The global generic pharma market has experienced robust deal activity over the last 18 months to the end of 2019 but is now contending with the COVID-19 crisis which has had an immediate and unprecedented impact on health systems. It is yet unclear what the long-term general impact on generic drug usage will be, but generic drugs and generic companies will continue to be important, providing effective treatments for patients through and beyond the pandemic. M&A and wider deal activity in this sector is expected to continue at pace, reflecting recent trends.

Recent M&A deal activity has involved a broad spectrum of industry participants ranging from big pharma multinationals, non-profit organisations and smaller companies with more limited product offerings or distribution capabilities. Companies have been undertaking a slew of spin-offs, acquisitions, and divestitures with transaction values in the billions of dollars during this period, with corporate activity being driven by the desire to capitalise on the increasingly large bonanza available in the generic pharma market, and the need to react to the market dynamics and forces impinging on the segment. The large market bonanza is being fuelled by a flurry of branded drugs losing their exclusivity and underpinned by an aging demographic that is spending more on healthcare.

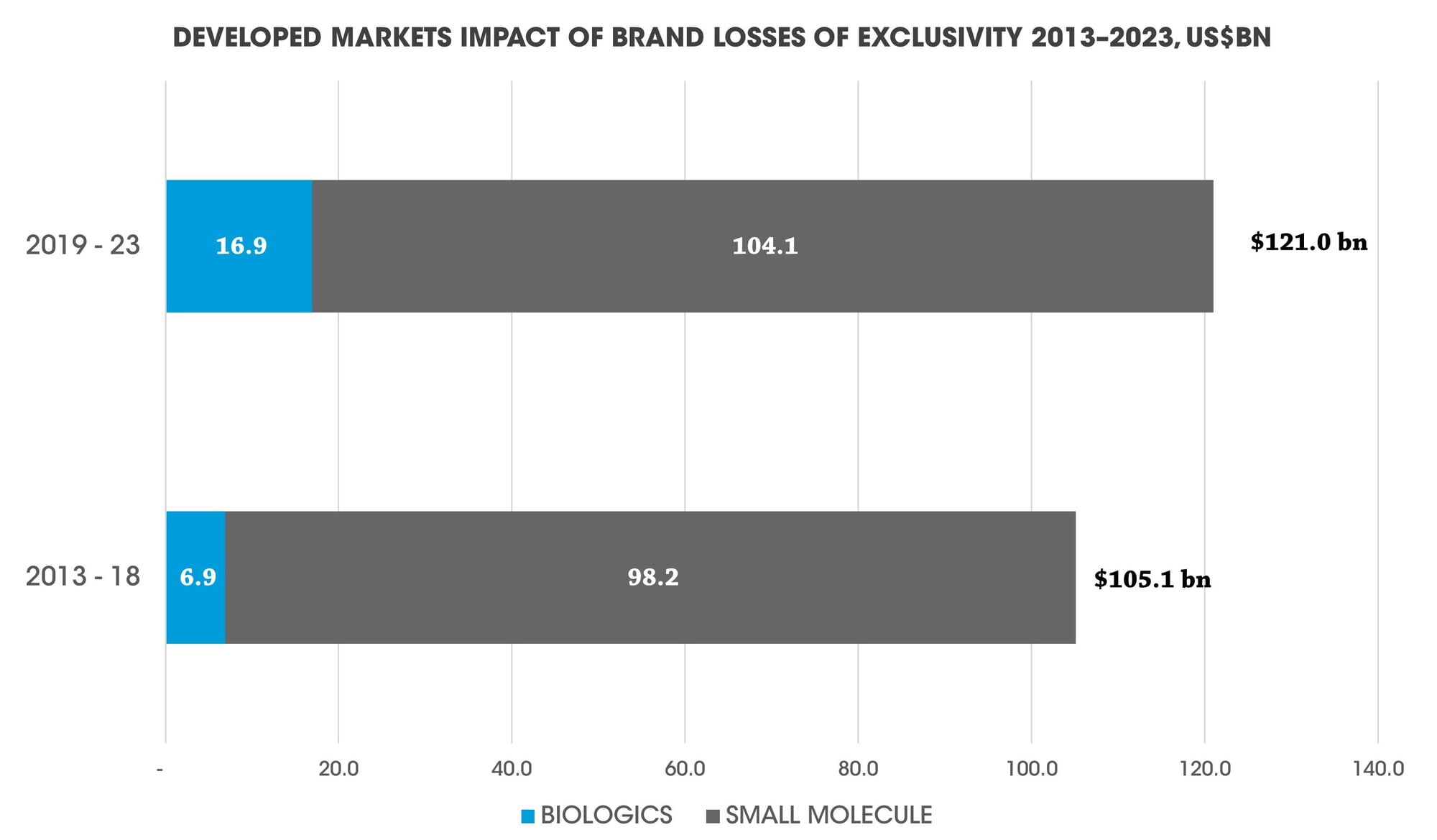

For developed markets, between the period 2013 - 2018, there was a loss of exclusivity for branded drugs amounting to $105bn. In the years ahead, the opportunity for generics is expected to become greater with the brand loss of exclusivity increasing further to $121bn for the period 2019 – 2023, of which the US market constitutes almost $95bn in value.

Figure 1: Developed Markets Impact of Brand Losses of Exclusivity 2013–2022, US$Bn. Source: IQVIA Market Prognosis, Oct 2018; IQVIA Institute, Dec 2018

The market dynamics acting on the generics segment are multi-faceted but an overarching theme over the years has been the downward price pressure on generic drugs.

Healthcare payors and purchasing organisations have been squeezing generics prices in order to rein in healthcare budgets – for example, the Chinese collective purchasing efforts have really weakened producer pricing power and resulted in significant price concessions, while in the US, pharmacies have been working with wholesalers to achieve the same. Also, the generic market structure is characterised by very many generic market participants competing to obtain market share, and in a ‘freeish’ generic market, the theoretical end result is price erosion. Needless to say, within generics, the commodity type products naturally face the most challenging environment, while the situation is more defensible for products with greater complexity or those offering some barriers to entry.

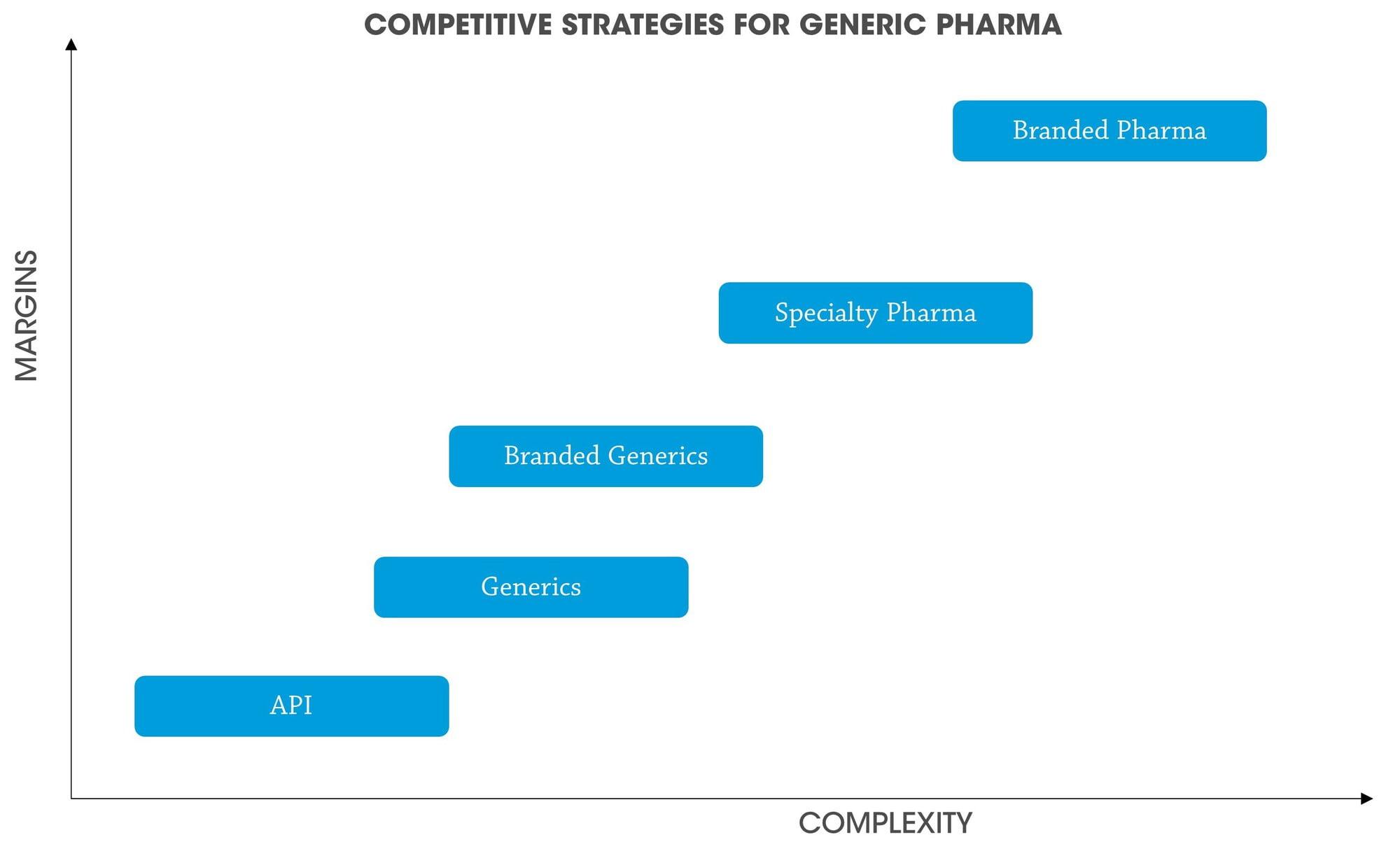

Faced with the prospect of further price erosion and margin loss which inevitably results in lower shareholder value, companies are constantly examining their strategies in order to achieve the twin objectives of optimising their competitive advantages and maximising shareholder returns. So, what options are available to optimise competitive advantage?

In a spectrum consisting of pureplay API manufacturers on one end and branded pharma/biotech on the other, companies can choose to deliberately narrow the scope by gaining further scale within their existing product offering, or trying to enter adjacent spaces and attempt to introduce greater complexity or intellectual property into their product offering.

So, what options are available to optimise competitive advantage?

Once companies have selected an optimal strategy to pursue, they have the option to pursue them either organically or inorganically. Organic measures include investing capital expenditures to build economies of scale, moving up the complexity spectrum by investing further into R&D programs or choosing to be the first to file and first to market for paragraph (IV) products. Companies that have multiple offerings straddling the spectrum may review if their product bundling or vertical integration strategy is beneficial and if shareholders are obtaining the desired valuation or suffering from a conglomerate discount. From an inorganic standpoint, corporate chieftains can attempt to restore margins by using M&A strategies to achieve cost and revenue synergies.

Figure 2: Competitive Strategies for Generic Pharma

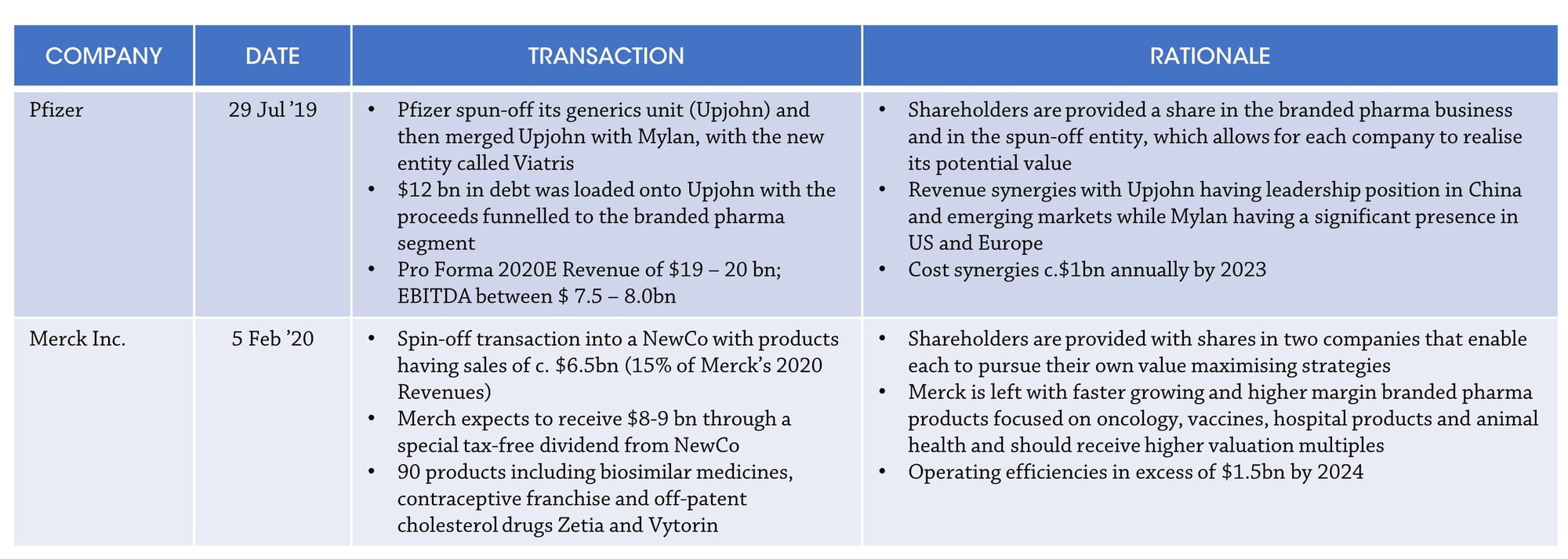

When reviewing transactions in the generics segment over the past 18 months, several observations can be made. Firstly, many well-known pharma companies with both branded pharma and generics/OTC portfolios undertook transactions to strategically separate the lower margin and slower growing generics/OTC portfolio from the higher margin branded pharma portfolio. These included companies such as Merck, Pfizer, Takeda, Esteve and Grupo Ferrer, who all clearly articulated their focus on the higher margin branded pharma business and separated the non-core segments either by selling or spinning-off the said assets.

Although both selling or spinning-off options result in the business segments being separated, the impact to shareholders may be different. A sale of the assets is generally a quicker and more straightforward process, but the seller is liable for Capital Gains Tax. In situations where a company may be able to affect a spin-off, the transaction can be structured as a tax-free distribution to shareholders where the shareholder receives new shares in the spun-off entity in addition to keeping hold of their original company shares. Frequently, the spun-off entity goes on to flourish as it can use its capital structure to grow its business, thus providing shareholders with a share that appreciates in value.

For example, Pfizer recently separated its riskier branded pharma business from Upjohn, its slower growing but stable generics unit. The deal was structured such that the branded pharma business received about $12 billion of cash from debt that was loaded onto the Upjohn spinoff before the spun-off entity was merged with Mylan, with the new entity branded as Viatris.

In theory, this looks like a win-win situation for Pfizer shareholders as the branded pharma business is well capitalised for growth while Viatris will be able to realize synergies from the merger with Mylan and use its large cash flows to deleverage and grow the business. The choice of Viatris as a brand name is interesting – besides emphasising the dedication to patients, for those that may be able to recall, the Viatris heritage is associated with an impressive value creation history. In 2002, Degussa deemed Viatris Pharma non-core to its specialty chemicals business and sold the business to Advent International for Euro 375M, which in turn sold the company a mere three years later to Meda for Euro €750m. Meda was later acquired by Mylan for a transaction value of $9.9bn. The table below shows recent spinoff transactions and how the transactions have been designed to financially turbo-charge the branded pharma business.

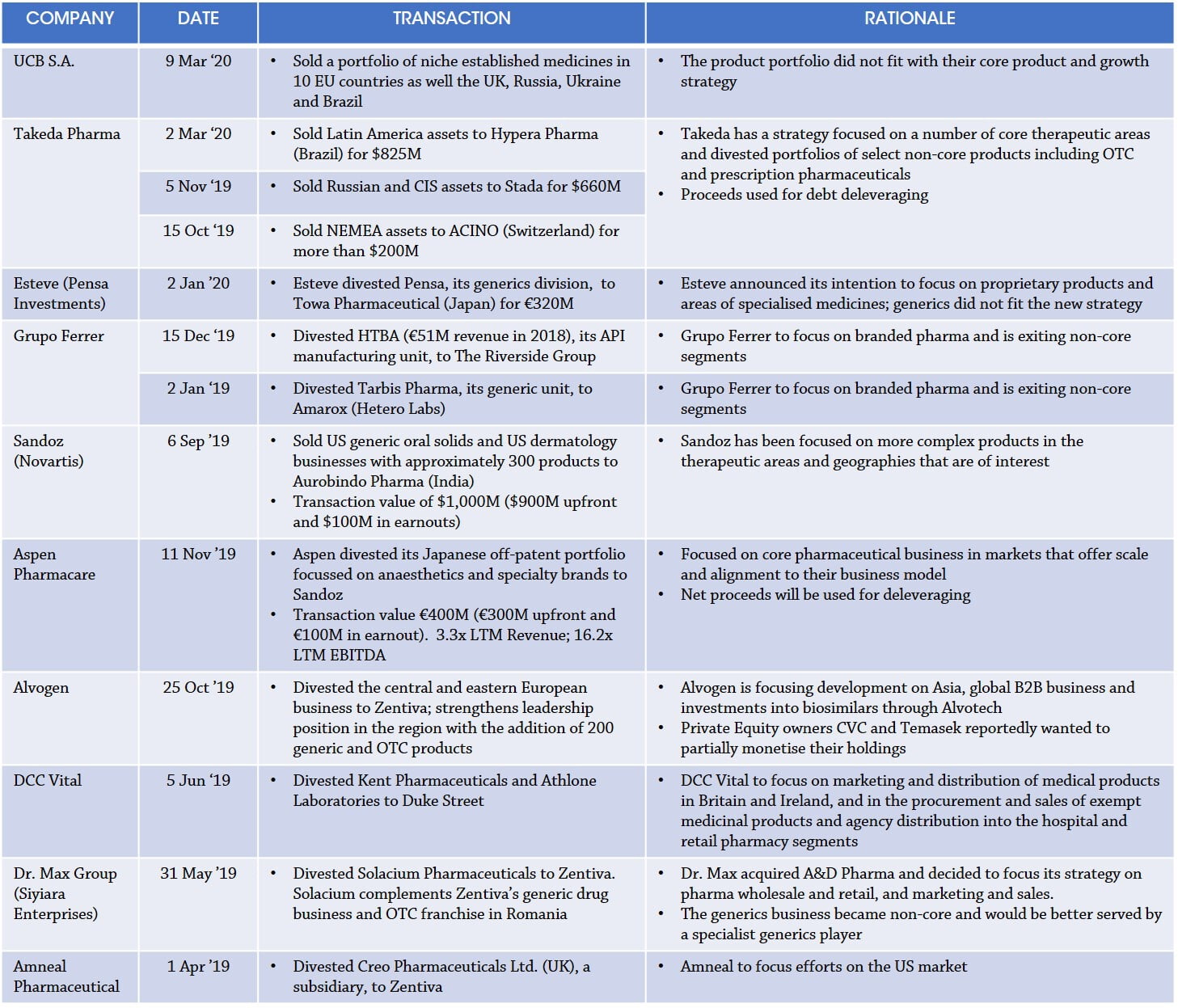

Besides using spinoffs to separate the slower growing businesses, the more frequent methodology employed is the relatively straightforward divestment approach. Figure 4 lists a number of selected divestments that took place in the last 18 months.

Note: On 2nd April 2020, Aurobindo Pharmaceuticals and Sandoz mutually terminated the deal for Aurobindo’s proposed acquisition of Sandoz’s US dermatology business as they could not obtain US Federal Trade Commission approval within the anticipated timelines.