Technology services sector market review: Q2 2021

Welcome to the Results International Q2 2021 Technology Services Perspective – Results International’s full-year market update of the technology services sector.

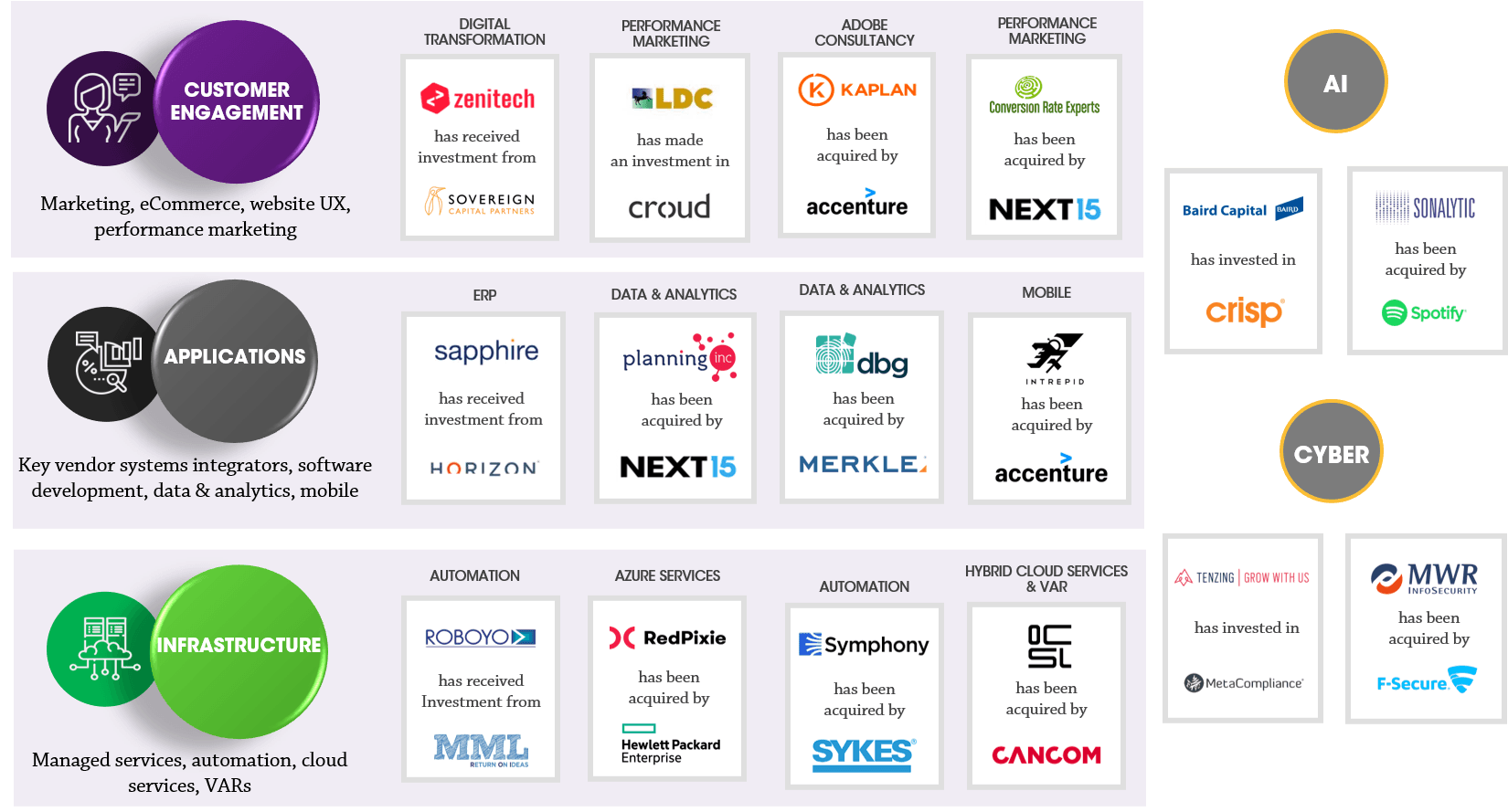

The subsectors we track include (i) customer engagement (marketing & eCommerce, website UX and performance marketing), (ii) applications (key vendor systems integrators, software development, data & analytics and mobile), (iii) infrastructure (managed services, automation, cloud services and VARs), (iv) AI and (v) cybersecurity services. Separately, we cover the broader marketing services market (beyond the customer engagement categories mentioned above) in our quarterly Marketing Services Market Review and security software in our quarterly CyberScope.

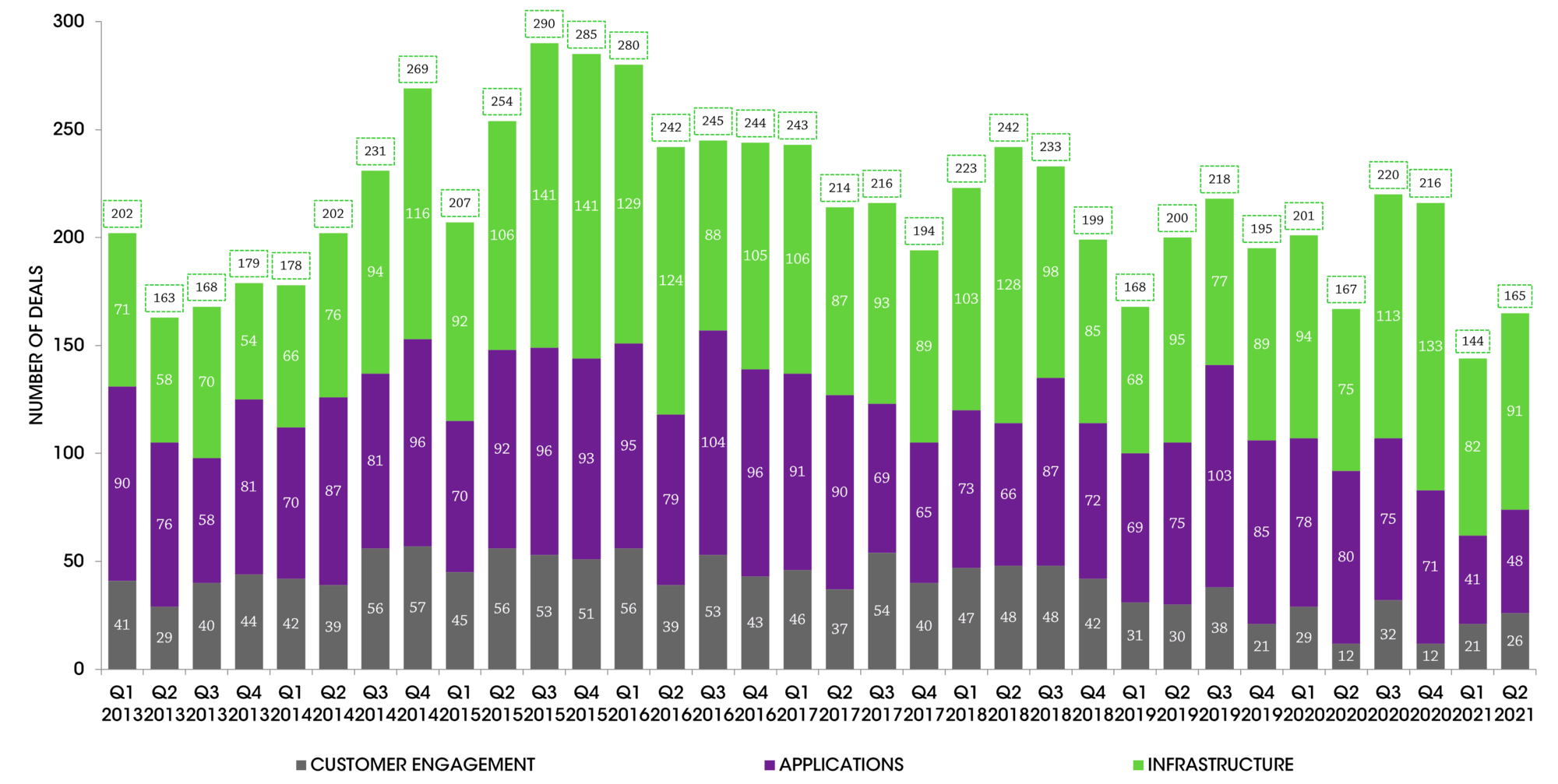

As we predicted in Q1, deal volumes have increased in Q2 (up 15%) including a number of very notable transactions and we have seen continued strength in deal valuations and public market activity.

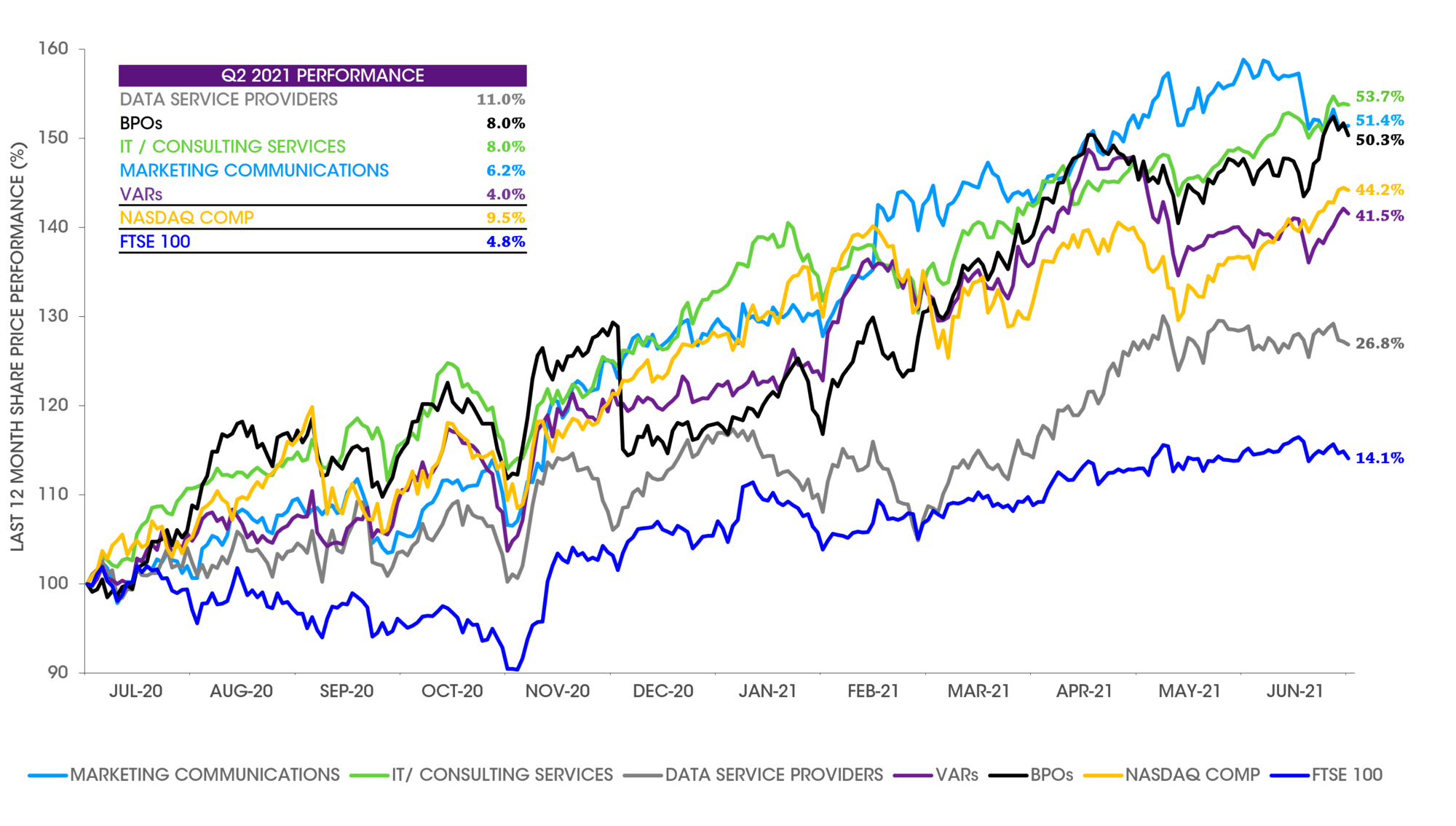

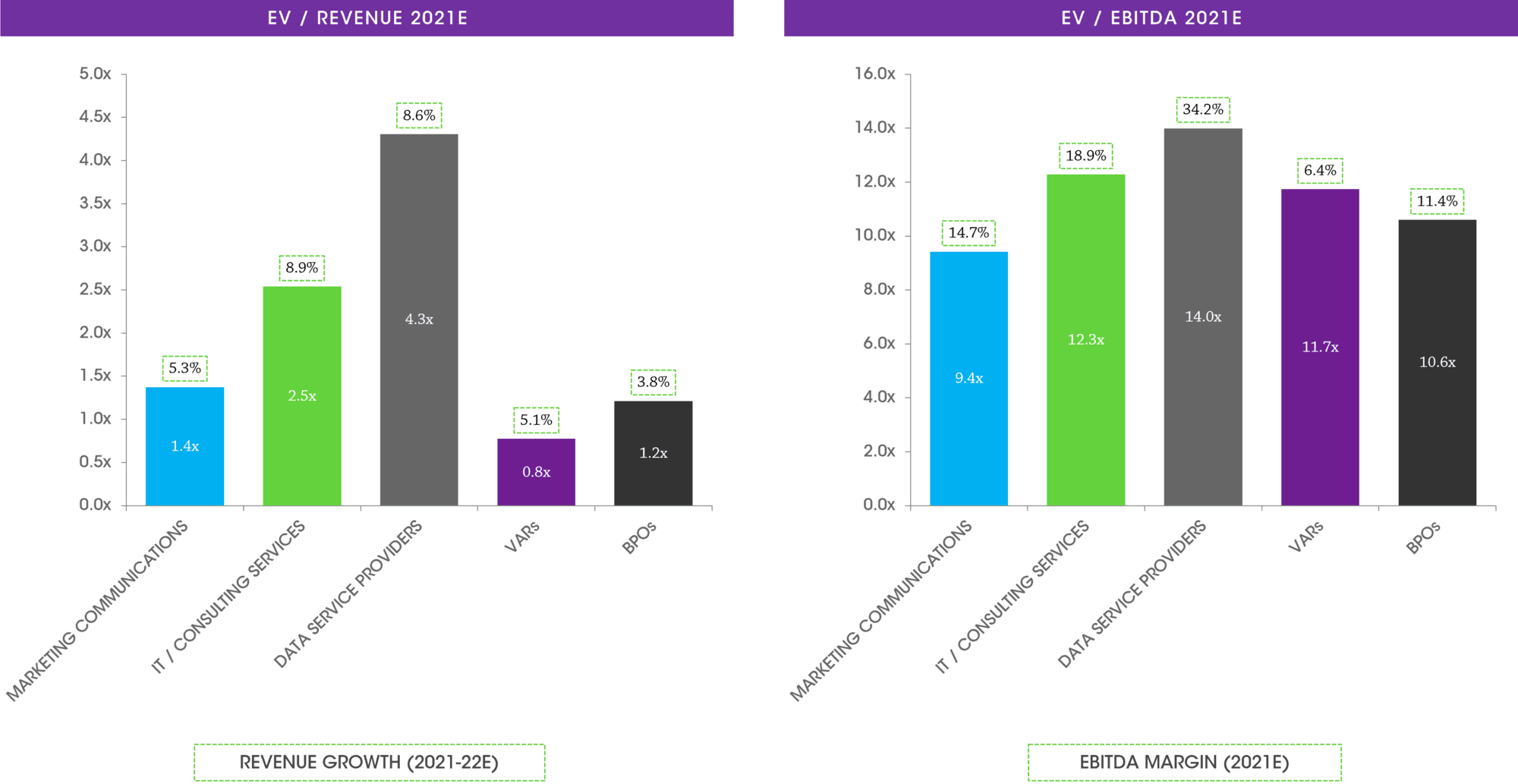

Unsurprisingly, public companies in tech are tracking closest to Nasdaq’s trajectory in the past 12 months compared to the FTSE, with many companies tracking 40-50% ahead of the share price in June 2020 and median EV/EBITDA multiples largely in excess of 10x. Growth and profitability command a premium valuation dynamic along with a focus on emerging technologies and a perception of providing end-to-end digital transformation services being the strategic operator and engineering execution partner of large scale programmes.

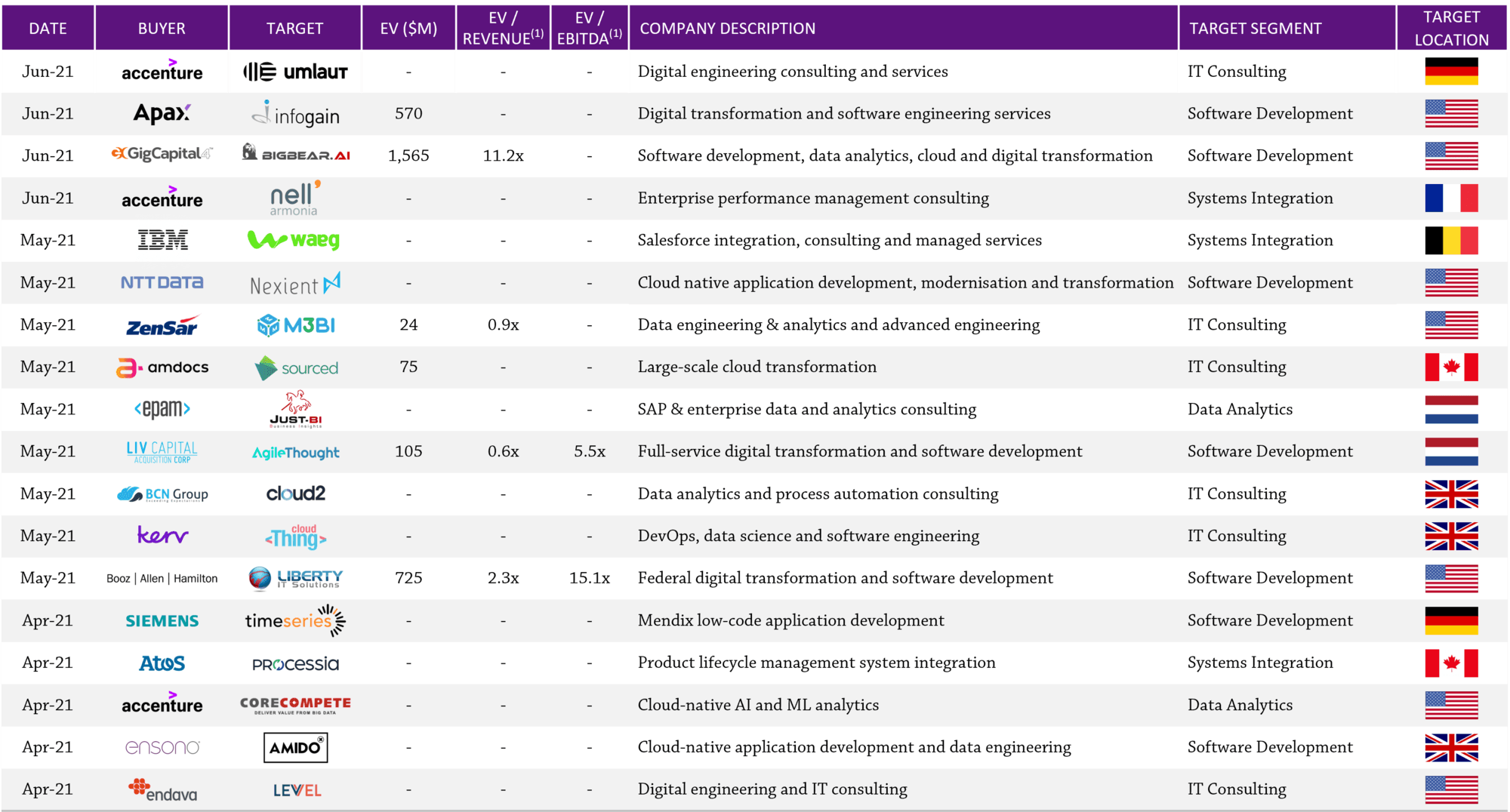

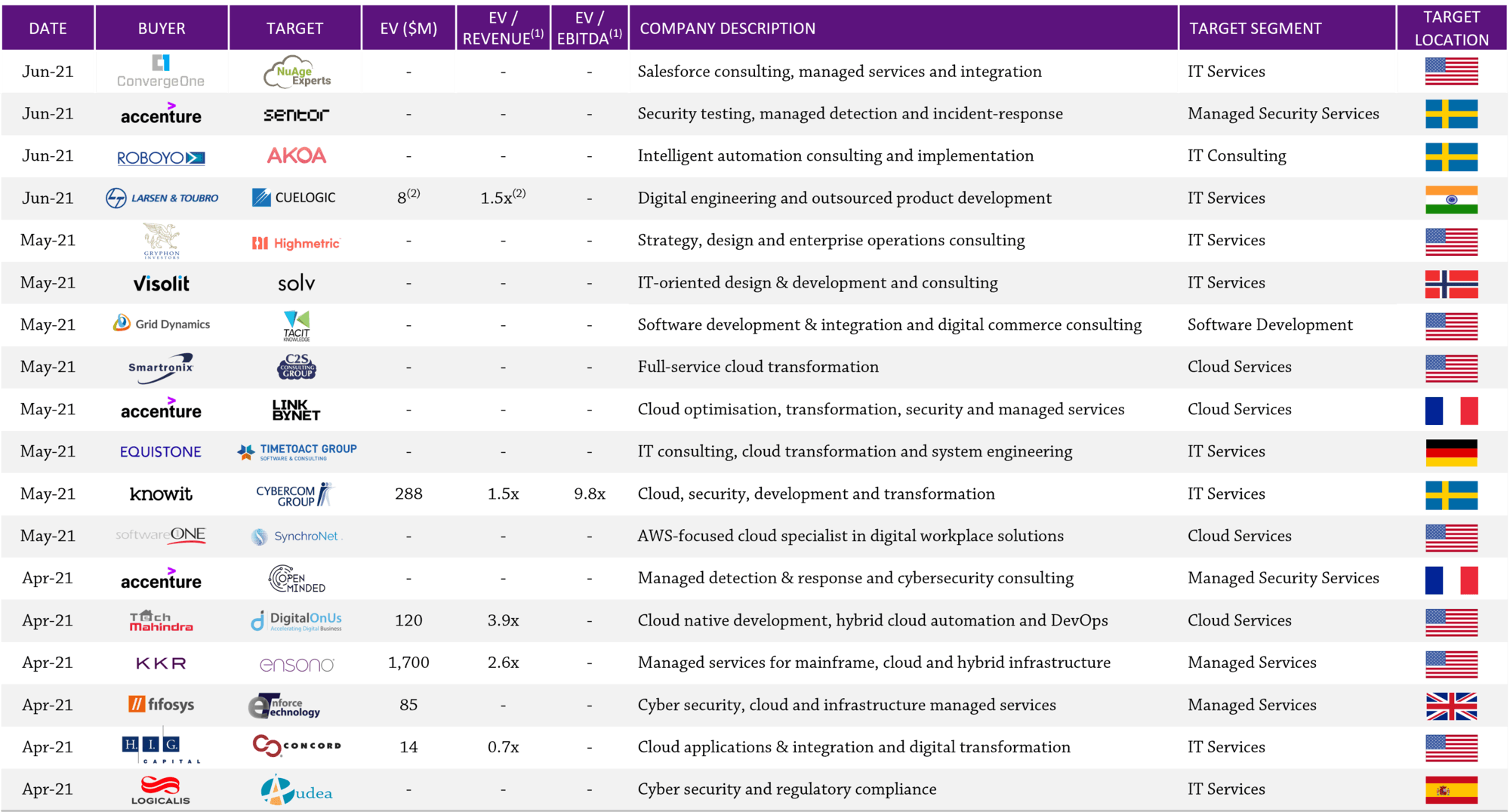

This theme is mirrored in many of the M&A transactions including Booz Allen Hamilton’s acquisition of Liberty IT Solution (software development) for $725m (15x EBITDA) and Knowit’s acquisition of Cybercom (cloud services) for $288m (10x EBITDA). Both transactions reflect an increasing focus from strategic consultants to own more of the customer journey, particularly given the budget allocation influence they have in the boardroom, as they continue to reflect on the success that Deloitte has had in broadening out its own end-to-end stack.

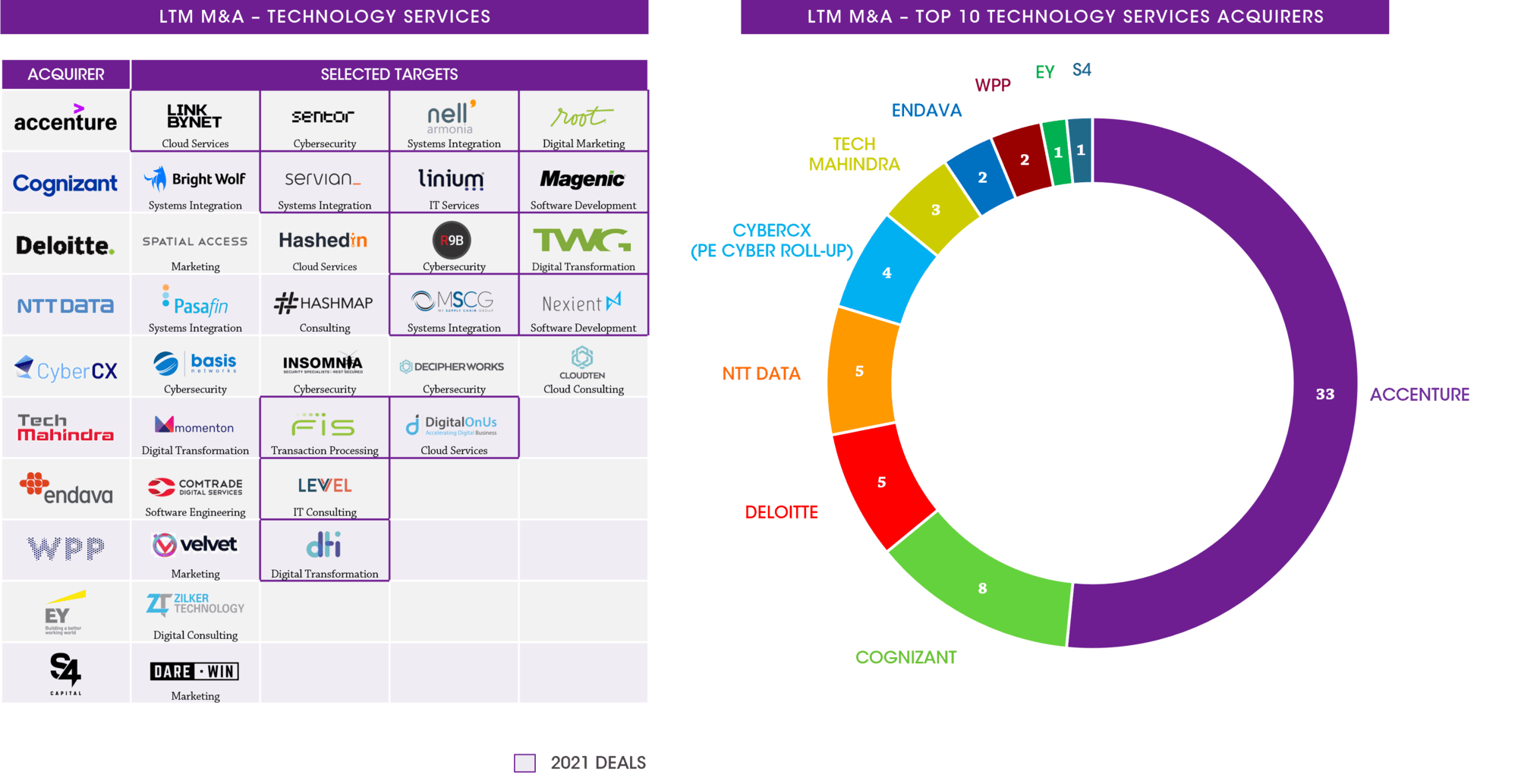

Elsewhere, Accenture continues to be the most prolific acquiror across the spectrum and is undertaking its M&A strategy across multiple geographies and capabilities, focusing on single-region scale-up, rather than large international M&A. Private equity and investors also continue to be particularly active, with notable transactions including KKR’s investment in US-based MSP Ensono for $1.7bn (nearly 3x revenue) and GigCapital’s acquisition of AI software development house Bigbear for $1.6m (11x revenue). The latter yet another example of a SPAC being formed to carry out the merger, funded by the investment group GigFounders.

Notes: Based on share prices as at 30th June 2021; indices weighted by market capitalisation. Sources: Capital IQ and Results International analysis.

Note: EV = Enterprise Value; financials calendarised to December year end; median values reported. See the Selected Publicly Traded Companies section of this document for details of companies included in each category. Source: Capital IQ.

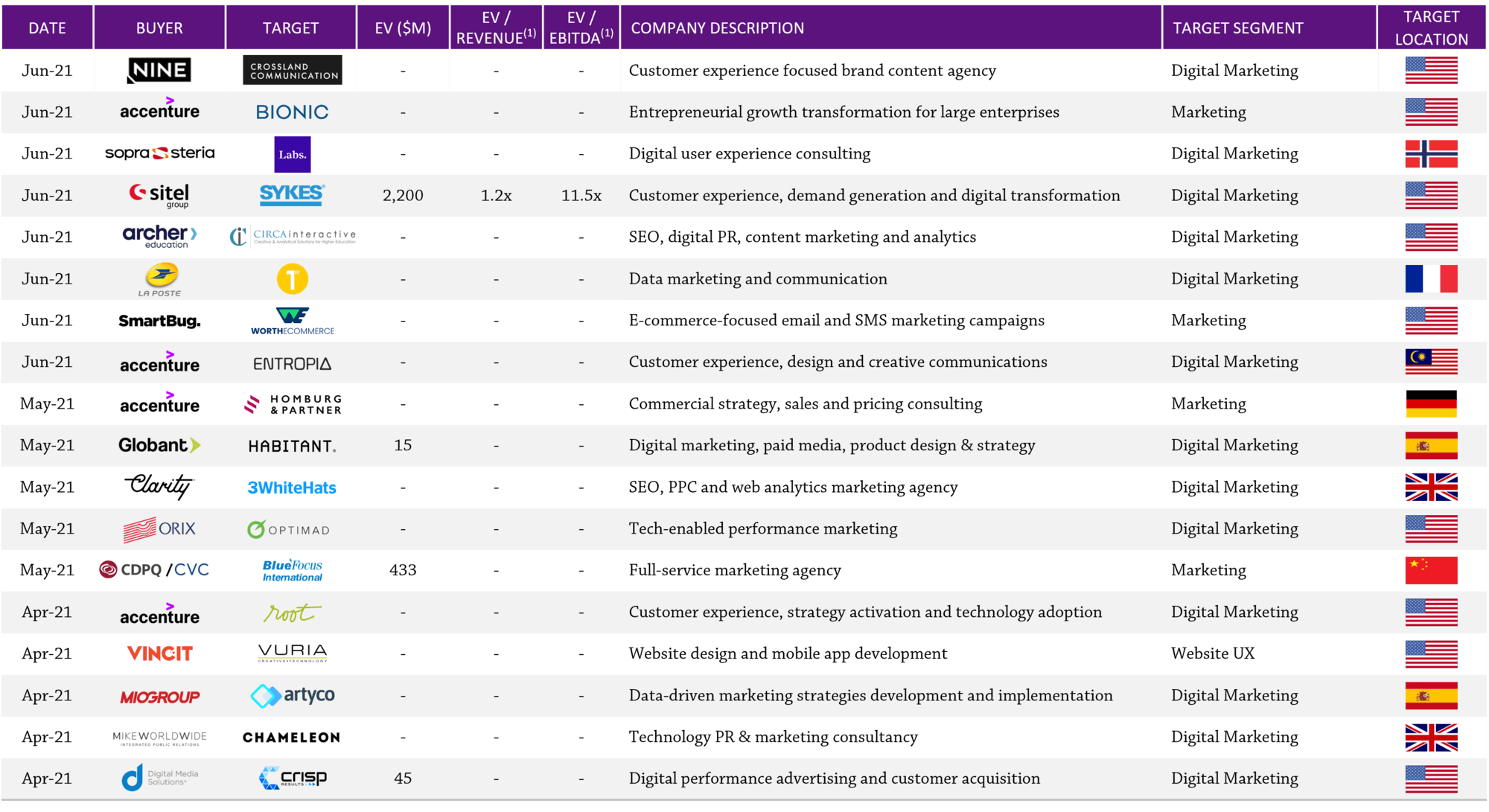

Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results International analysis.

Note: Parent shown as acquirer when acquisition made through group subsidiary / group. Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results International analysis.

(1) In certain cases EV/Revenue and EV/EBITDA are publicly reported estimates and includes deferred consideration; TTM financials have been used where possible; EV = transaction value scaled to 100% shareholding plus net debt (incl. minority interest). Note: Earnout considerations excluded in the calculation of Enterprise Value. Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results International analysis

(1) In certain cases EV/Revenue and EV/EBITDA are publicly reported estimates and includes deferred consideration; TTM financials have been used where possible; EV = transaction value scaled to 100% shareholding plus net debt (incl. minority interest). Note: Earnout considerations excluded in the calculation of Enterprise Value. Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results International analysis.

(1) In certain cases EV/Revenue and EV/EBITDA are publicly reported estimates and includes deferred consideration; TTM financials have been used where possible; EV = transaction value scaled to 100% shareholding plus net debt (incl. minority interest). Based on Mar’21E financials. Note: Earnout considerations excluded in the calculation of Enterprise Value. Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results International analysis.

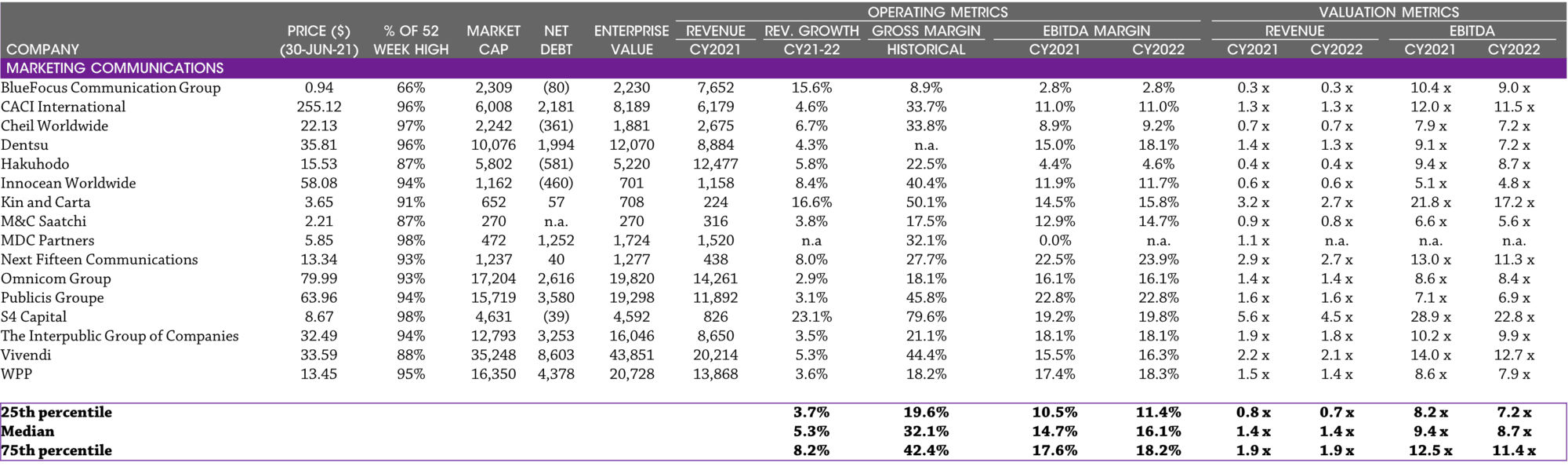

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ.

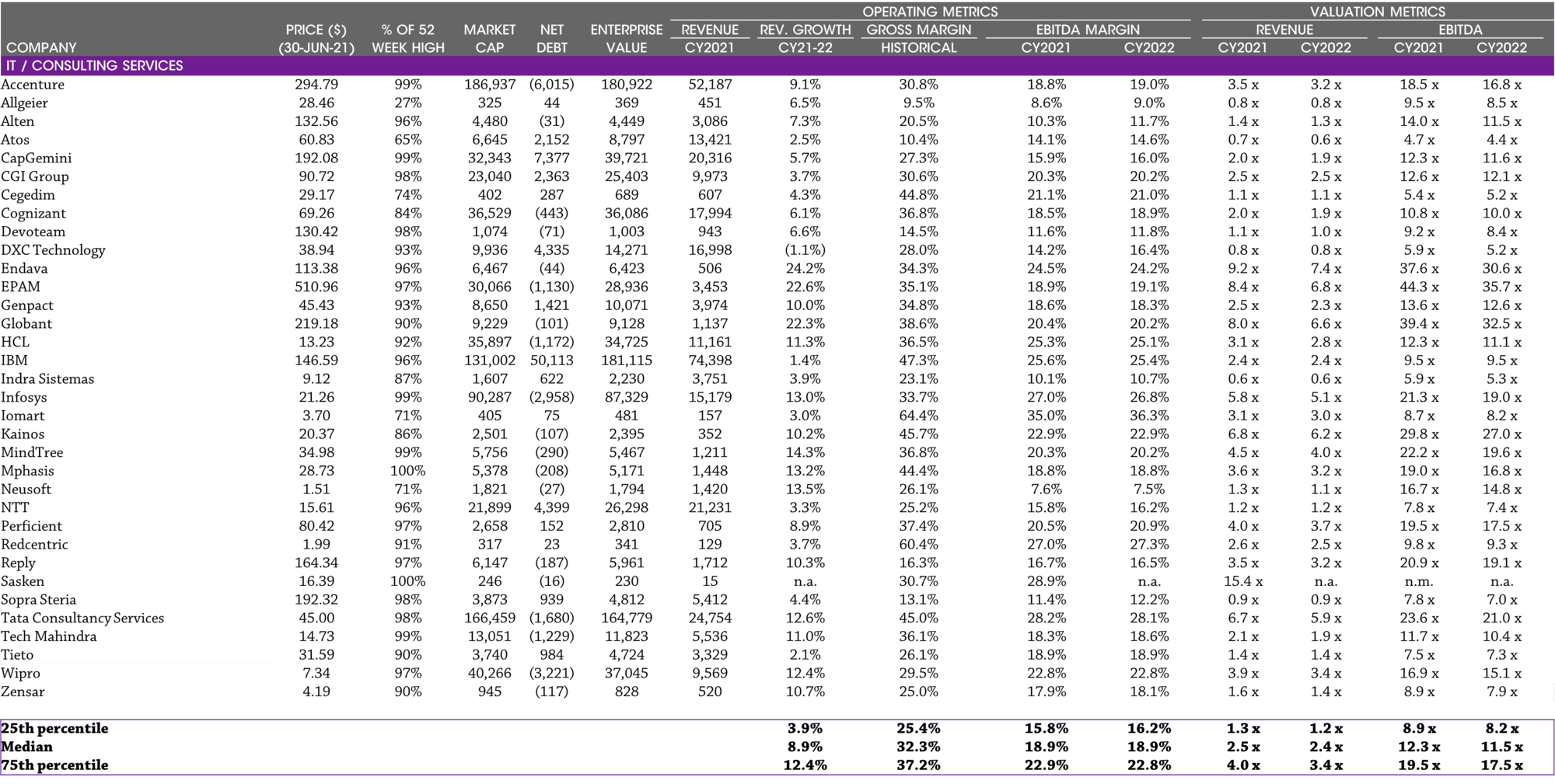

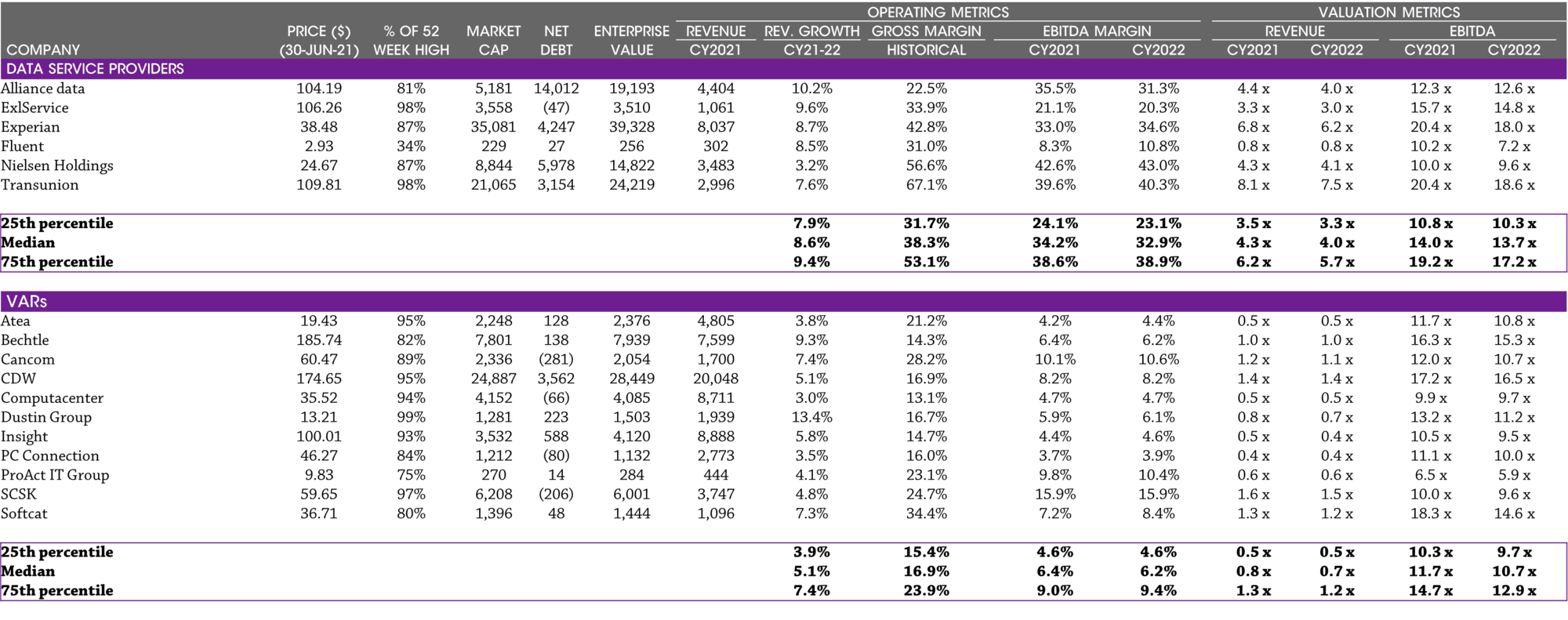

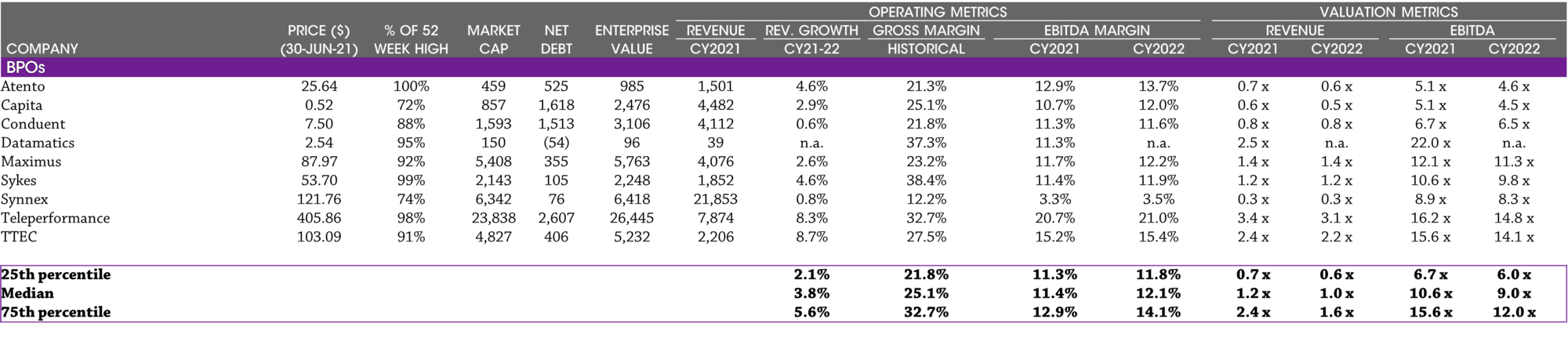

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest.Source: Capital IQ.