March 2021

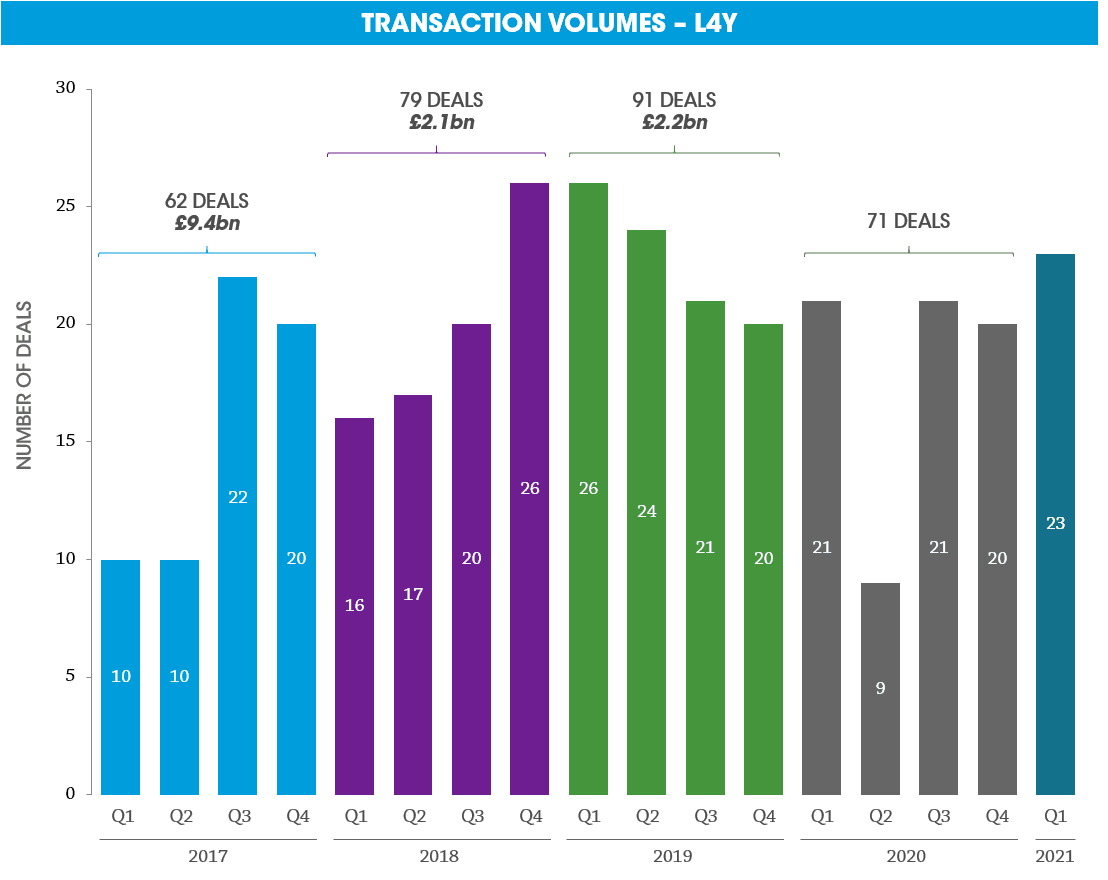

The level of impact that C-19 has had on M&A activity is comparable to that of the Great Financial Crisis, however, the rebound has been notably stronger. In the last year c.70 deals completed with a significant contribution from the second half of the year

There was a meaningful drop-in activity in Q2 which was driven by the need for buyers to focus on internal priorities in the wake of the pandemic and was further challenged by travel restrictions, impeding deal processes

This trend reversed in Q3 as buyers were in a better position to assess the impact that the pandemic had on target companies and they became more accustomed to diligence businesses virtually

2021 has gotten off to a strong start, with 23 deals completed by the first week of March, signalling a likely strong Q1 performance

Sources: Results analysis, CapitalIQ, Mergermarket. Q1-21 deals only until 03/03/2021

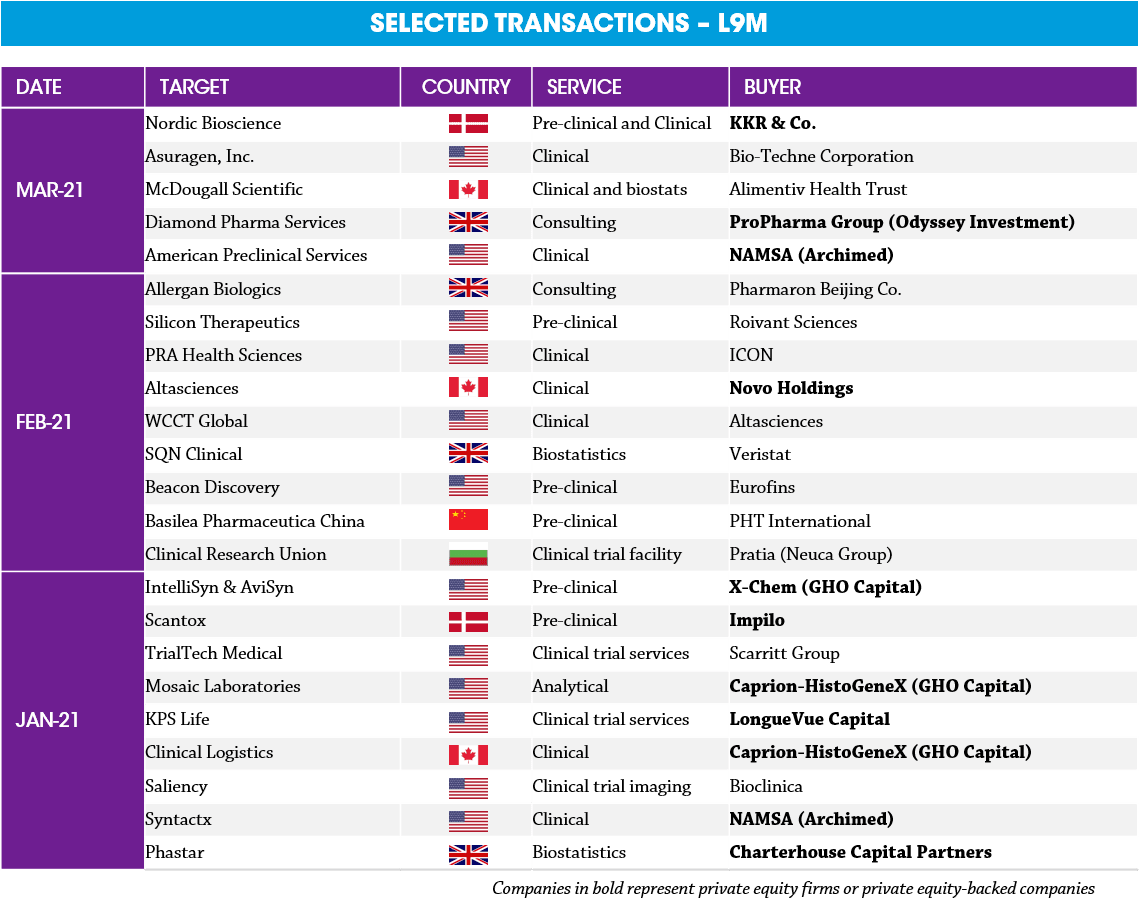

Deal activity in the past 9 months has continued to be dominated by private equity buyers and medium-sized CRO with stable cashflows and healthy balance sheets

There has been a notable scarcity of larger deals for the most part of the last 6 months, until recently

At the end of February, ICON acquired PRA in a $12bn move which is designed to address the growing market demand for de-centralised and hybrid trial solutions. ICON paid a 30% premium to PRA’s share price days prior to the bid

Sources: Public data, CapitalIQ, Mergermarket. Mar-21 deals represent closed transactions to 04/03/2021

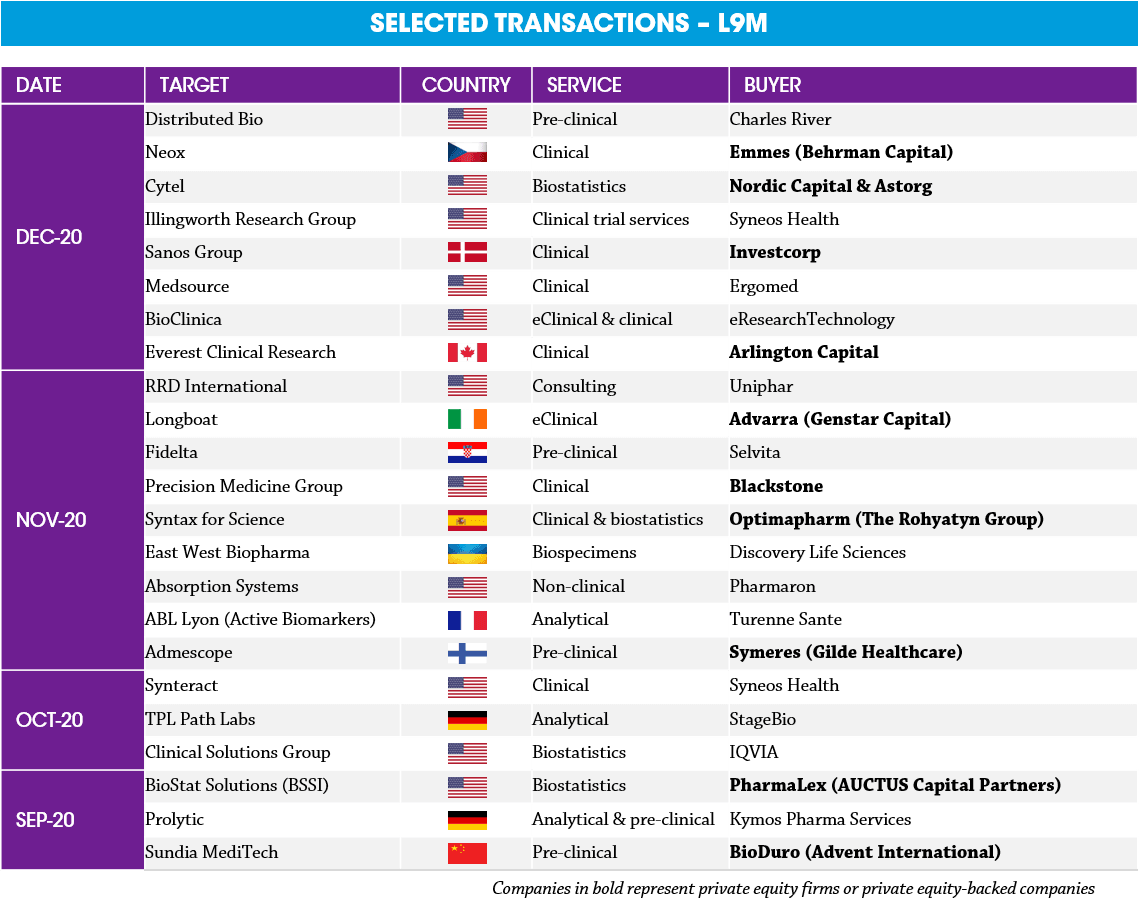

Private equity firms have been eager to deploy capital after the debt markets recovered at the beginning of Q3 2020. Out of the c.50 transaction completed over the past 9 months half have involved PE buyers

In November 2020, Blackstone completed its investment into Precision for Medicine for a reported $2.8bn. The investment is intended to help fuel PMG’s global footprint and technical capabilities

Sources: Public data, CapitalIQ, Mergermarket Mfg = manufacturing.

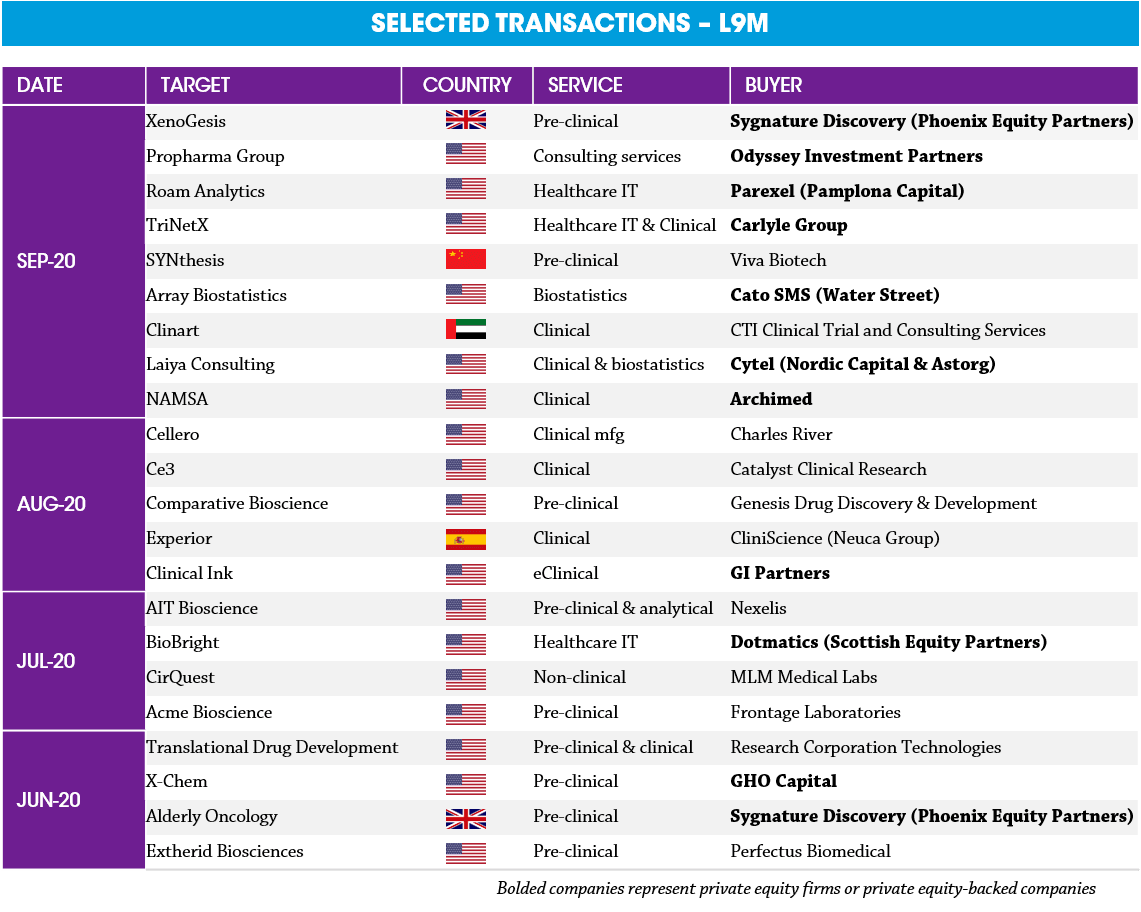

Sources: Public data, CapitalIQ, Mergermarket Mfg = manufacturing