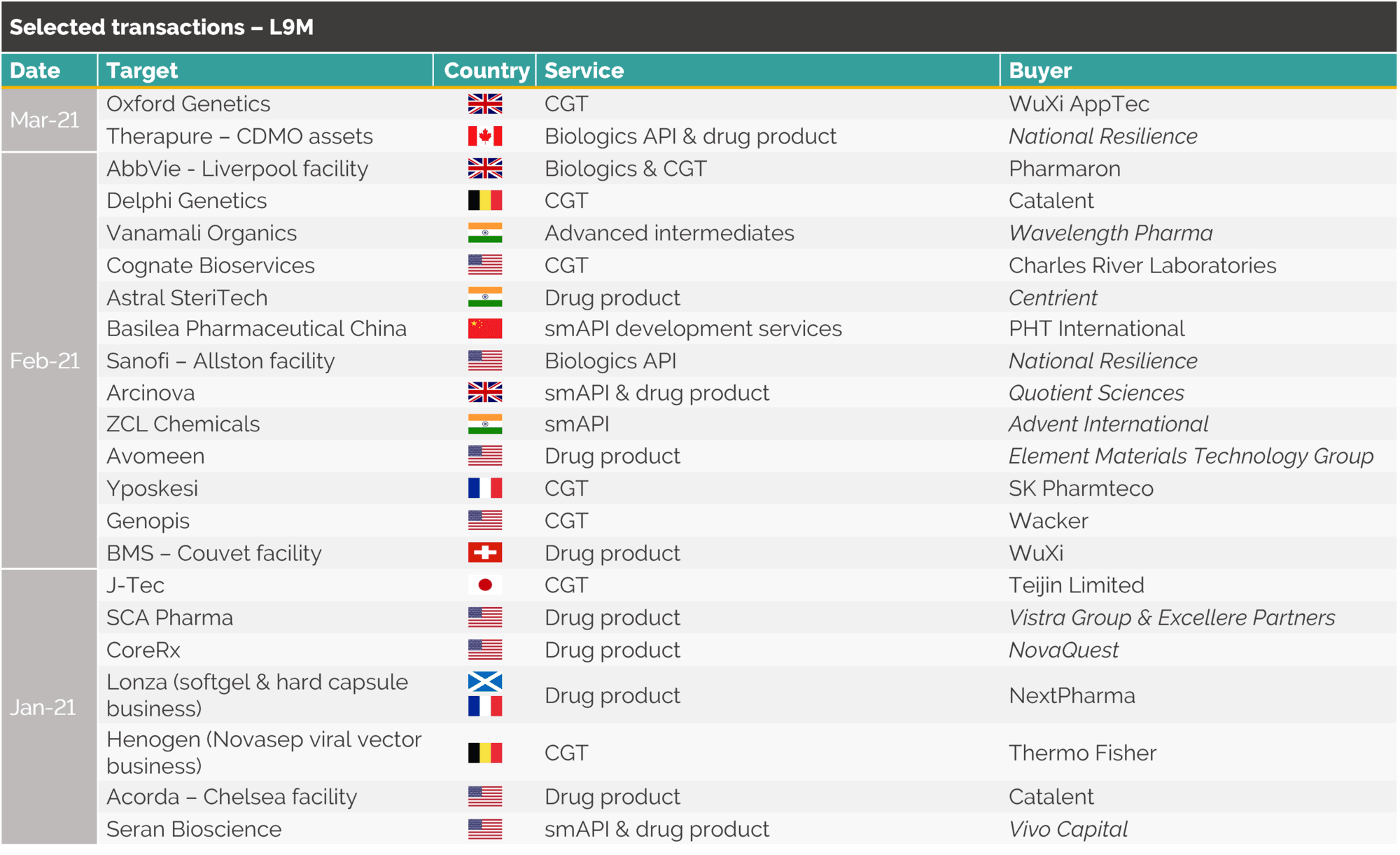

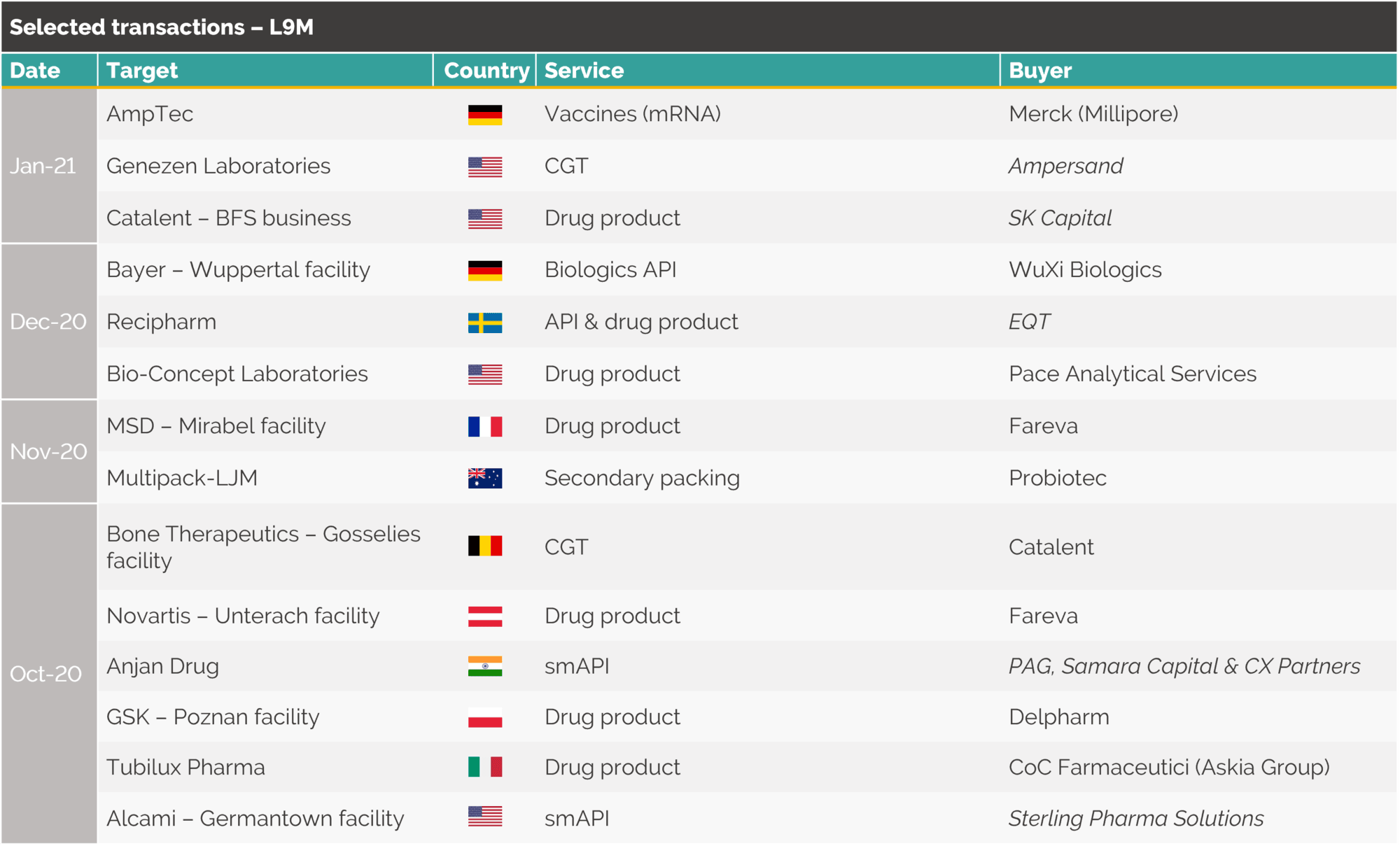

Cell and gene therapy manufacturer acquisitions in particular drove activity with a number of significant deals such as Yposkesi’s acquisition of SK Pharmteco and the spin-out of Henogen from Novasep

Deal activity had recovered in Q3, as it became apparent that - as an essential industry - pharmaceutical manufacturing would perform strongly through the pandemic and many transactions were already at a late stage in Q2 and could complete virtually and without much need for travel

However, Q4 saw another significant dip in activity, as many countries went back into lock-downs during the winter period

Although buyers have become increasingly comfortable with virtual processes, in-person diligence at manufacturing facilities remains a key component of CDMO transactions