November 2021

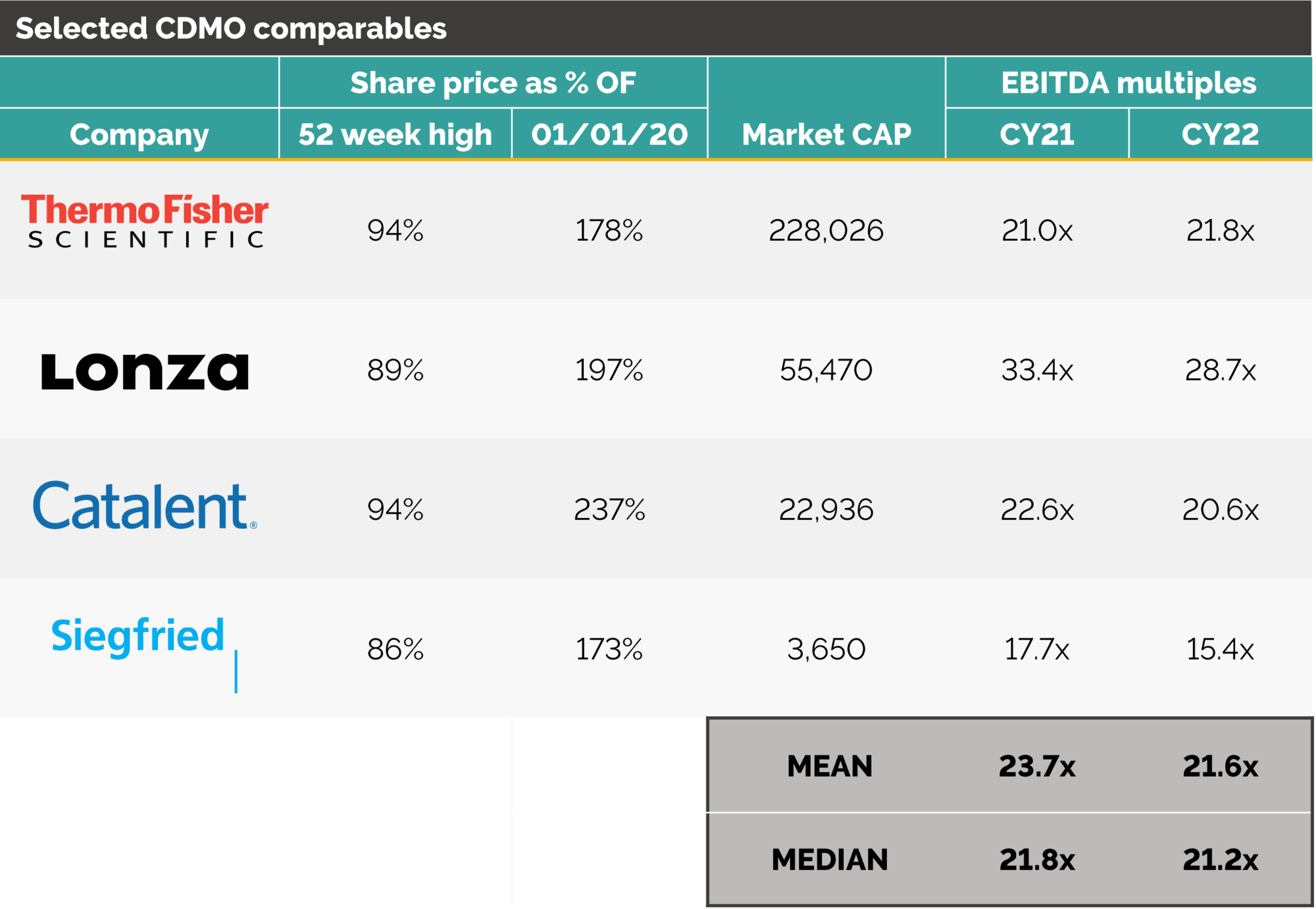

Sources: Public data, Capital IQ. Data calendarised to December YE. Enterprise value is in USD millions. Data accurate as at 30/09/2021

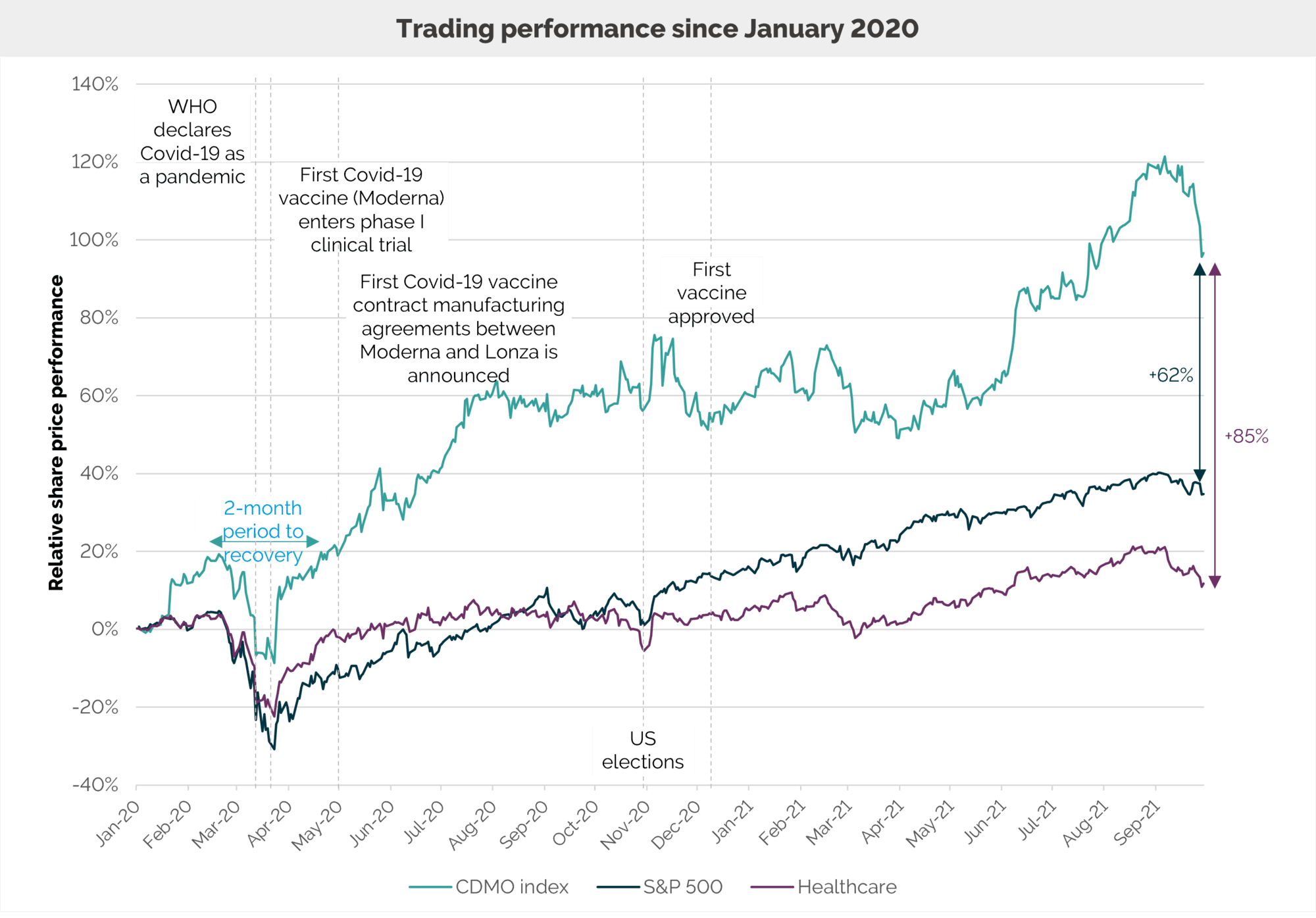

Sources: Public data, CapitalIQ. Data accurate from 01/01/2020 to 30/09/2021. Index starts at 100. Healthcare index is the MSCI European healthcare index. CDMO group contains the following companies: Lonza, Catalent, Siegfried and Thermo Fisher

Source: GlobalData. RBC capital markets, ResearchDive, IQVIA

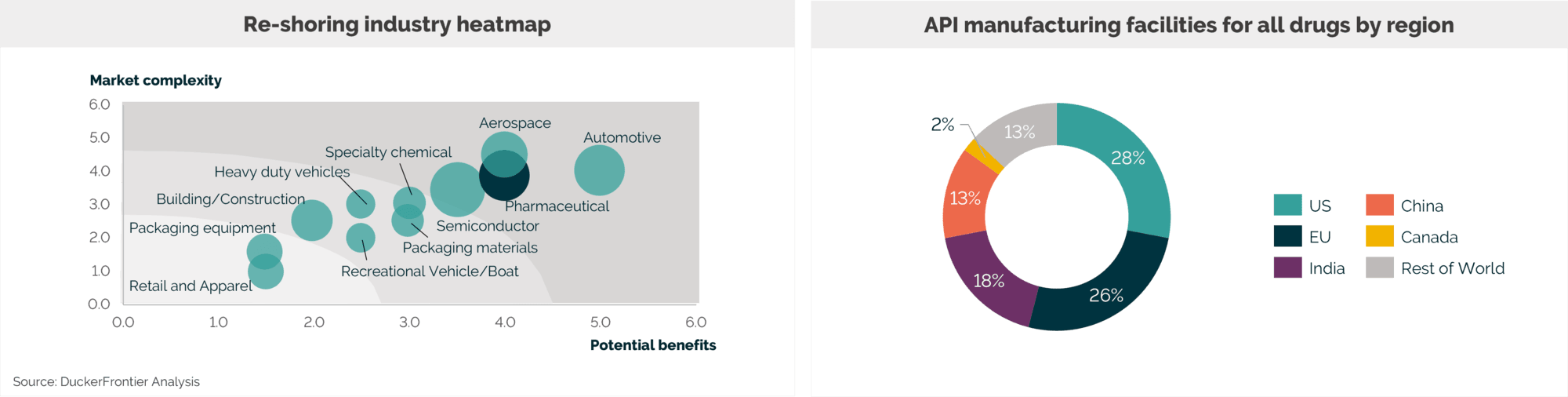

US and European pharma are considering ways to diversifying their supply chains, including reshoring of drug and ingredients manufacturing, in the light of drug shortages that have arisen from the pandemic.

Covid has been ultimately disruptive for many countries, such that they will need to recalibrate the delicate balance between onshoring and offshoring to maintain the autonomy and survive future crises

There have been a number of examples of companies in other industries that are making similar moves to bring their operations back to their home turf

These have tended to be mainly industries which are considered critical infrastructure and key resource sectors, which includes those that are healthcare and commodities related

In these sectors there has historically been a high degree of foreign sourcing and dependency on critical components and finished products

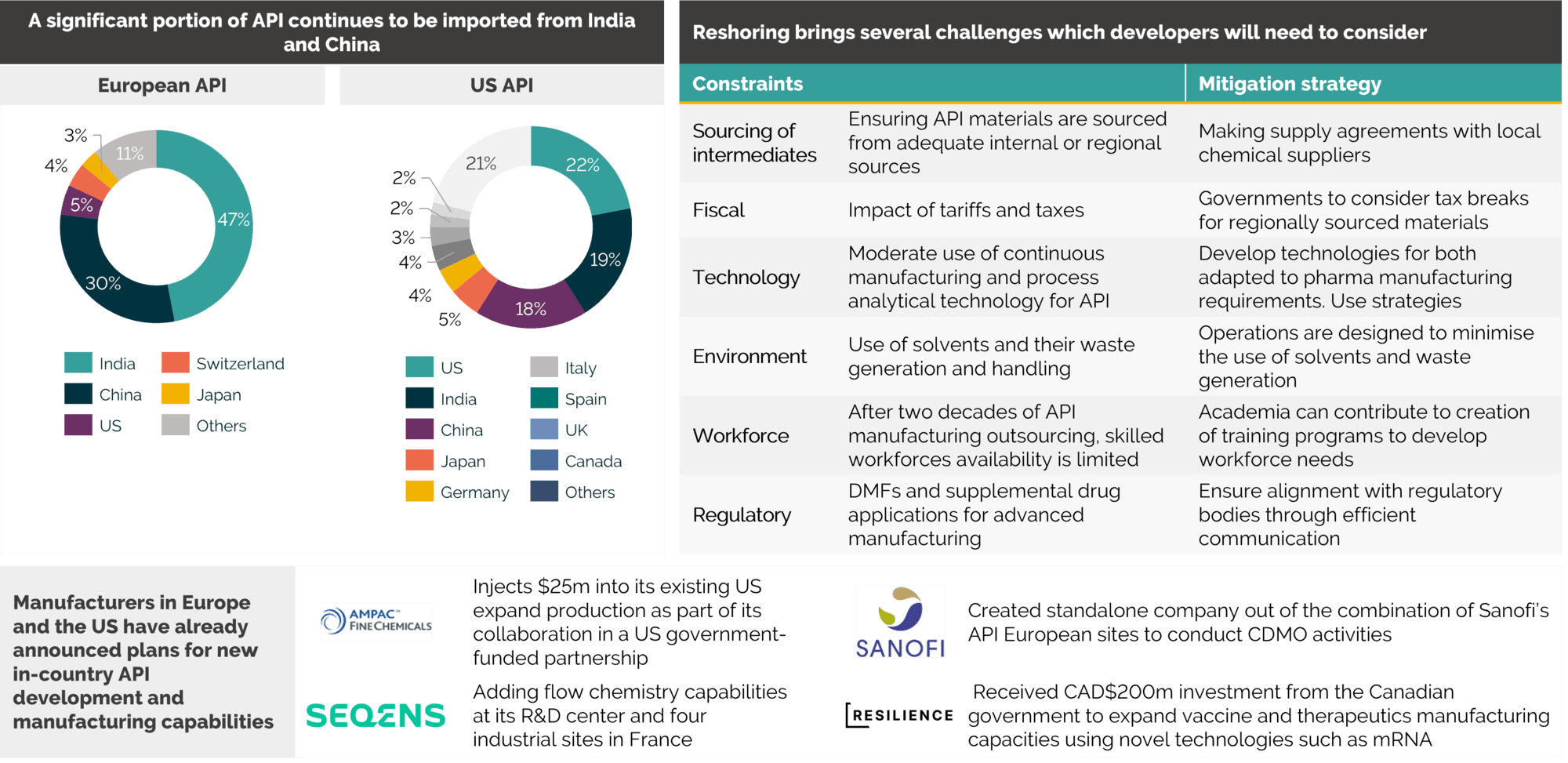

The US and Europe remain highly dependent for their sourcing of APIs with 41% and 77% respectively imported from India and China

We expect this shift to be reflected in the M&A market through greater demands and increases in valuation with respect to European and US site divestments and corporate sales, particularly for API sites and others where the technology is critical and in finite use

Source: PharmaTech.com, CHEManager

CDMOs have been uniquely positioned to address the challenges that drug developers have faced during the pandemic. The industry has proved itself as being defensive given the robust demand and performance that has been observed across the last 18 months

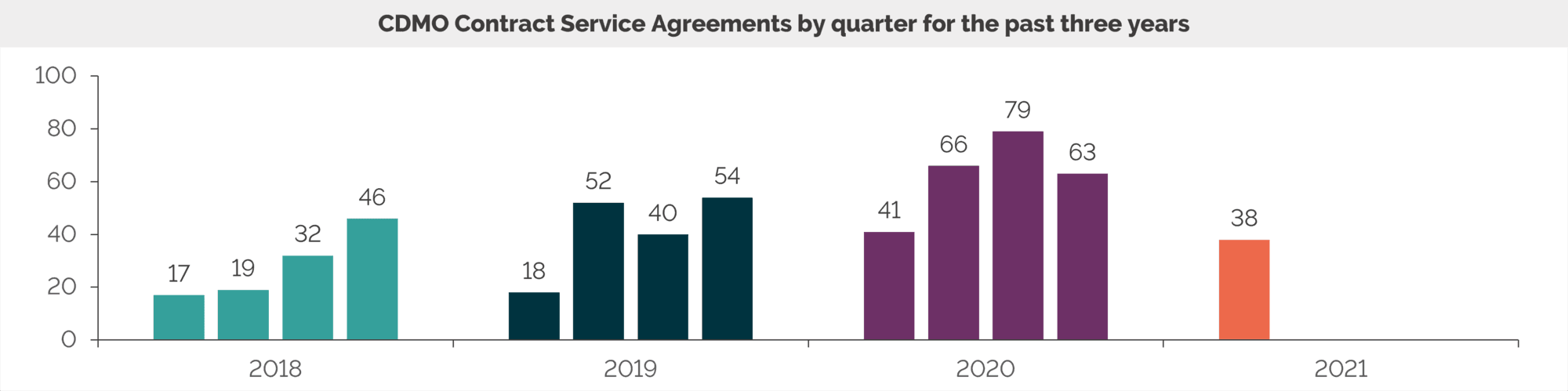

Market reports indicate that contract manufacturing has increased both in volume, as well as value, during the pandemic. The industry is facing greater shortages of staff and resources as the pandemic has exacerbated the short supply of single use products and devices

We estimated the total size of the global CDMO market at approximately $100bn in 2020 with an annual growth rate of 7.0% until 2023. Increased demand for vaccines and pharmaceuticals in general as a result of the pandemic is likely going to boost sector growth by 2-3% annually in the near-term and continue to drive the inflow of investment

Areas of particularly strong growth will include cell and gene therapies (viral vectors), injectable drug products, viral vaccines and highly potent API manufacturing

Given the increased buyer and investor appetite in the sector as a result of continually favourable fundamentals that have been further boosted by the pandemic, we see M&A activity remaining at the current high levels with valuations likely to stay near all-time highs

There is still ample scope for consolidation in the sector as the market remains highly fragmented with approximately 70% of CDMOs generating less than $50m revenue

Private equity will continue to be a major driver of M&A activity, both through new investments and the increasing number of growth platforms they back

We expect that global pharma will continue to evaluate their global supply chains and in-house manufacturing networks, leading to future opportunities for high-quality pharma manufacturing asset acquisitions