June 2020

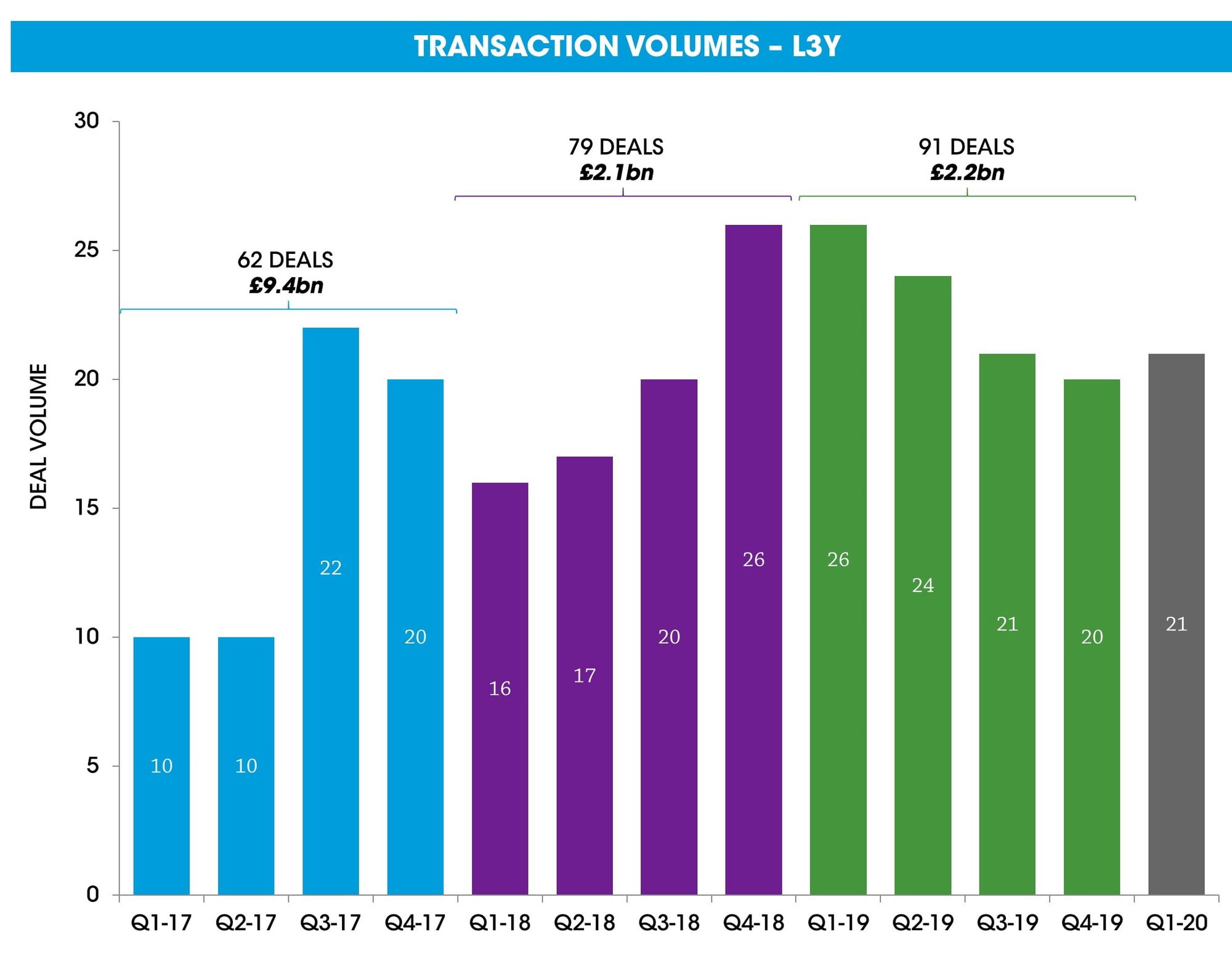

Deal activity in 2019 experienced a marked pick-up in volumes increasing to 91 compared to 2018 (79) and 2017 (62)

Notably there continues to be the absence of any large-scale transactions that occurred in the 2015-17 period

Deal volume in Q1 20 remains broadly in-line with the average over the same period in the last two years

Deals that completed in Q1 are likely to have been well progressed and therefore less impacted by COVID-19 before closing

Sources: Results proprietary knowledge, Public data, CapitalIQ, Mergermarket

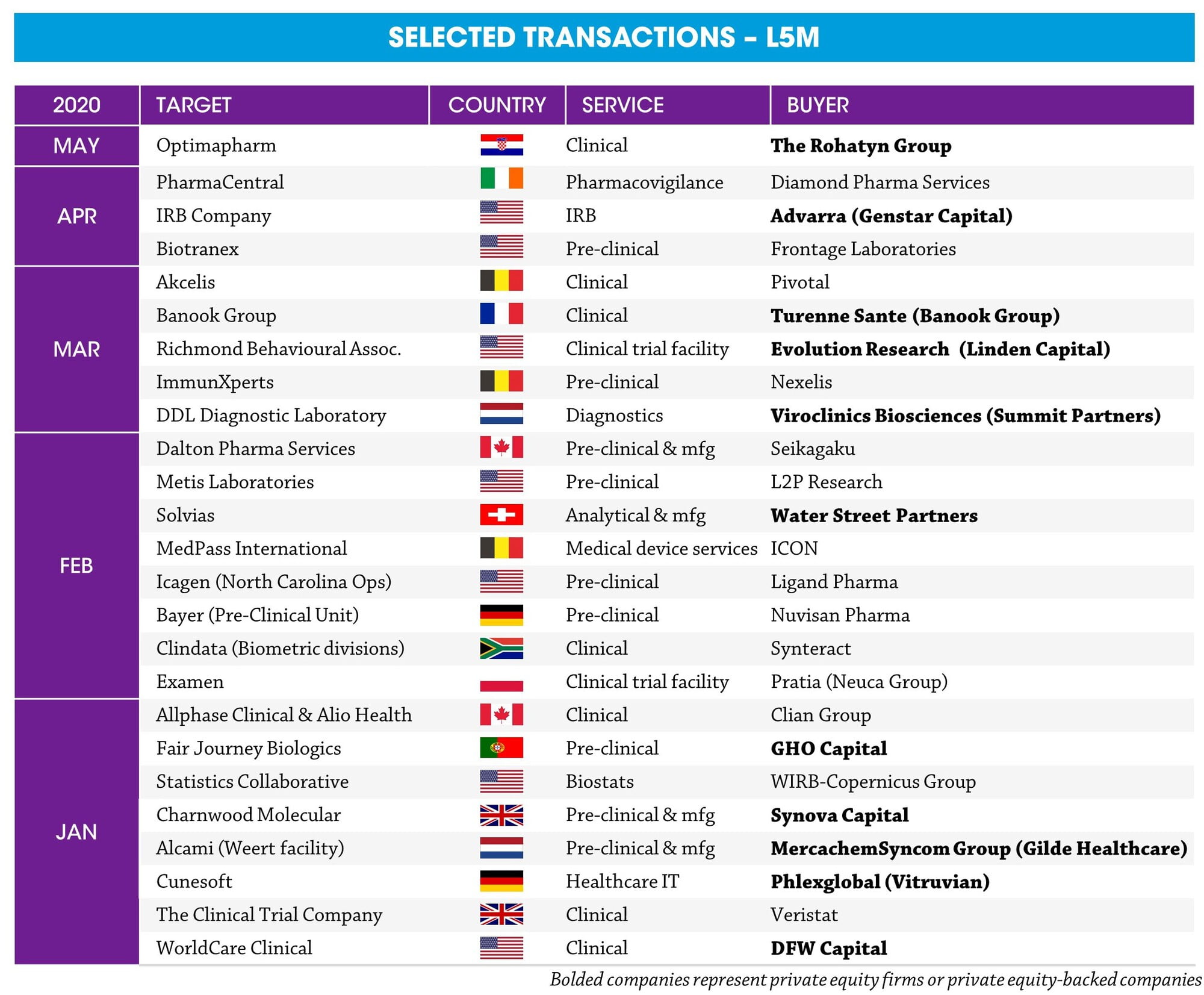

CRO M&A activity began to taper-off after February. Deals are still getting past the line but in much fewer numbers

Several notable processes which are in the early stages have stalled as parties wait to assess the impact of COVID-19 before launching processes (after the summer) and buyer wait for the financing markets to return back to normality

Deal activity has been dominated by medium-sized CROs and private equity buyers acquiring a mixture of clinical and pre-clinical assets in western markets

Sources: Public data, CapitalIQ, Mergermarket Mfg = manufacturing.