The enterprise software market review: Q1 2022

Welcome to the Q1 2022 edition of the Enterprise Stack report – Results’ quarterly market update for the enterprise software sector.

Contact: Julie Langley Contributors: Richard Latner, William Garbutt, Vinay Saraiwala, Ryan Wheeler McKinley

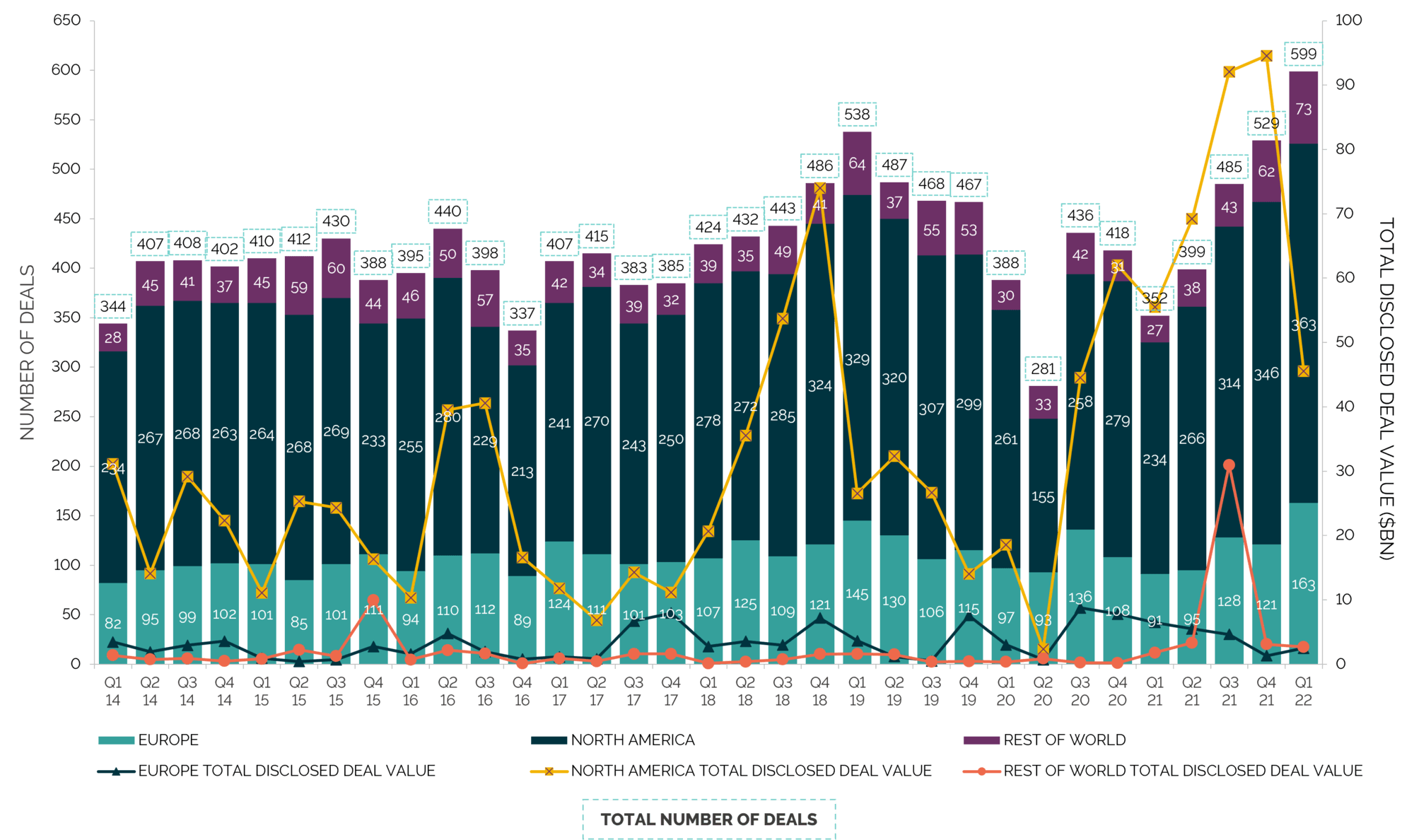

The private M&A market recorded a record quarter for deal volumes in Q1 2022, reaching just shy of 600 deals for the quarter, the highest number since we began tracking activity in 2014. This was in sharp contrast to activity in the public markets - after a record year for IPOs in 2021, Q1 2022 saw a slow down in activity as a background of geopolitical uncertainty saw some listings put on hold

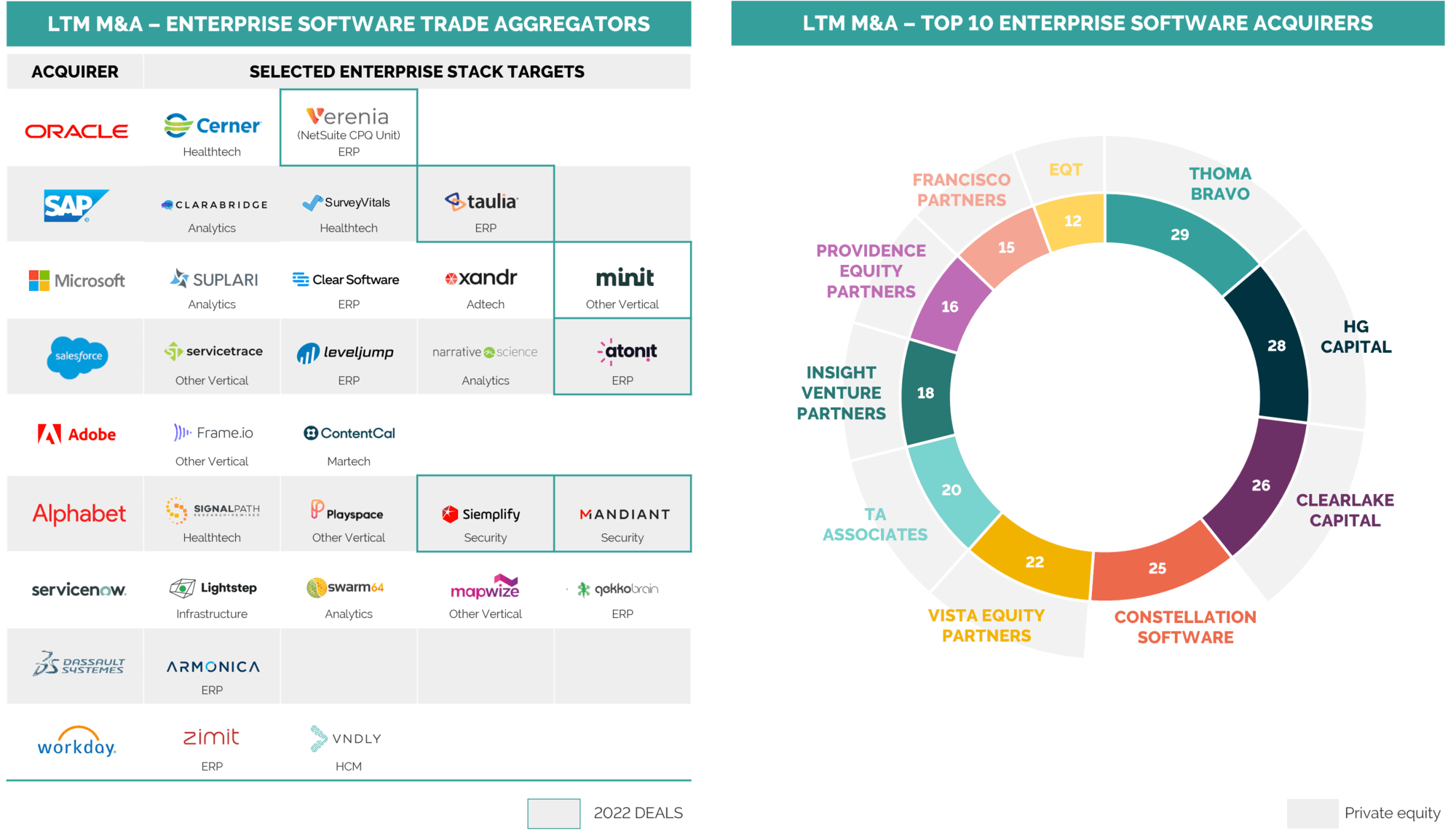

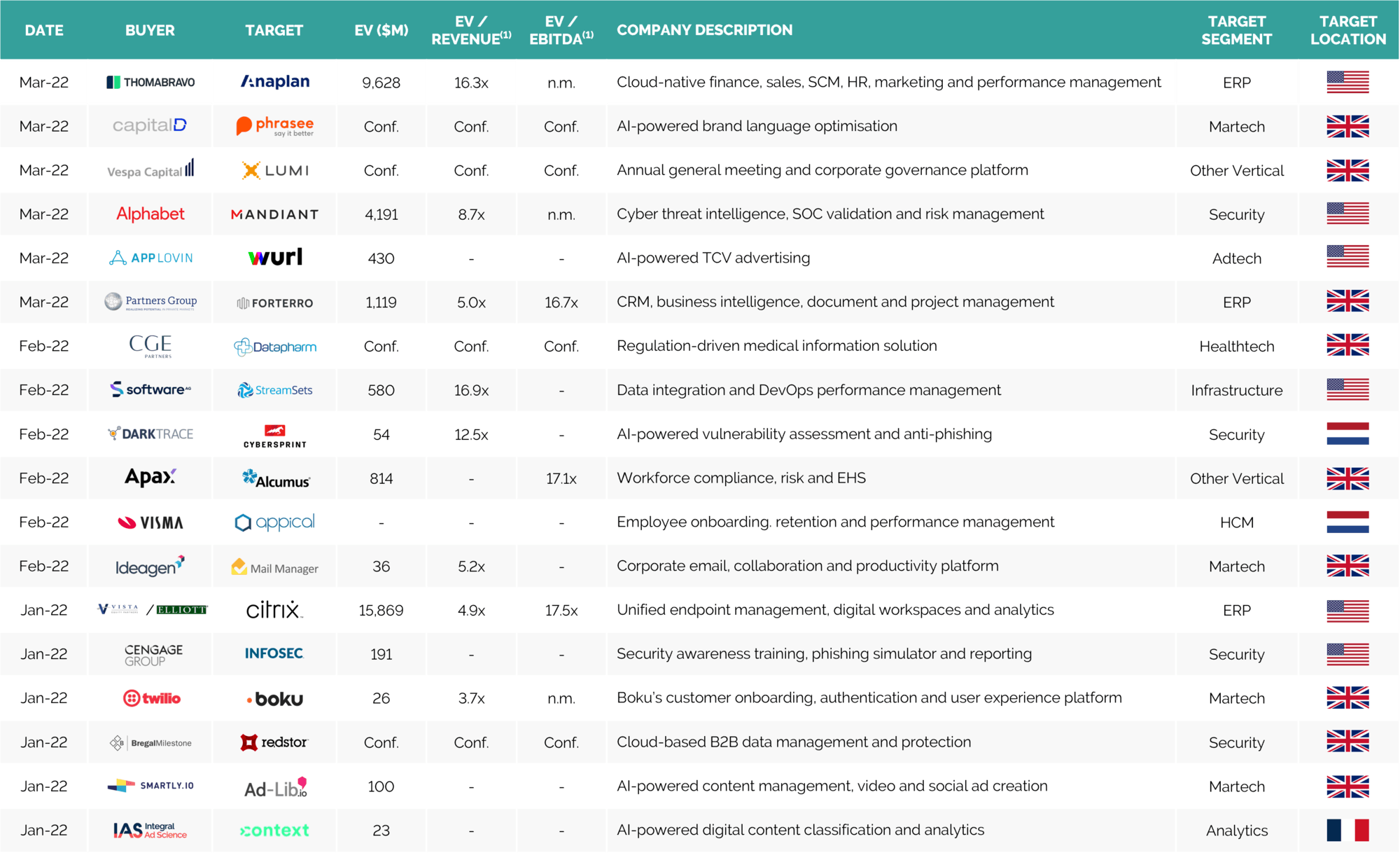

As the sophistication of cybersecurity threats continues to increase, cloud providers have stepped up their investment into security products to keep their networks secure. One of the standout transactions from Q1 2022 was Google’s acquisition of threat intelligence platform Mandiant for c.$5Bn, it’s second largest acquisition ever. Google also acquired SOAR platform Siemplify for $500m earlier in the quarter, together both deals represent a substantial investment into Google’s inhouse cloud security capability as it matches the recent spending in the space from other “Big Tech” rivals

The value of cloud deployment and the adoption of cloud technology shows no sign of slowing. Vista Equity Partners and Elliot Management took Citrix Systems private for c.$16Bn, with the intention that it will merge with Vista’s existing investment, Tibco, bringing the latter's analytics capability alongside Citrix’ cloud computing services

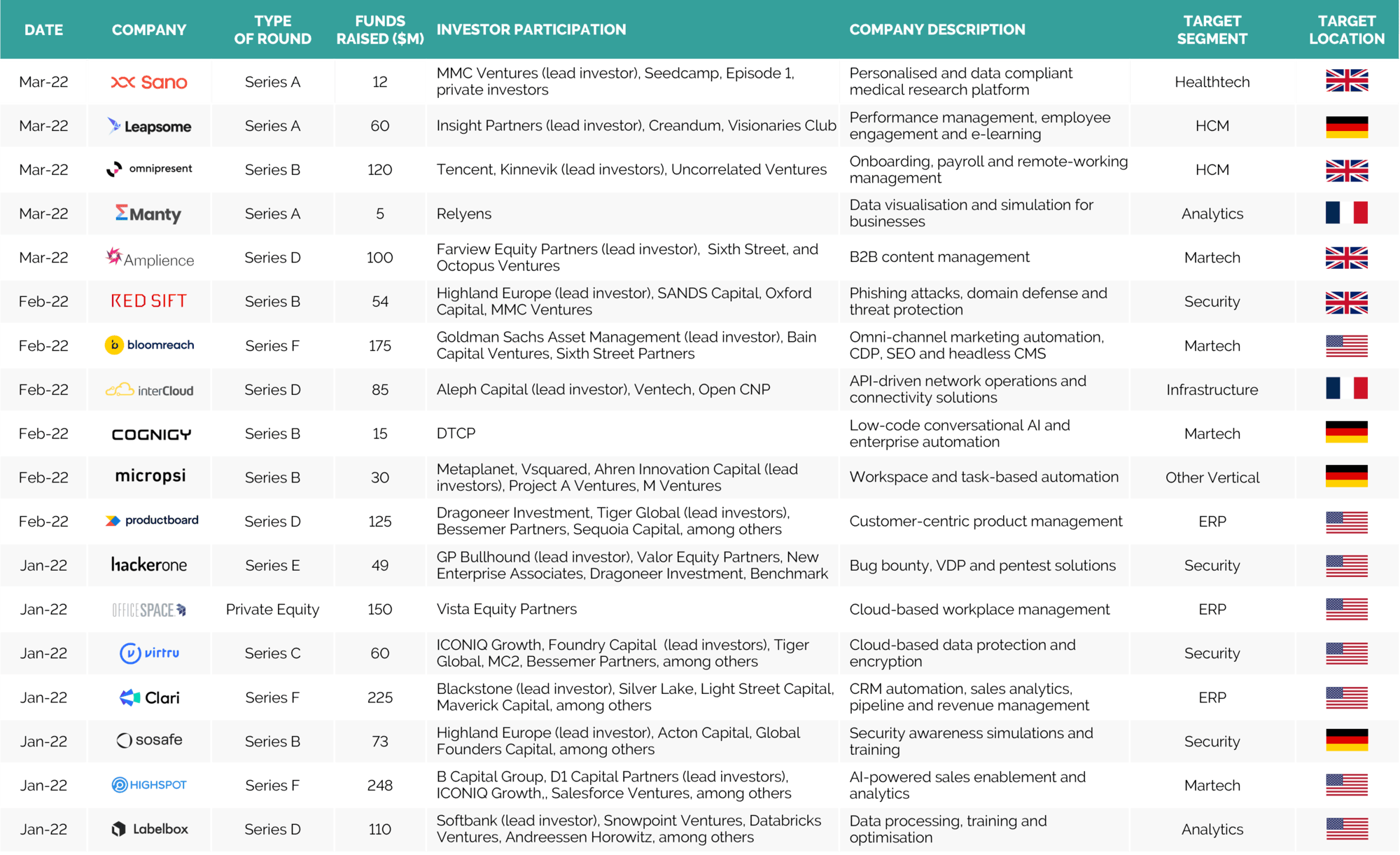

With the pandemic now abating in most geographies, it is becoming apparent that a hybrid work environment is here to stay. With that, many organisations are doubling-down on their investment into ‘work-anywhere’ solutions that also ensure data compliance and security is maintained. This quarter Results advised remote-AGM and corporate governance platform Lumi Global on its recapitalisation from Vespa Capital; Lumi is an example of a platform facilitating highly-secure and data compliant remote work

After being forced to rapidly adopt a more digital-first strategy over the last two years, brands are now prioritising unified digital experiences to secure customer loyalty and drive brand advocacy. Innovative new technology solutions are helping marketers to deliver on this strategy and in Q1 2022 Results advised AI-powered brand language optimisation platform Phrasee on its majority investment from Capital D; this investment will fuel geographic expansion and accelerate product innovation

The IPO market is expected to normalise later in 2022 with a flurry of Big Data platforms all lined up to go public in H2 including Databricks, Cohesity and Qlik

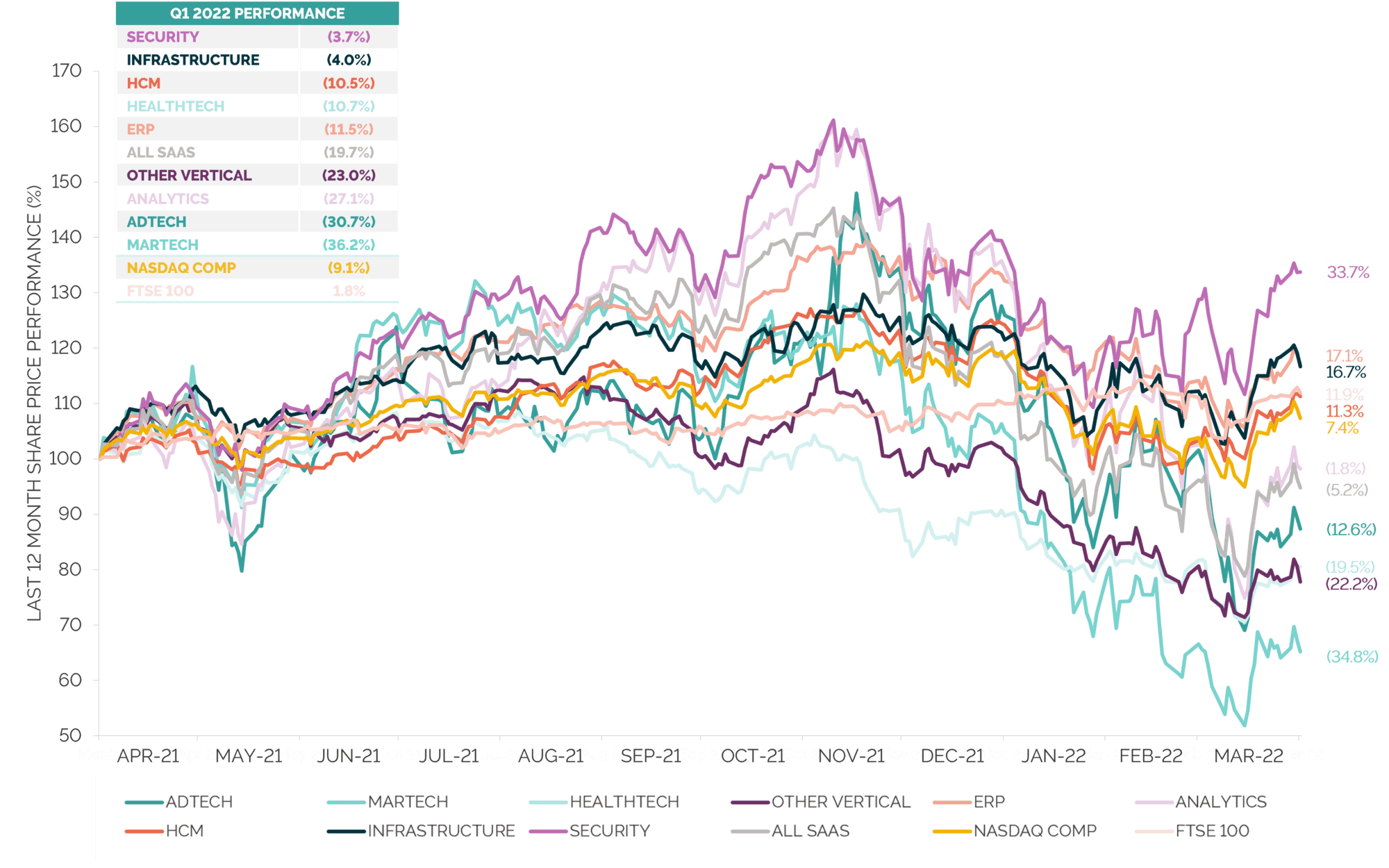

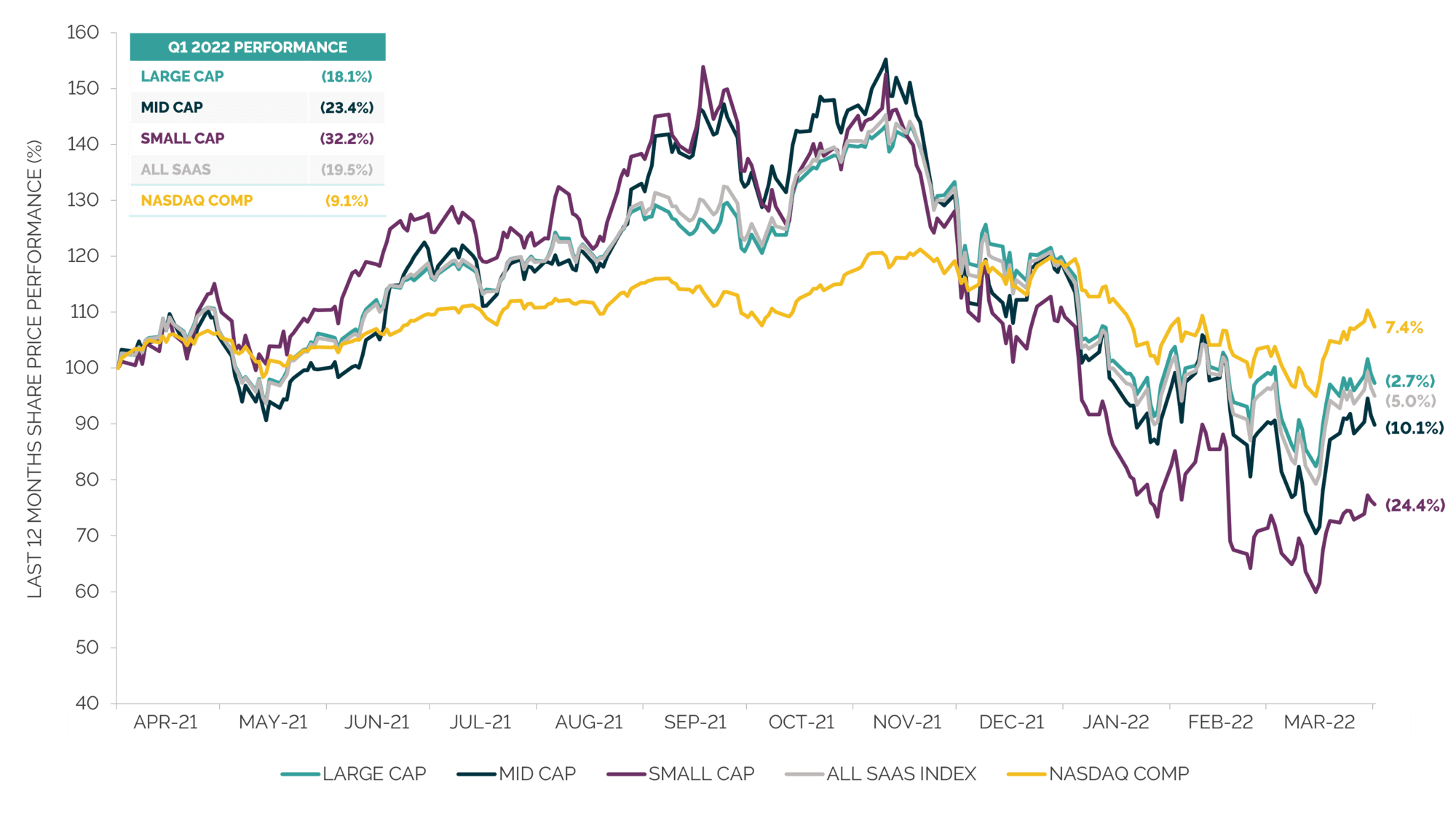

Notes: Based on share prices as at 31st March 2022; indices weighted by market capitalisation. Sources: Capital IQ and Results analysis

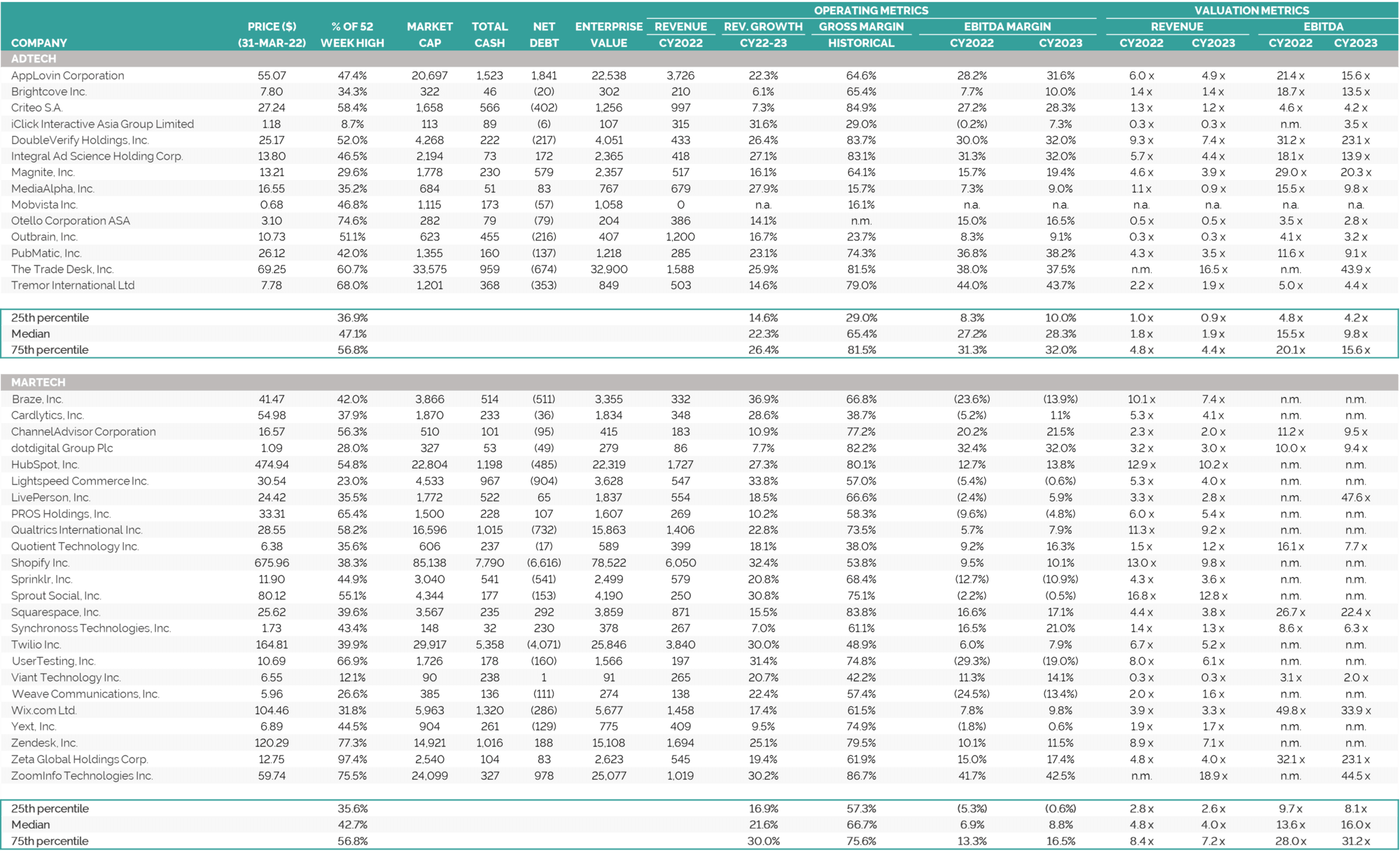

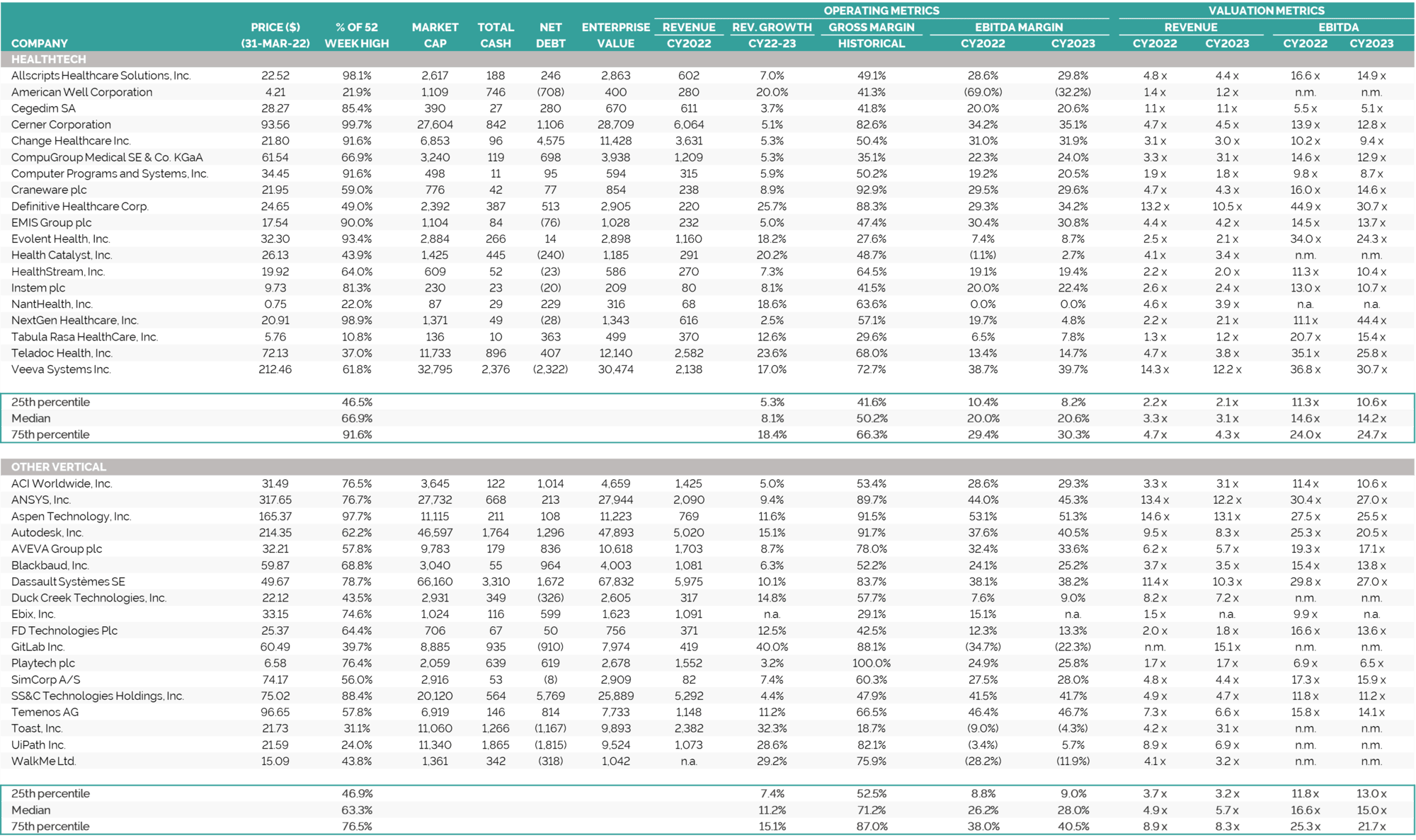

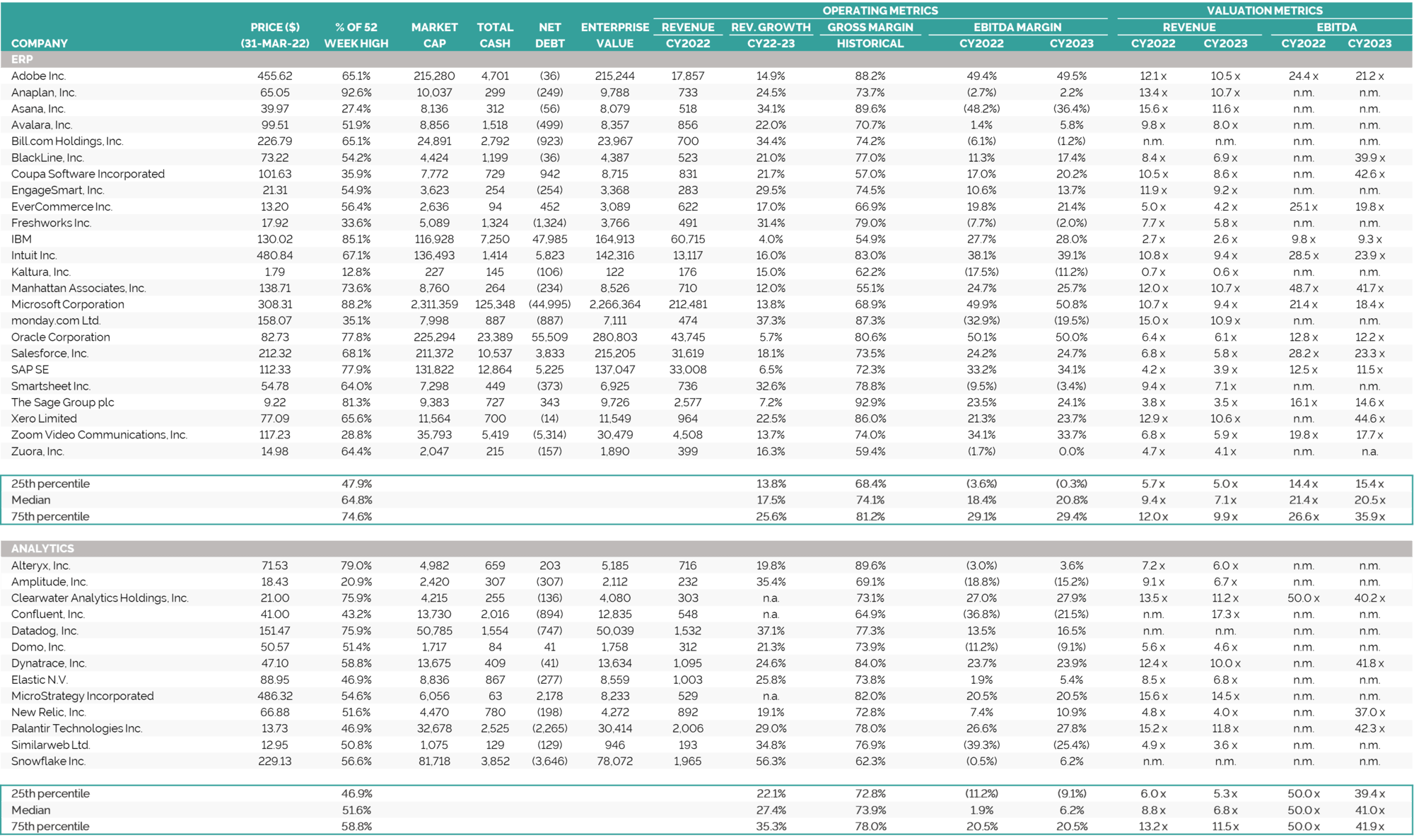

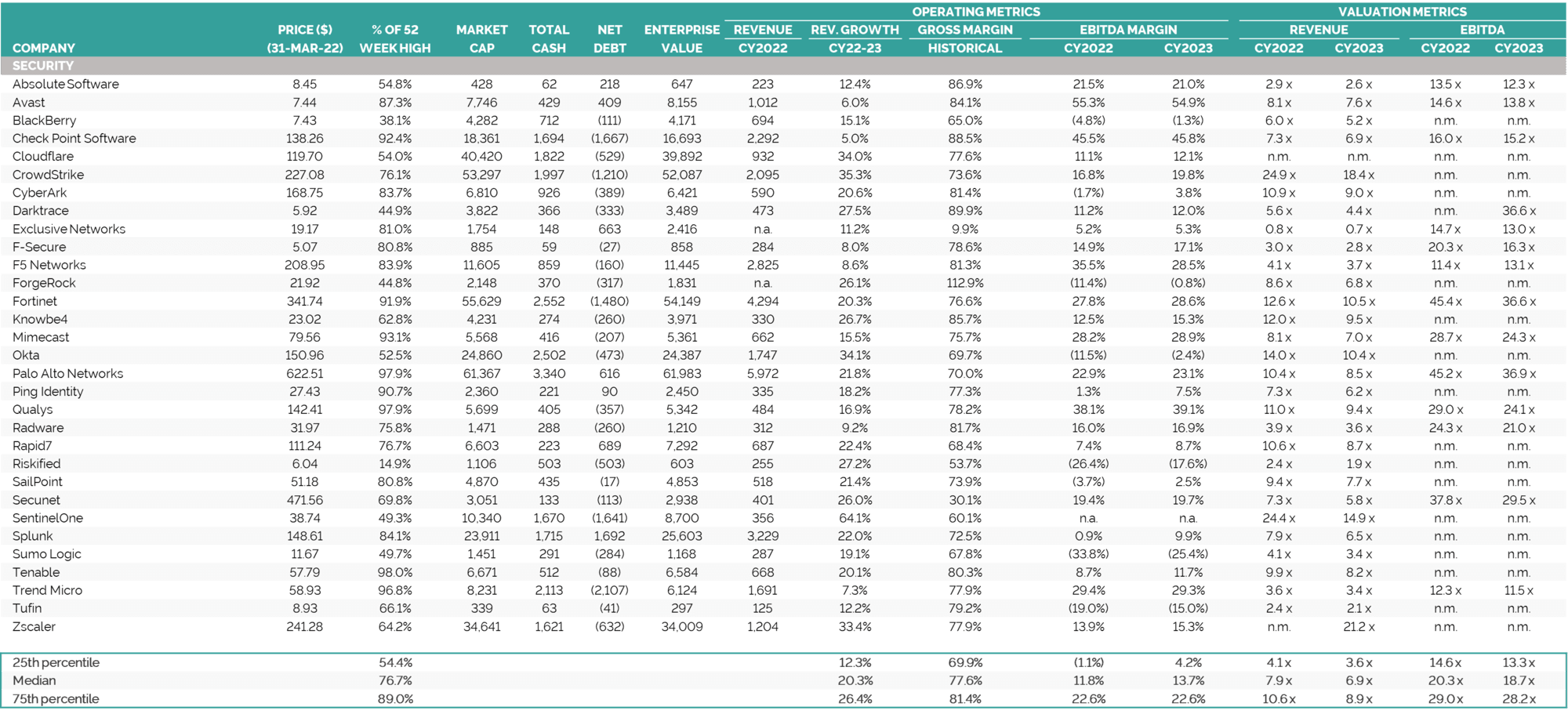

Note: For Security, 75th percentile values have been overlaid (shaded lighter) to illustrate next-generation vendors Note: EV = Enterprise Value; financials calendarised to December year end; median values reported See Selected Publicly Traded Companies here for details of companies included in each category. Source: Capital IQ

Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results analysis

Note: PE shown as acquirer when acquisitions made through portfolio company; parent shown as acquirer when acquisition made through group subsidiary / group Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results analysis

(1) In certain cases EV/Revenue and EV/EBITDA are publicly reported estimates; TTM financials have been used where possible; EV = transaction value scaled to 100% shareholding plus net debt (incl. minority interests). Note: Earnout considerations excluded in the calculation of the enterprise value. Sources: Press releases, 451 Research and Results International analysis

Sources: Pitchbook, Press releases, Crunchbase and Results analysis

Note: Based on share prices as at 31st March 2022 Sources: Capital IQ and Results analysis

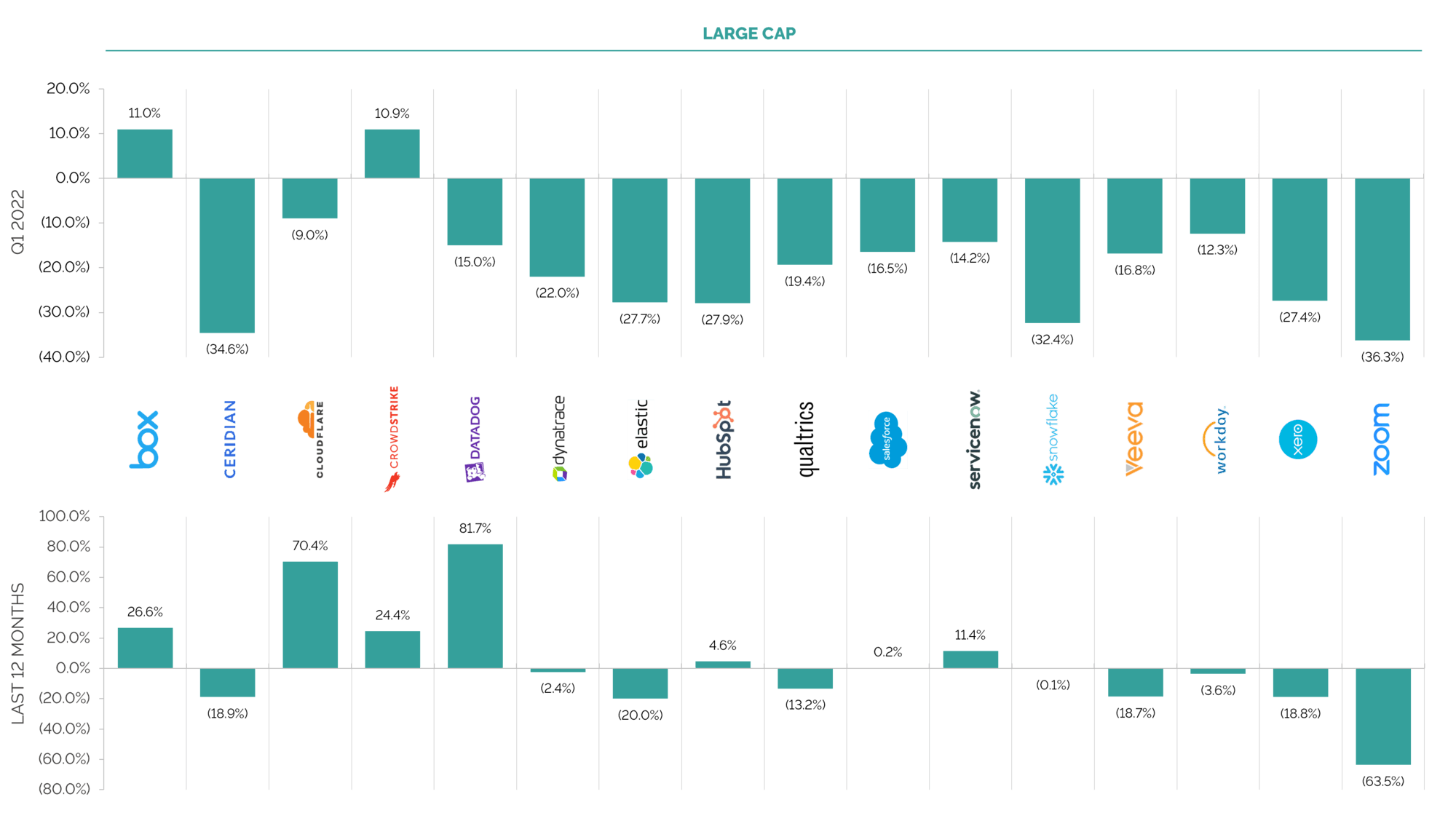

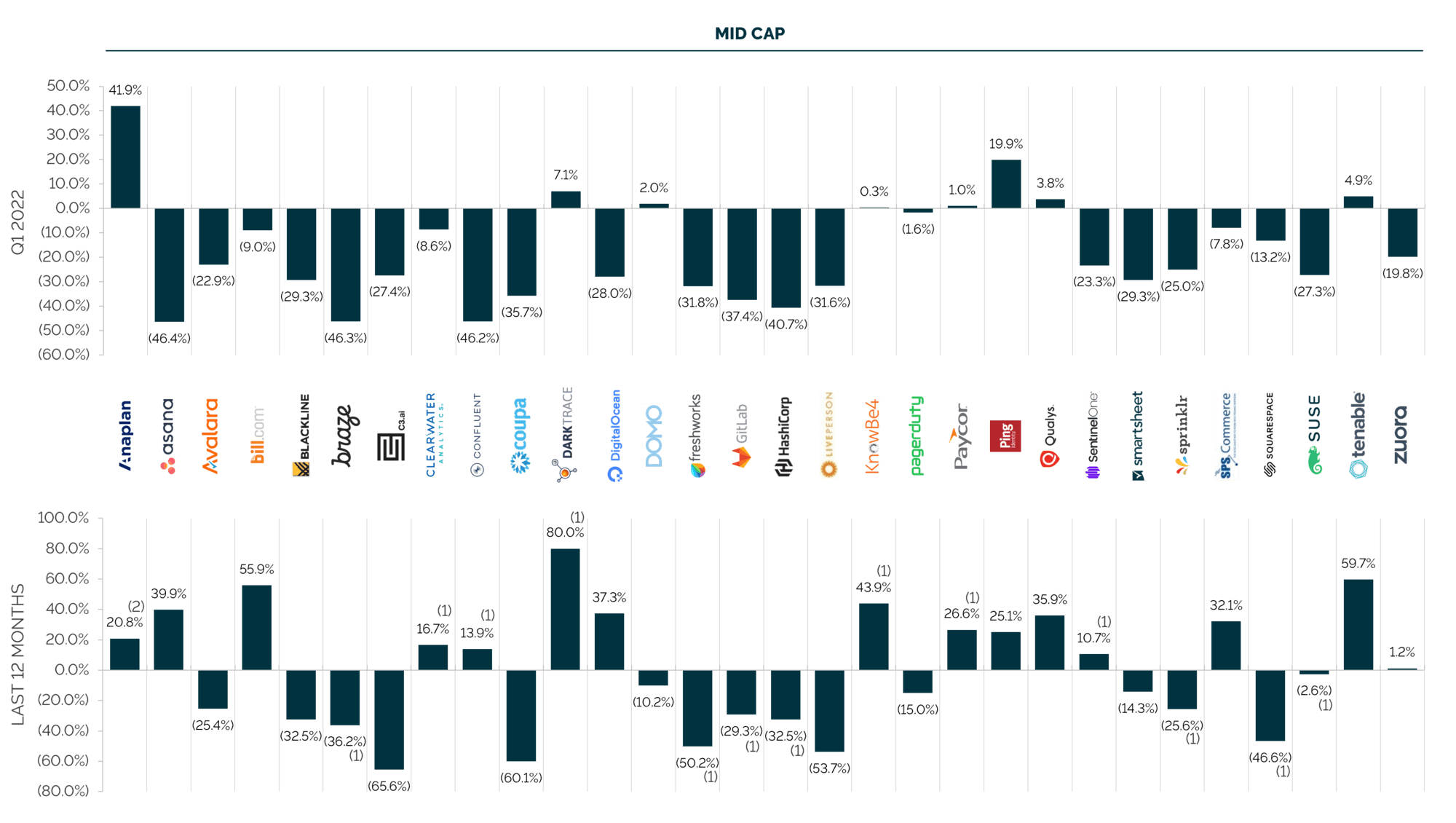

(1) These companies IPO’d within the last 12 months, the share price movement represents the change between the stock’s IPO date and 31st March 2022 (2) Anaplan has been acquired by Thoma Bravo on 21st March 2022 and is expected to go private in Q2 2022. Note: Based on share prices as at 31st March 2022 Sources: Capital IQ and Results analysis

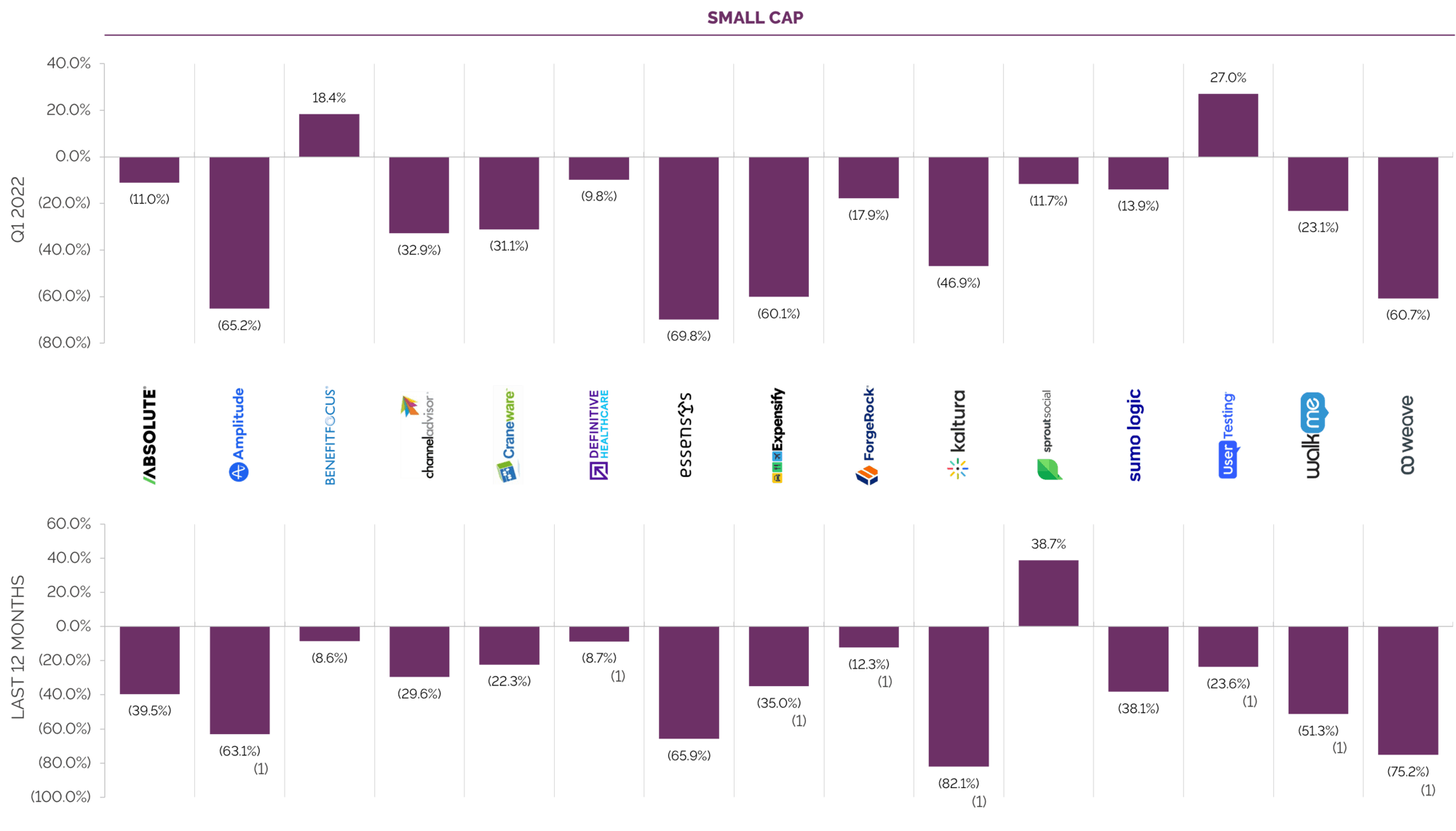

(1) These companies IPO’d within the last 12 months, the share price movement represents the change between the stock’s IPO date and 31st March 2022 Note: Based on share prices as at 31st March 2022. Sources: Capital IQ and Results analysis

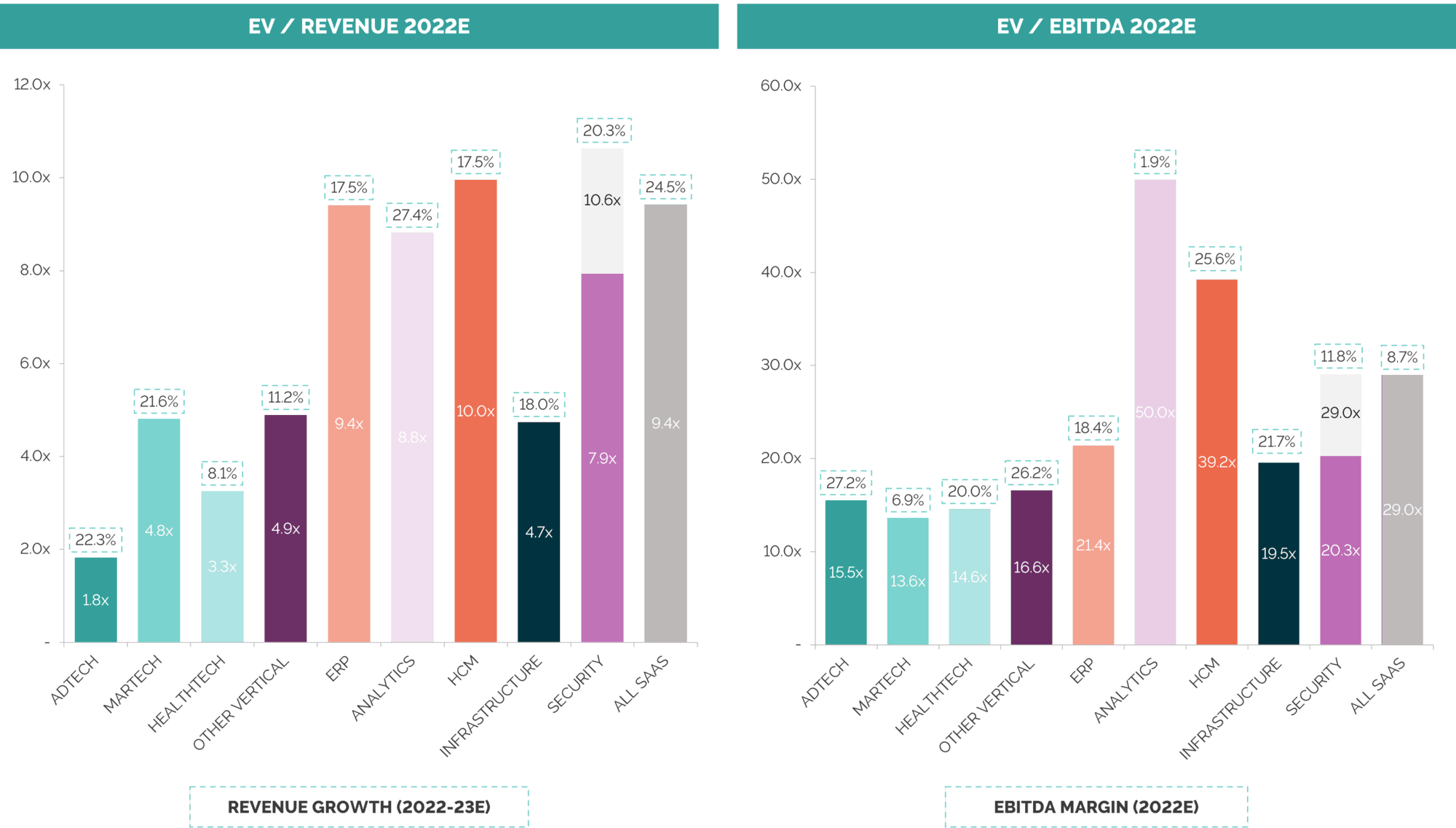

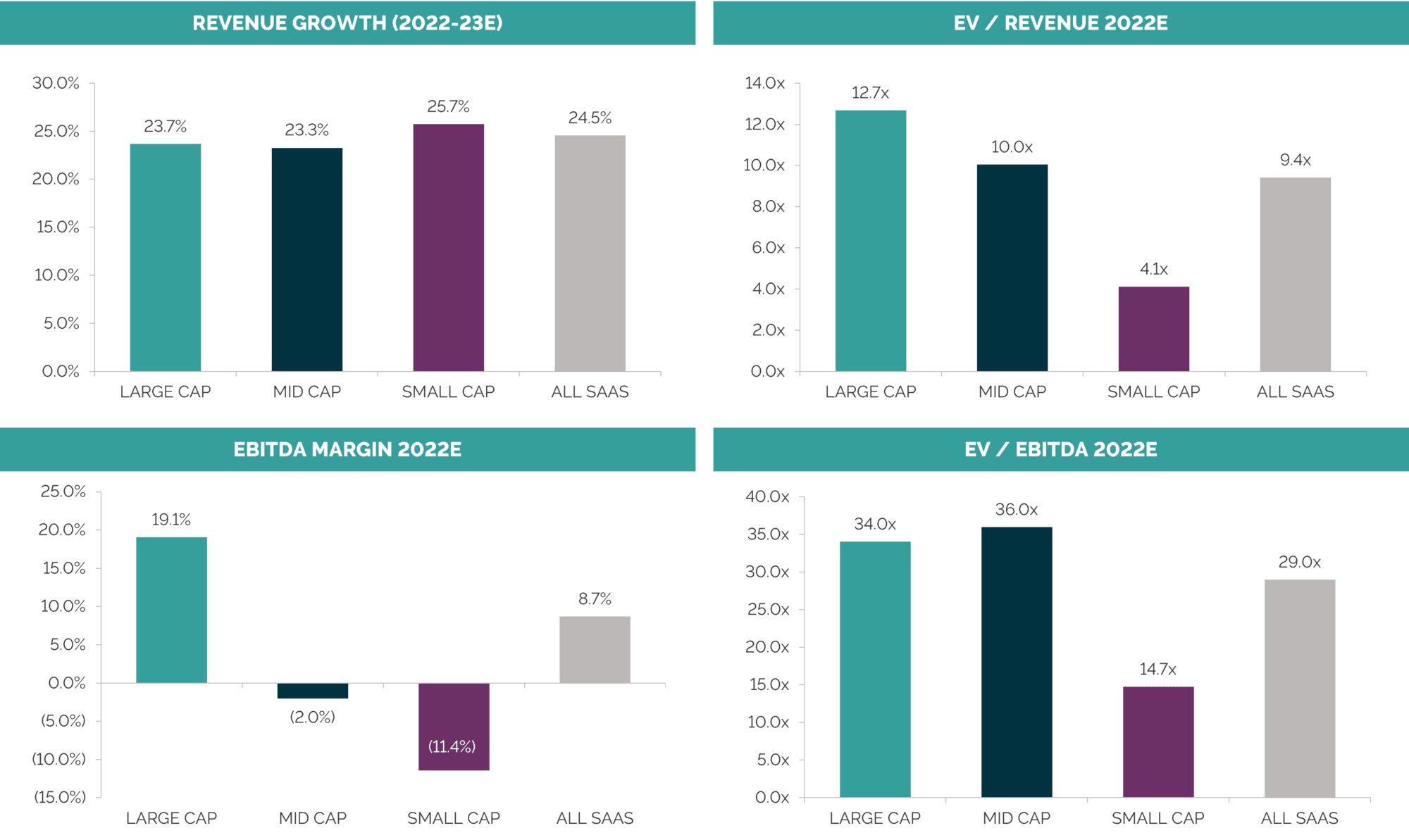

(1) All SaaS represents the median of all stocks in Large Cap, Mid Cap and Small Cap, with no weighting applied. Notes: EV = Enterprise Value; financials calendarised to December year end; median values reported. See Selected Publicly Traded Companies here for details of companies included in each category Sources: Capital IQ and analyst reports

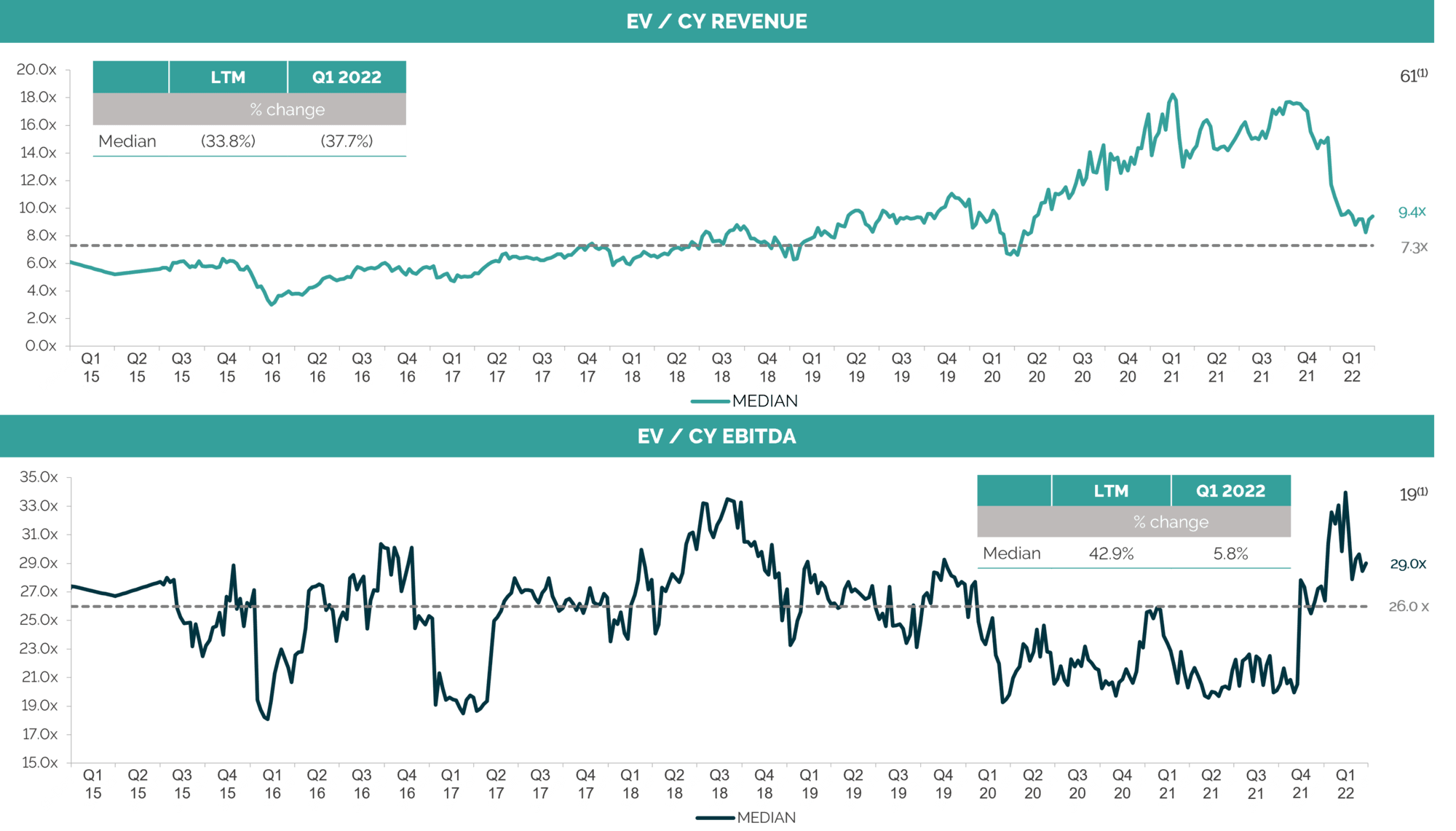

(1) Number of companies with applicable multiples in Q1 2022 index; Notes: EV = Enterprise Value; financials calendarised to December year end, which can impact the multiples at the start of each year as the base is shifted forward; weekly tracking of valuation multiples commenced in July 2015, October 2014 – September 2015 tracked on a quarterly basis, therefore a linear progression has been assumed between quarters up to July 2015 Dotted line represents median since data has been tracked. Source: Capital IQ

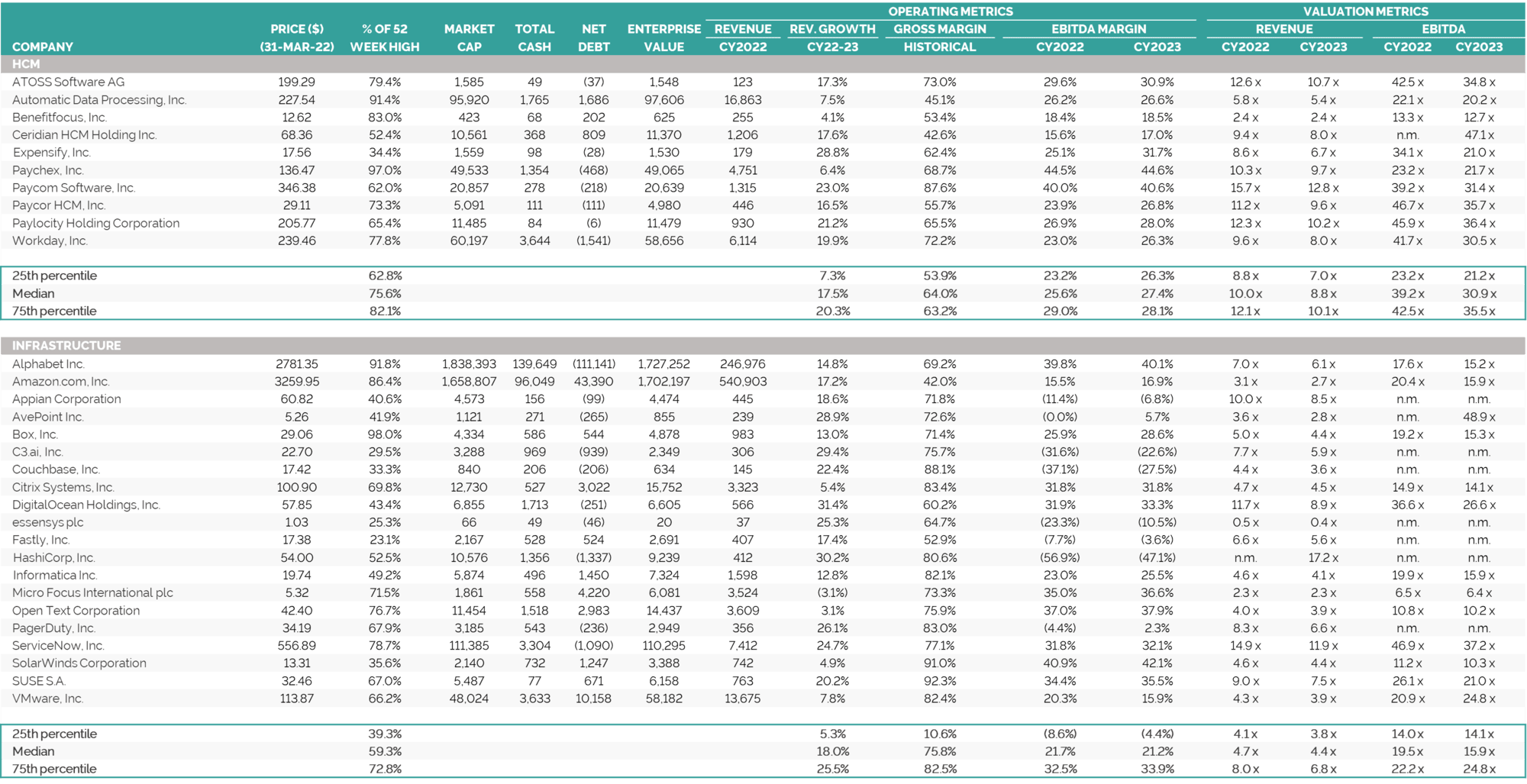

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Sources: Capital IQ and broker reports

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 25x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ

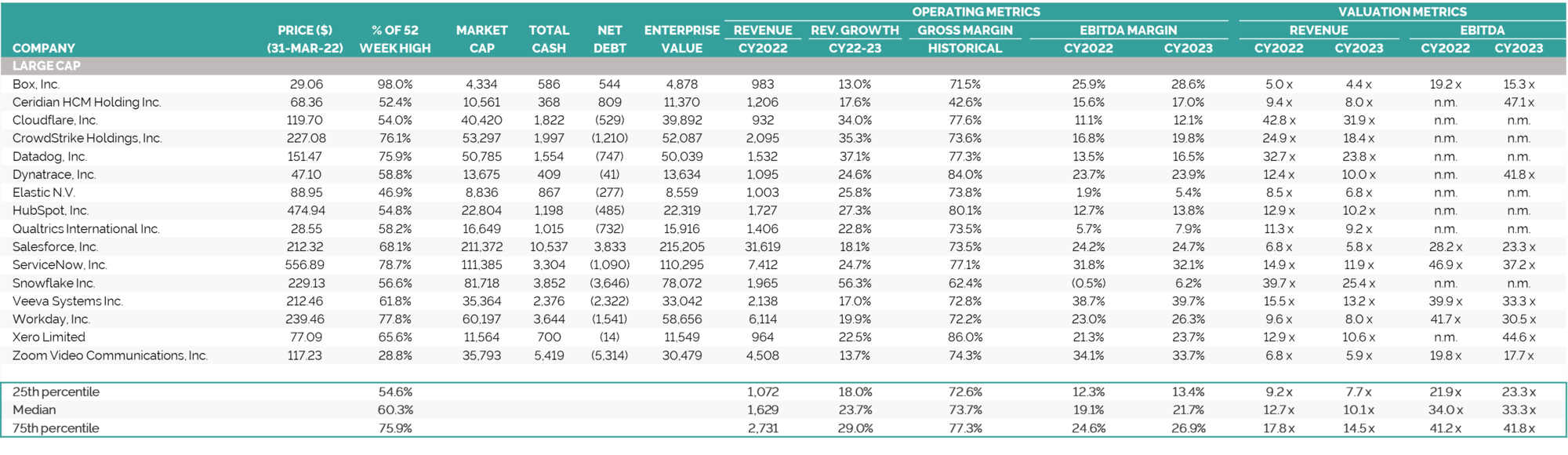

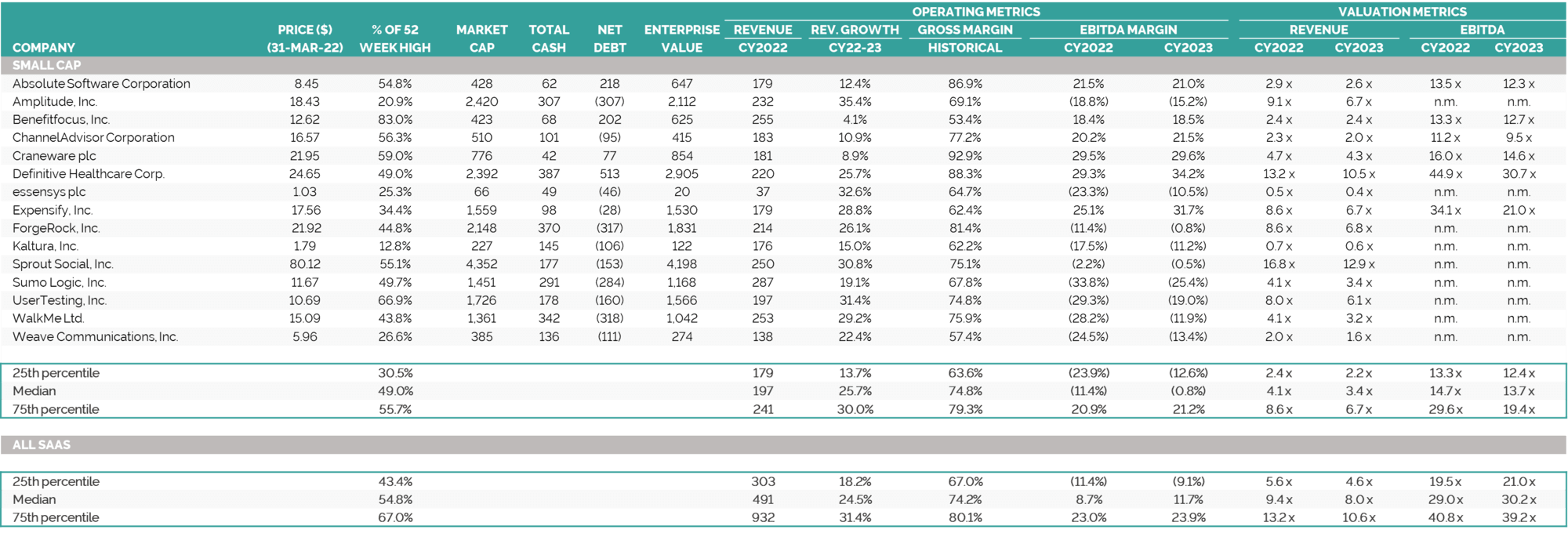

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 100x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Note: Market cap classifications categorised by CY2022E revenue or LTM where CY2022E revenue not available: Large Cap: revenues greater than $900m; Mid Cap: revenues between $300m and $900m; Small Cap: revenues less than $300m Source: Capital IQ

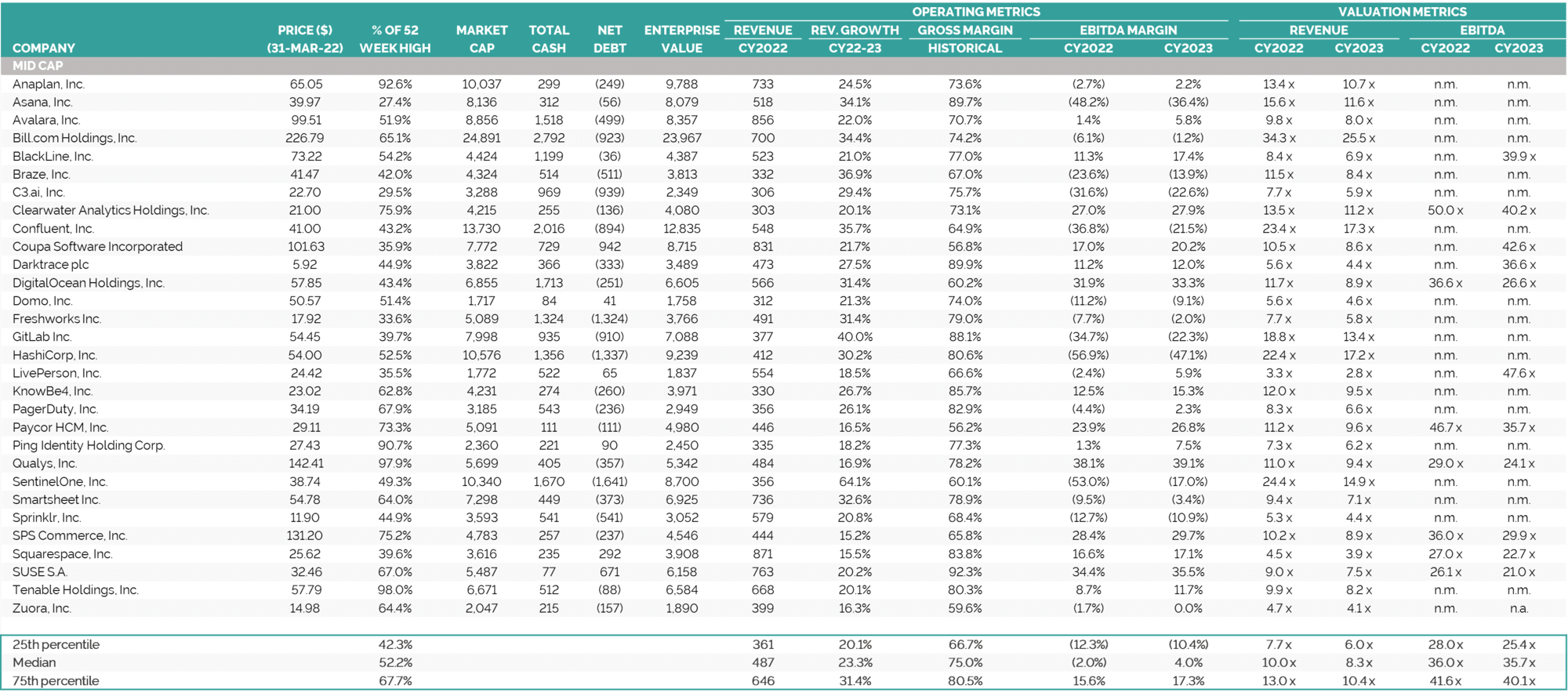

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 100x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Note: Market cap classifications categorised by CY2022E revenue or LTM where CY2022E revenue not available: Large Cap: revenues greater than $900m; Mid Cap: revenues between $300m and $900m; Small Cap: revenues less than $300m. Source: Capital IQ

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 100x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Note: Market cap classifications categorised by CY2022E revenue or LTM where CY2022E revenue not available : Large Cap: revenues greater than $900m; Mid Cap: revenues between $300m and $900m; Small Cap: revenues less than $300m. Source: Capital IQ