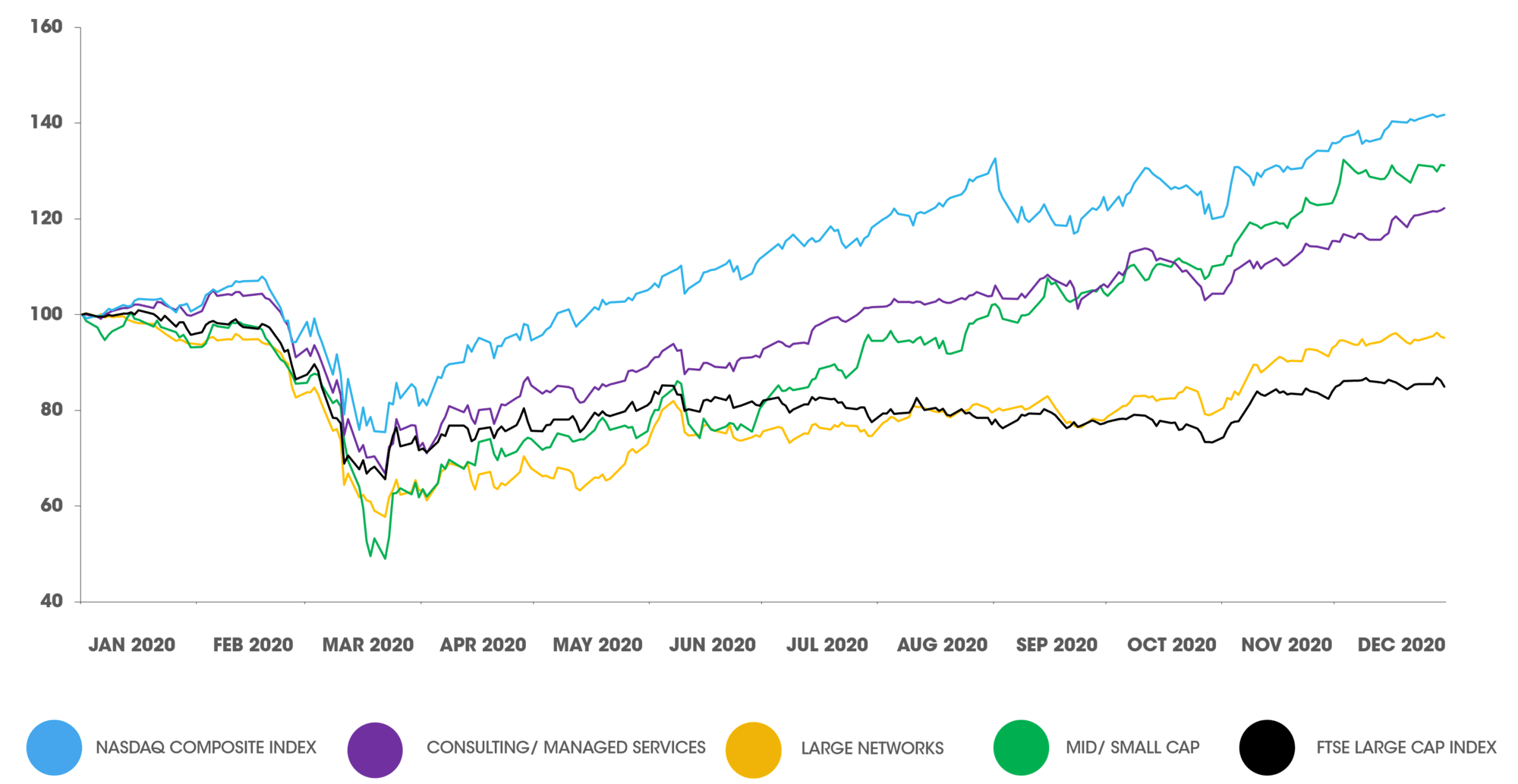

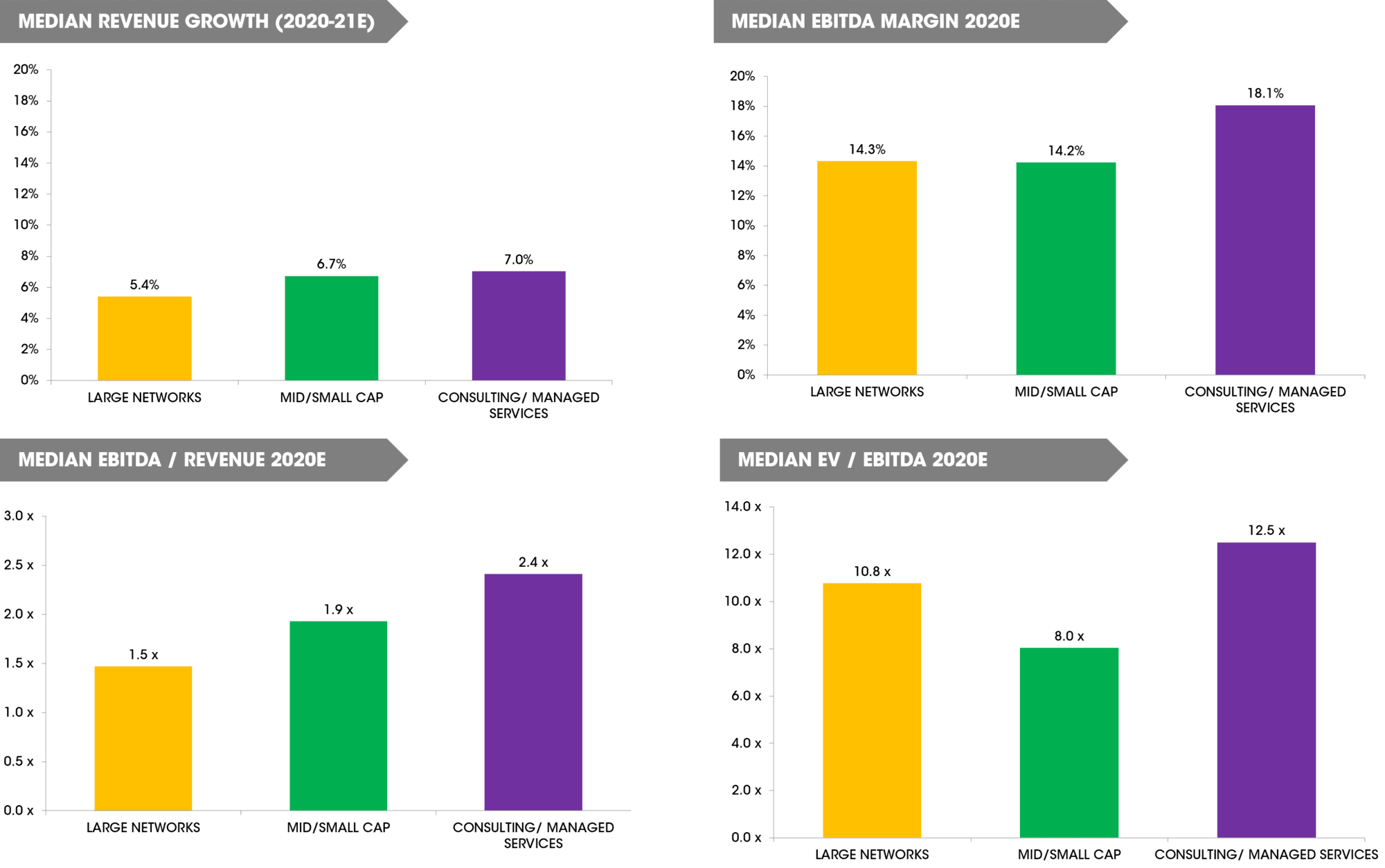

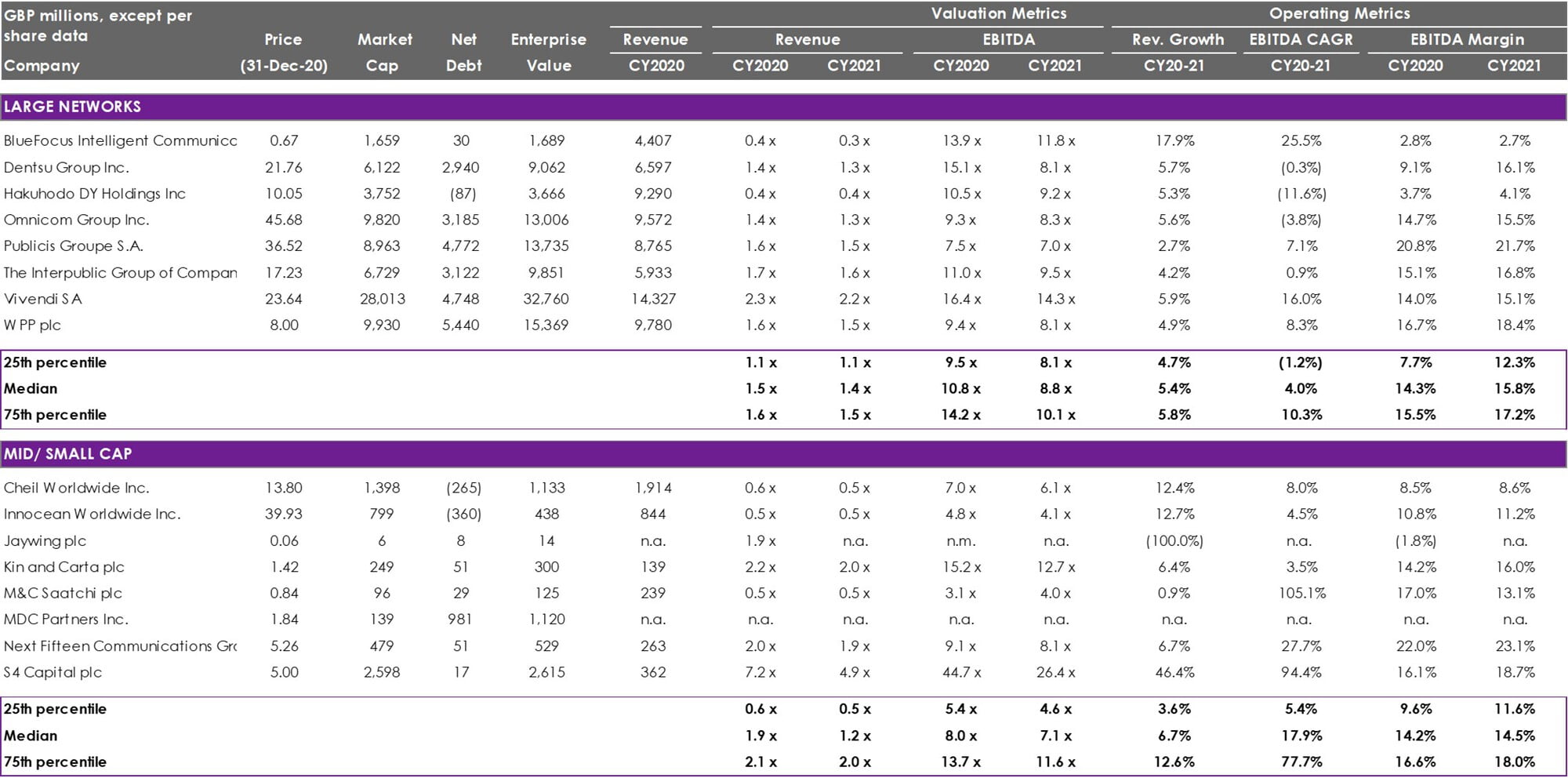

We saw a 50% fall from January share prices across a selection of the large and mid/small-cap marketing services groups in March 2020 compounding existing headwinds felt across this group. The good news is that share prices across the large networks had recovered to over 80% of January levels by the end of Q4. Prices for the mid/small-cap marketing services groups (driven by the gains seen in S4 and Next 15) actually outperformed those seen at the start of the year.

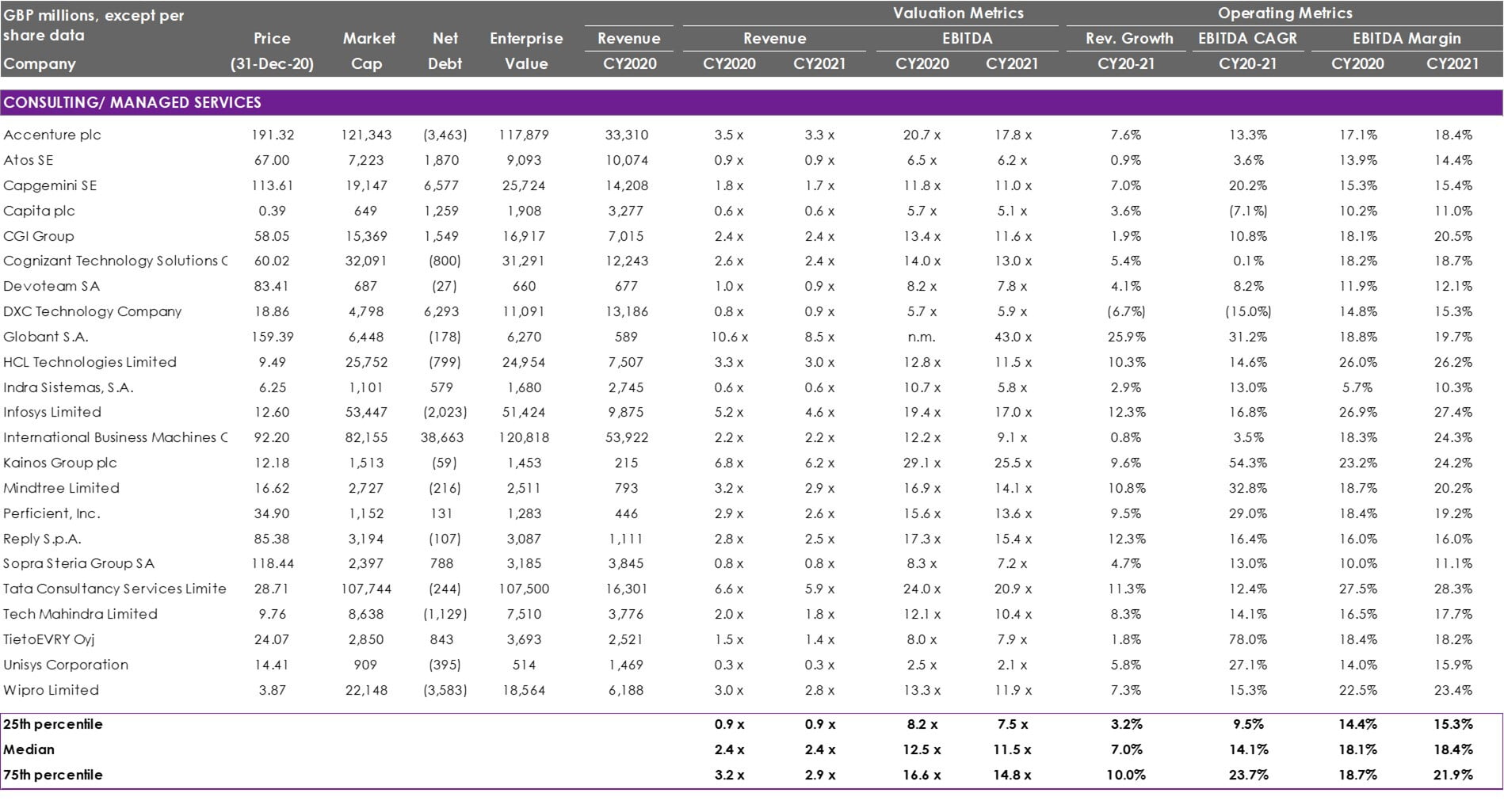

Share prices across the consultancy space fell to around 70% of January levels but we have seen a more positive trajectory through the year, with share prices and EV/EBITDA multiples in excess of the levels seen pre-Covid, in January 2020.