The enterprise software market review: Q2 2021

Welcome to the Q2 2021 edition of our Enterprise Stack Report – Results International’s quarterly market update for the enterprise software sector.

Public valuations remain high and have recovered after a slight dip in Q1 21:

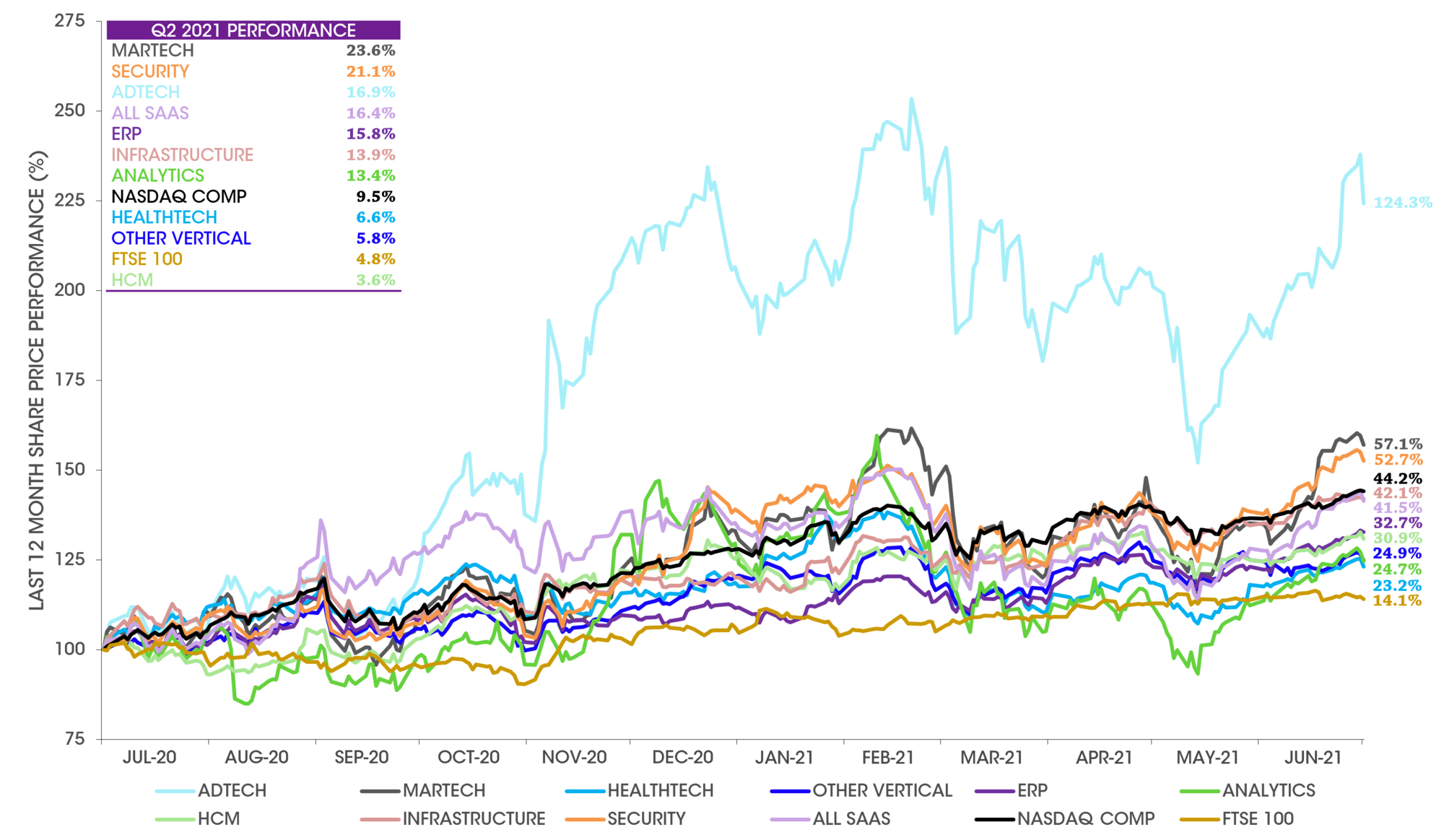

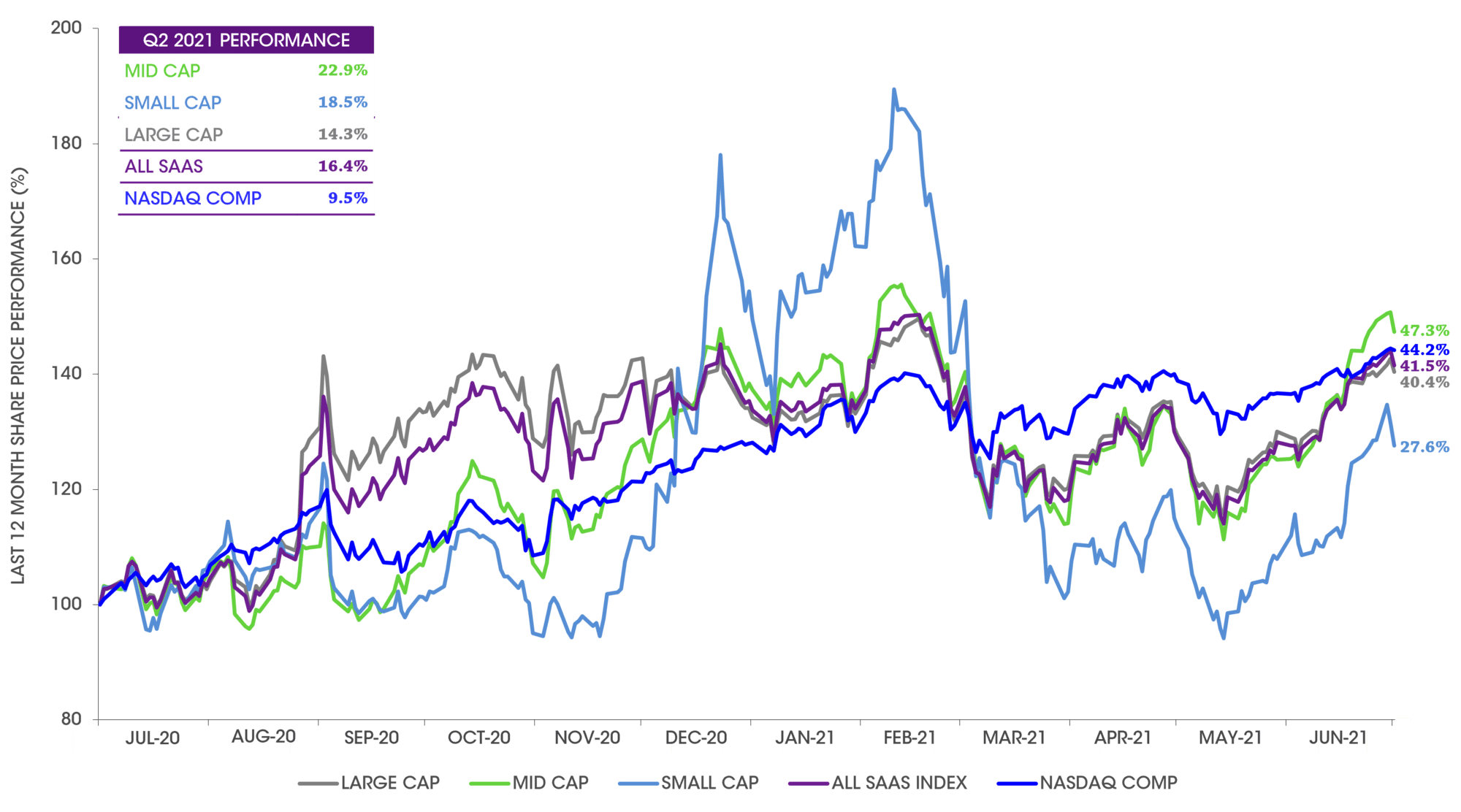

Our index of Pure Play SaaS vendors is up 16% in Q2 and this sentiment is shared across all of the other indices we track, including Martech, Adtech and Cybersecurity.

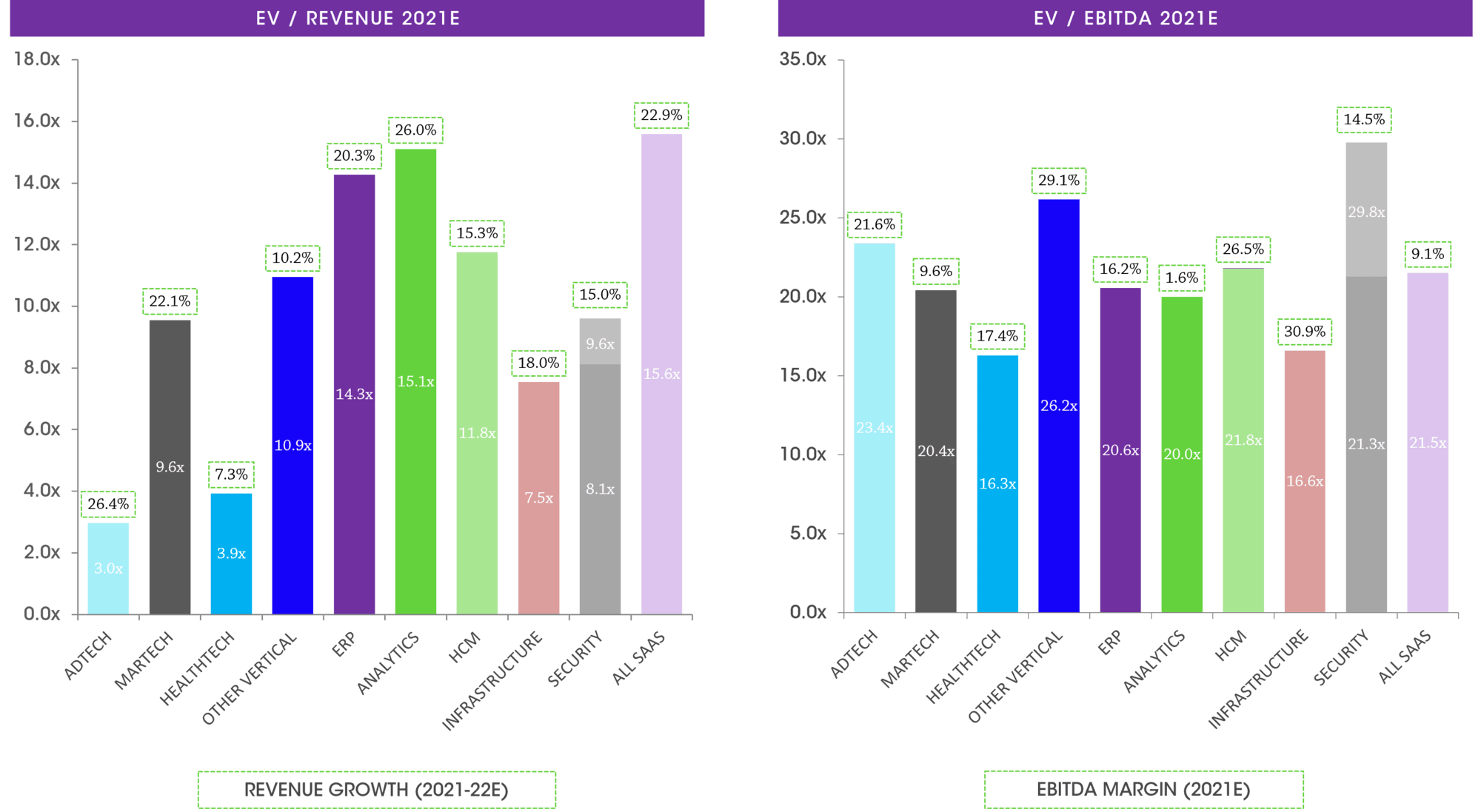

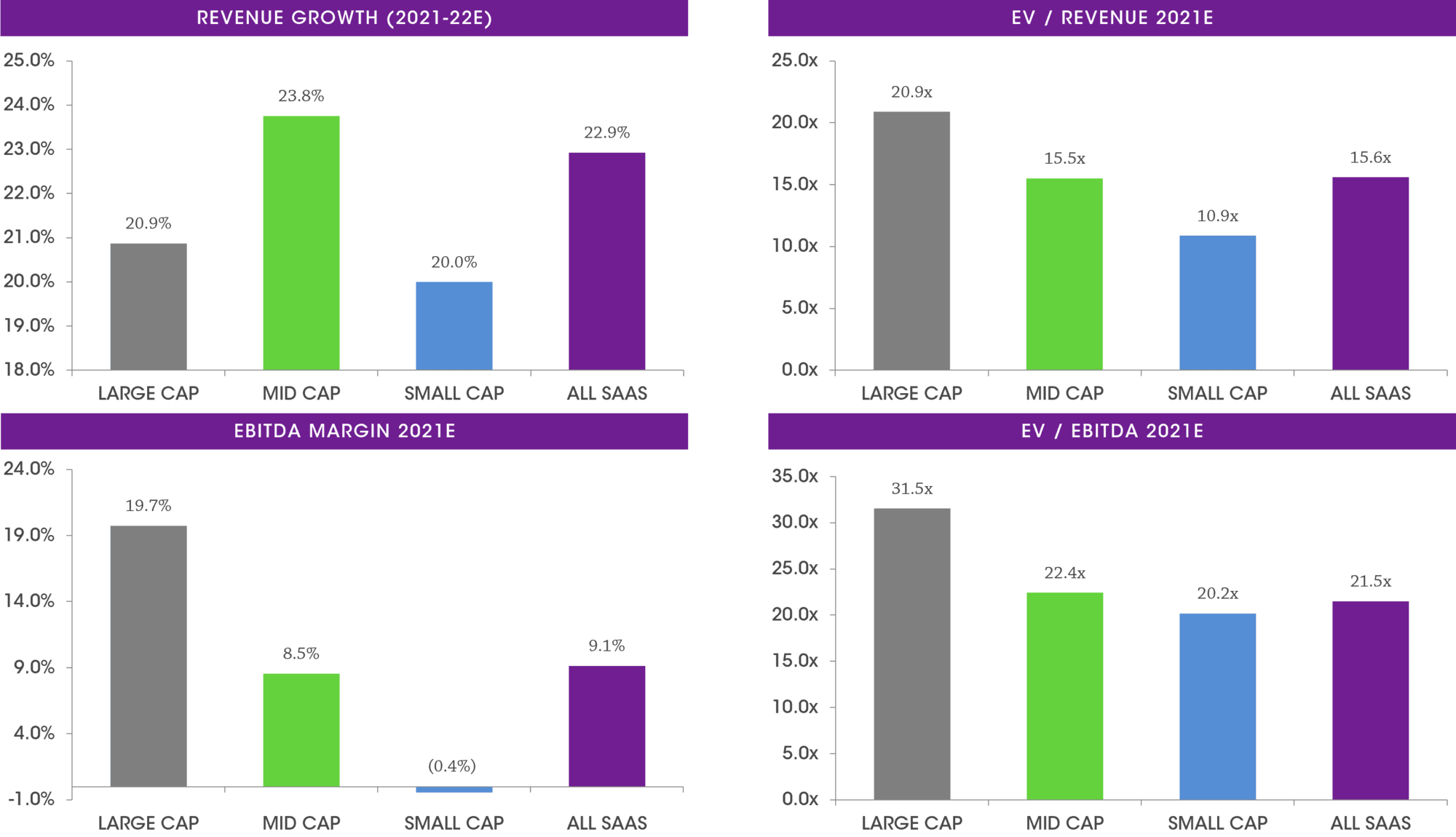

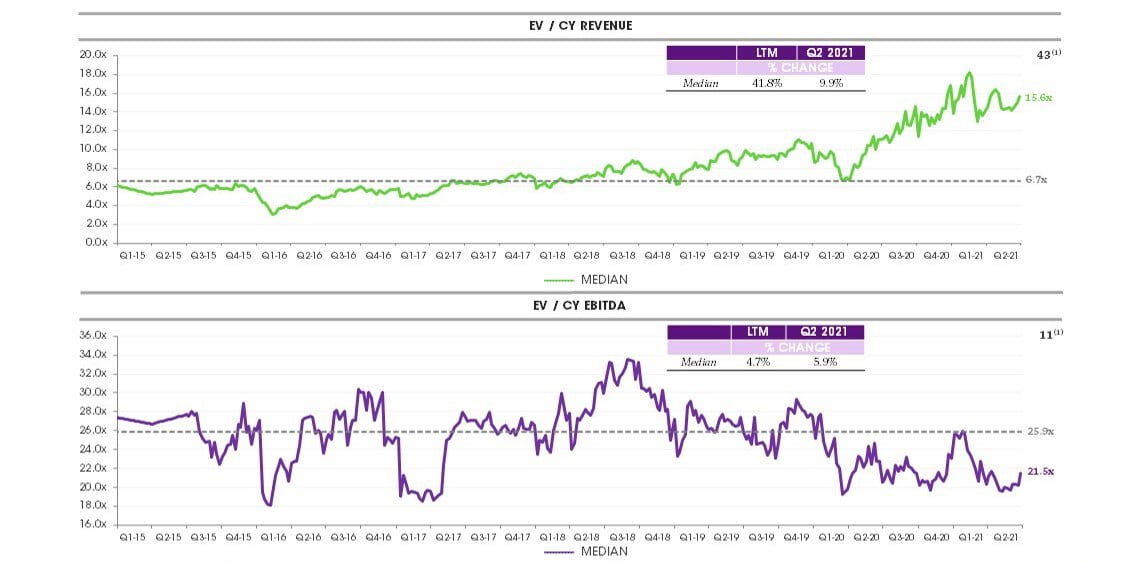

Multiples are also up in the quarter with SaaS businesses trading at a median of 15.6x revenue and 21.5x EBITDA in Q2, compared to 14.2x revenue and 20.3x EBITDA in Q1.

This positive sentiment is also reflected in the flurry of IPOs in Q2 with twelve across our sectors including three in Adtech (AppLovin, DoubleVerify and Integral Ad Science), three in Martech (Sprinklr, SquareSpace and Zeta Global) and others in ERP, Analytics, Infrastructure and Healthtech (Confluent, WalkMe, Similarweb, UiPath, Monday.com and Suse).

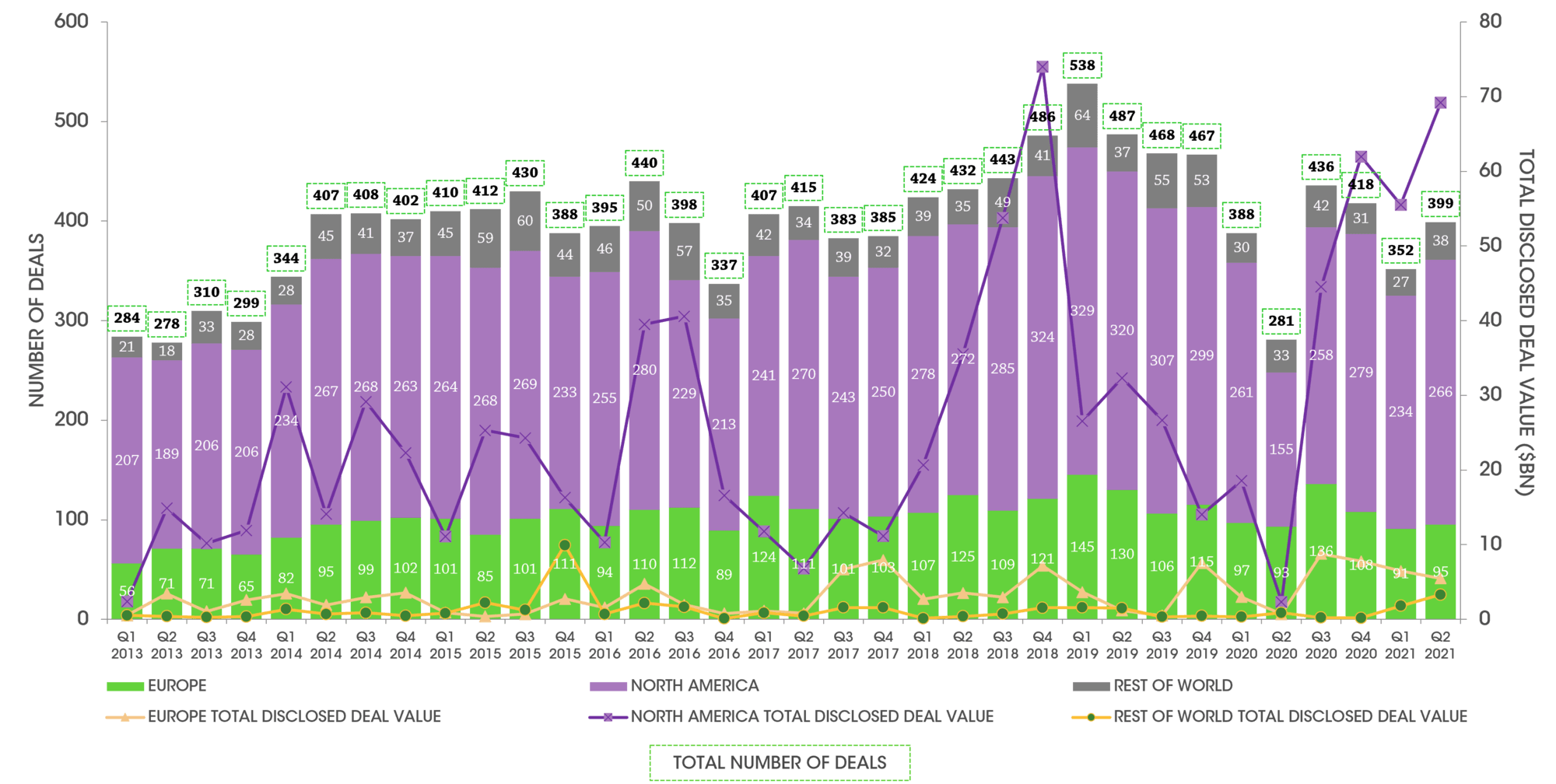

Deal flow continues to be very strong, with deal volumes climbing back to Q3 and Q4 2020 levels and up nearly 15% on Q1 21, with 400 transactions in the quarter and an abundance of scaled deal activity; 47 out of the 400 deals transacted at a value greater than $100m and 19 of them at a value greater than $1bn.

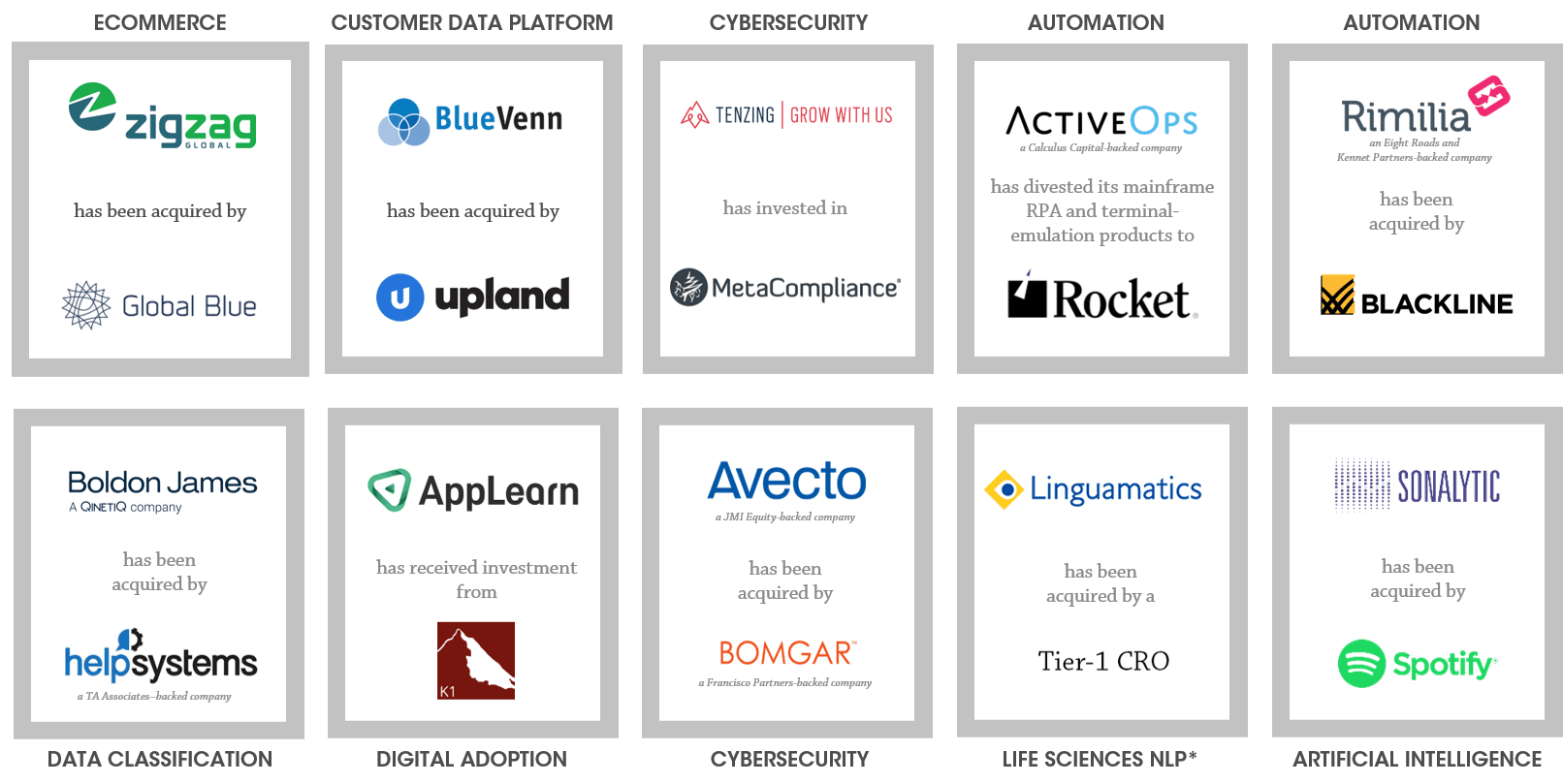

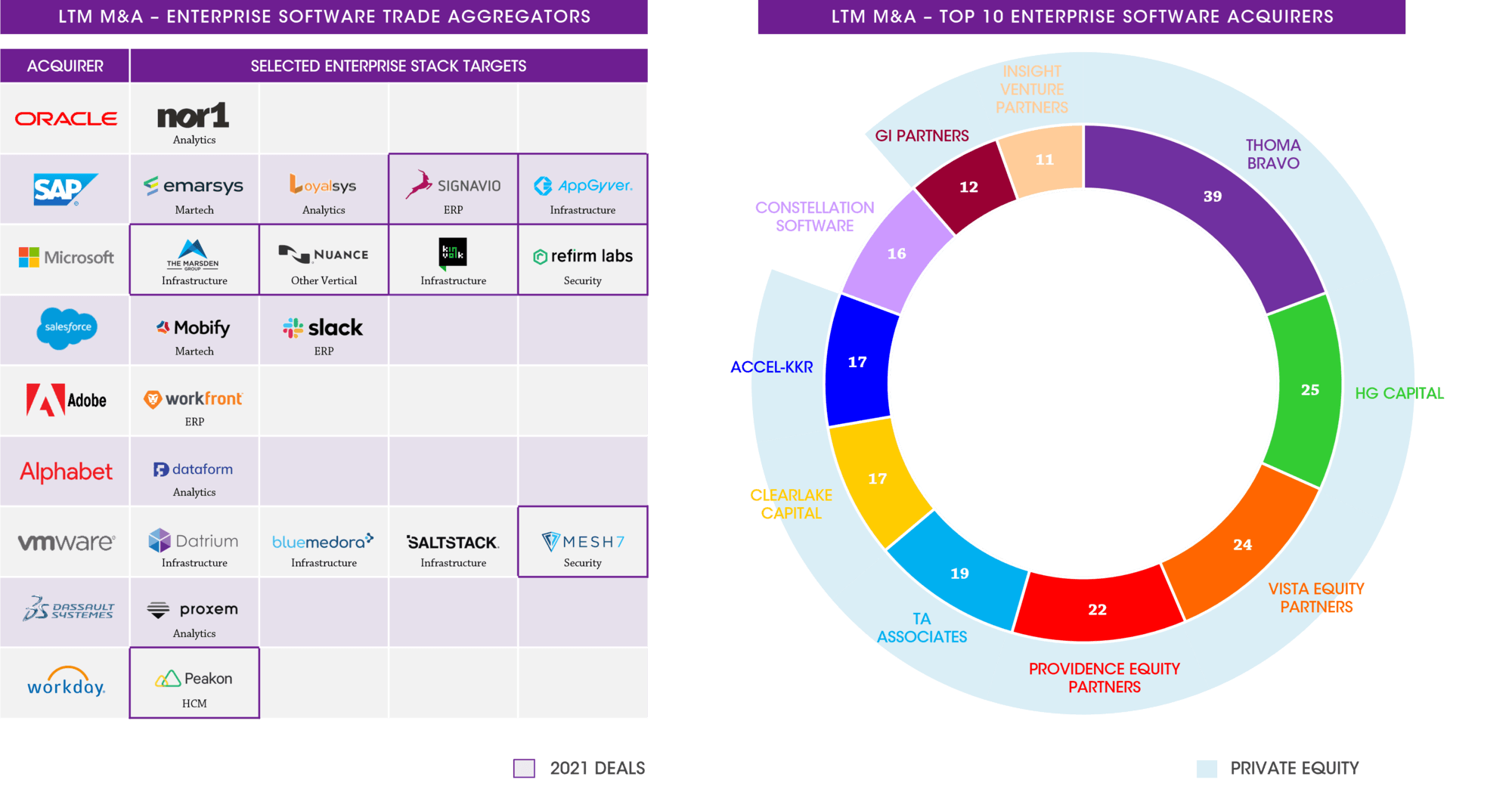

As has been the case for many quarters, private equity continues to dominate with Constellation Software the only strategic to figure in our top 10 most acquisitive in the last 12 months.

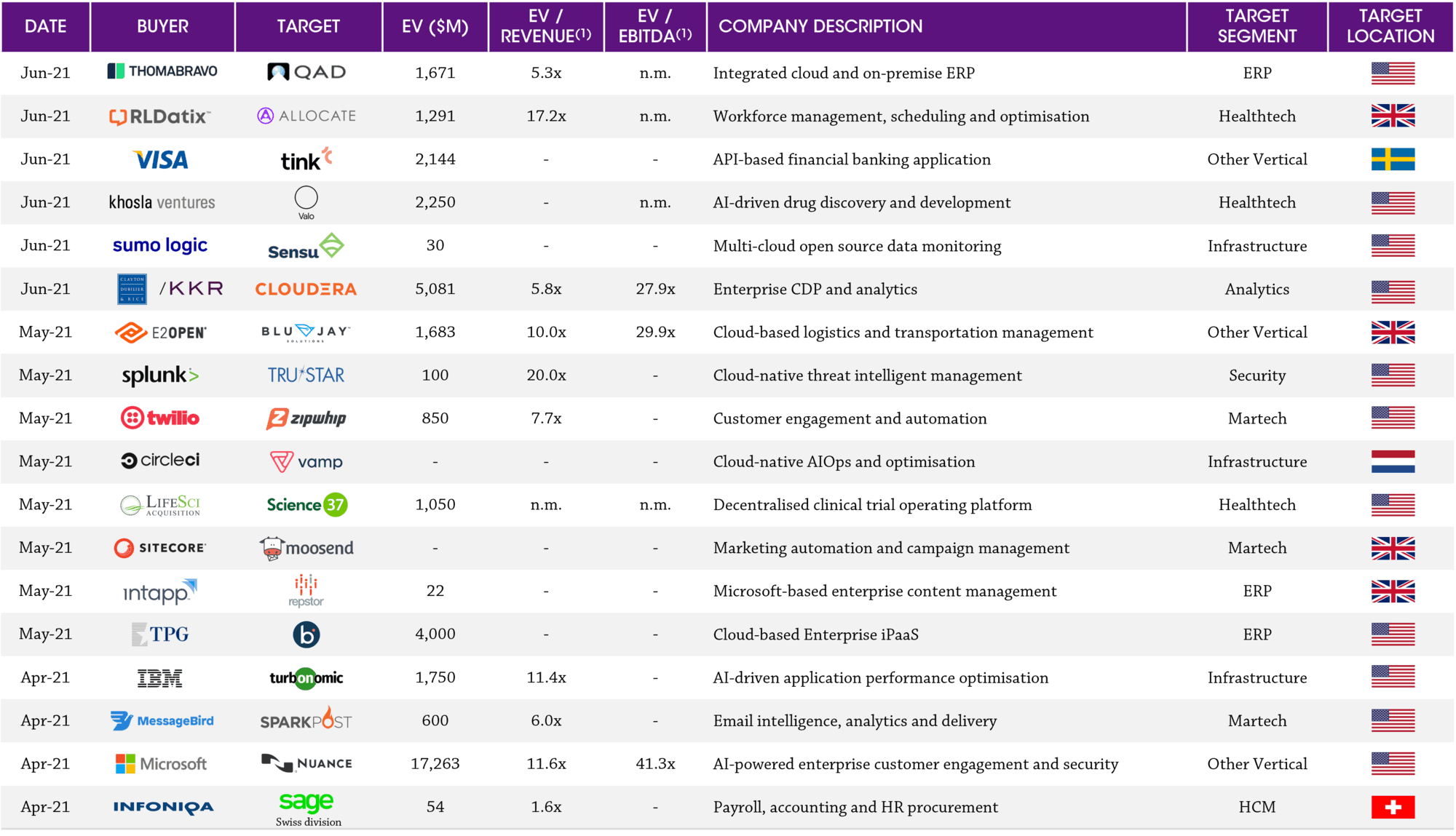

Led by Thoma Bravo, HgCapital and Vista (investing either directly or via their portfolio companies), the transactions of note this quarter include Thoma Bravo’s investment in QAD (US-based ERP software provider) for $1.7bn (5.3x revenue) and KKR in consortium with Clayton, Dubilier & Rice investing in Cloudera (US-based CDP provider) for just over $5bn (c. 6x revenue). QAD is yet another example of a PE go-private ERP deal following in the footsteps of Unit4 and ACS.

Within Europe, HgCapital also played the role of a seller disposing of Allocate Software for $1.3bn to US-based healthcare GRC software provider RLDatix. Allocate had been with HgCapital since 2018 and is one of the largest UK-based Healthtech providers.

*Natural Language Processing

Notes: Based on share prices as at 30th June 2021; indices weighted by market capitalisation. Sources: Capital IQ and Results International analysis

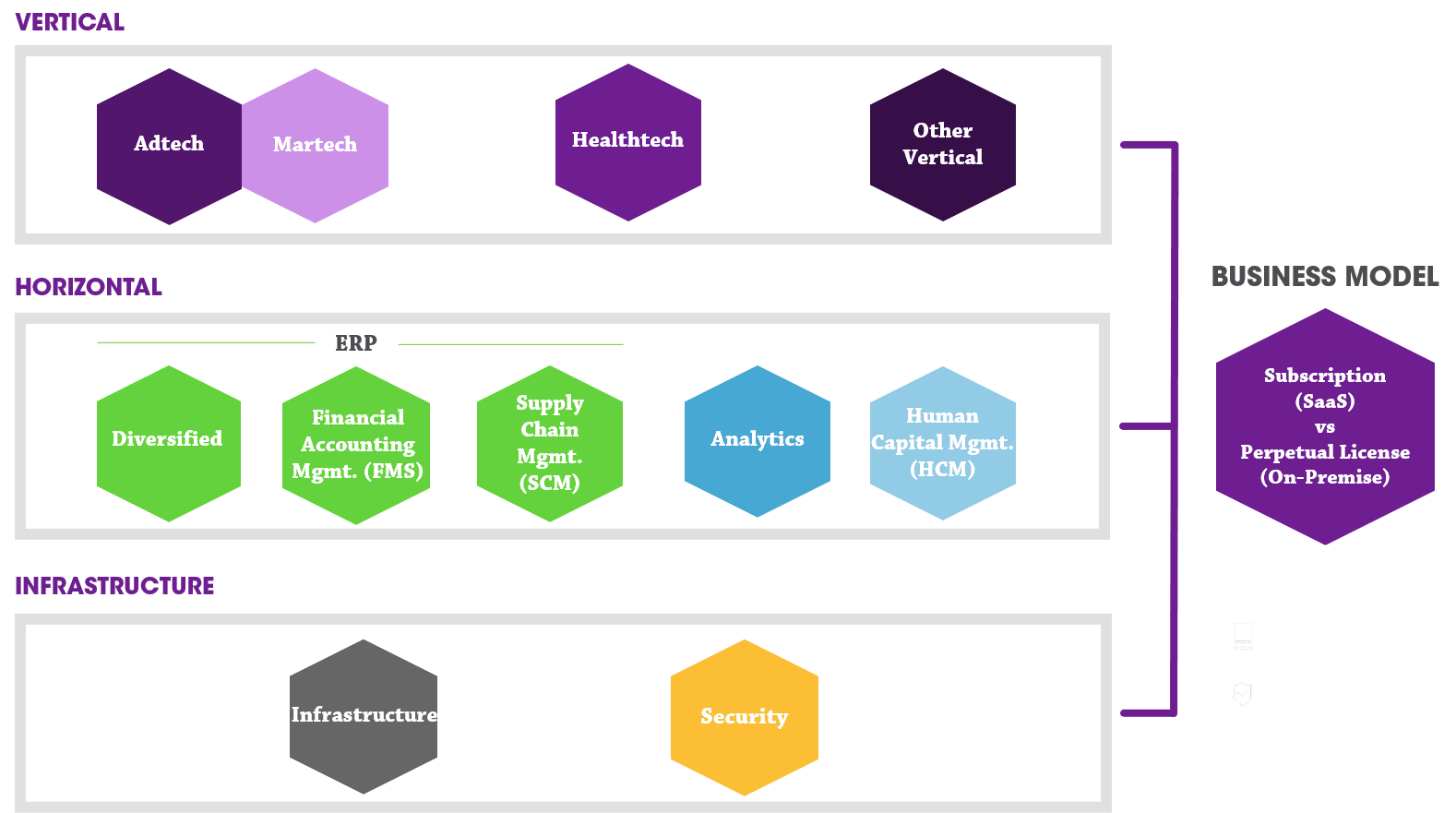

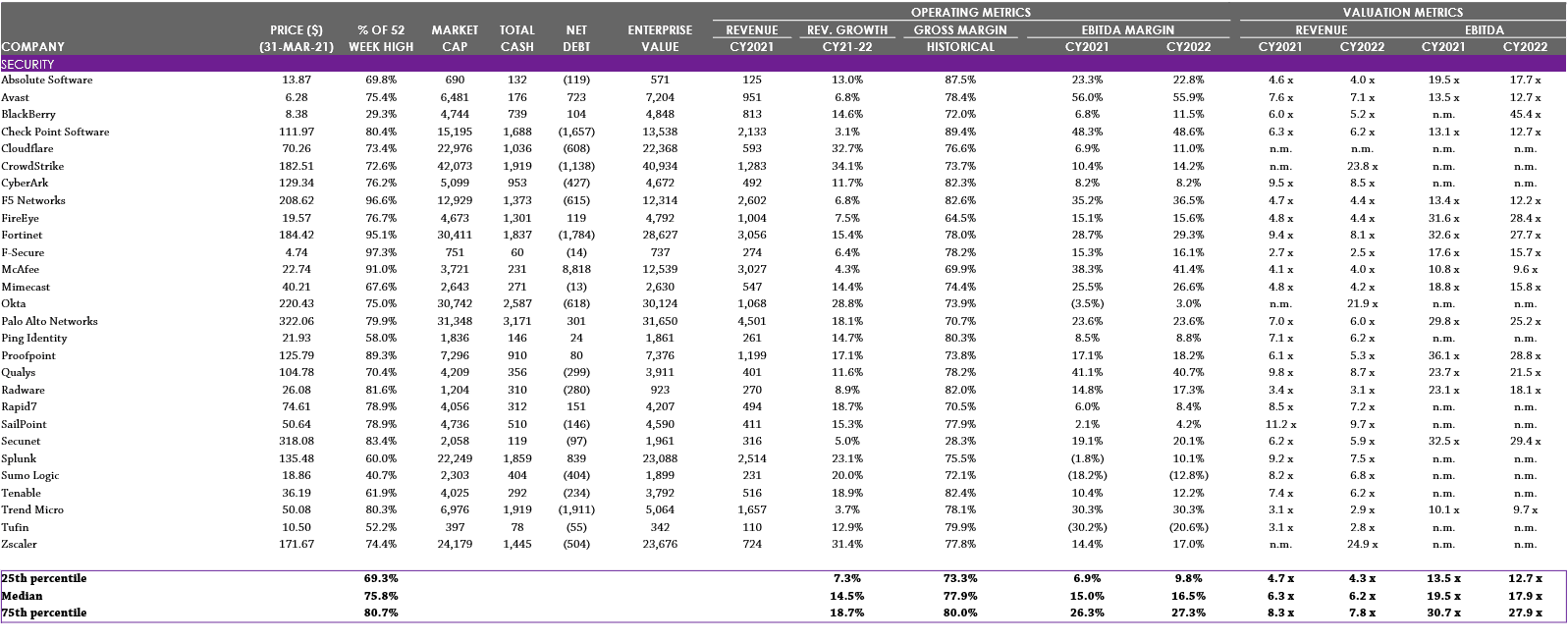

Note: For Security, 75th percentile values have been overlaid (shaded lighter) to illustrate next-generation vendors. Note: EV = Enterprise Value; financials calendarised to December year end; median values reported. See Selected Publicly Traded Companies (click here) for details of companies included in each category. Source: Capital IQ

Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results International analysis.

Note: PE also shown as acquirer when acquisitions made through portfolio company; parent also shown as acquirer when acquisition made through group subsidiary/ group. Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results International analysis.

1) In certain cases EV/Revenue and EV/EBITDA are publicly reported estimates; TTM financials have been used where possible; EV = transaction value scaled to 100% shareholding plus net debt (incl. minority interest). Note: Earnout considerations excluded in the calculation of Enterprise Value. Sources: Press releases, 451 Research and Results International analysis.

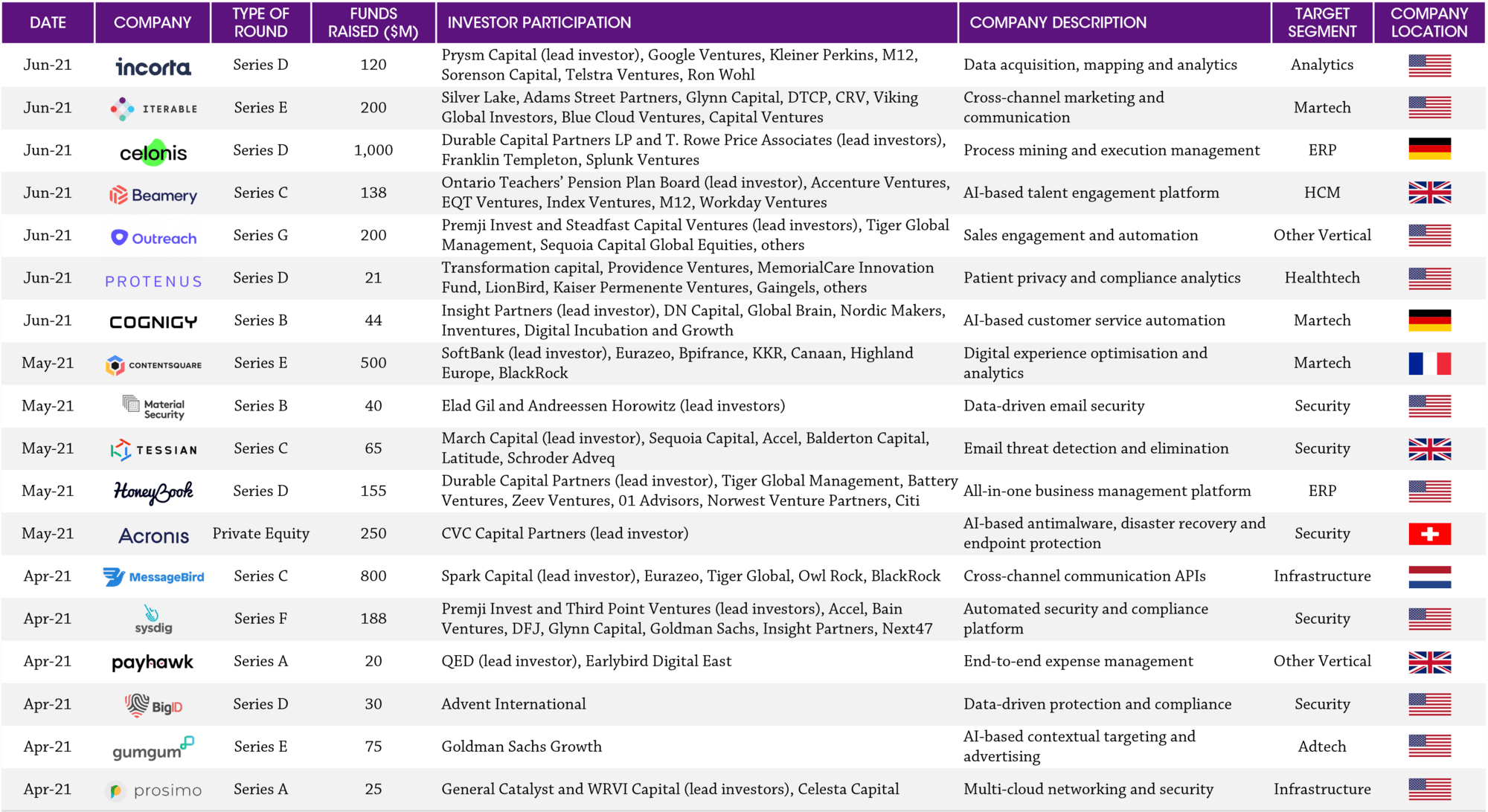

Sources: Pitchbook, Press releases, Crunchbase and Results International analysis

Notes: Based on share prices as at 30th June 2021; indices weighted by market capitalisation. Sources: Capital IQ and Results International analysis.

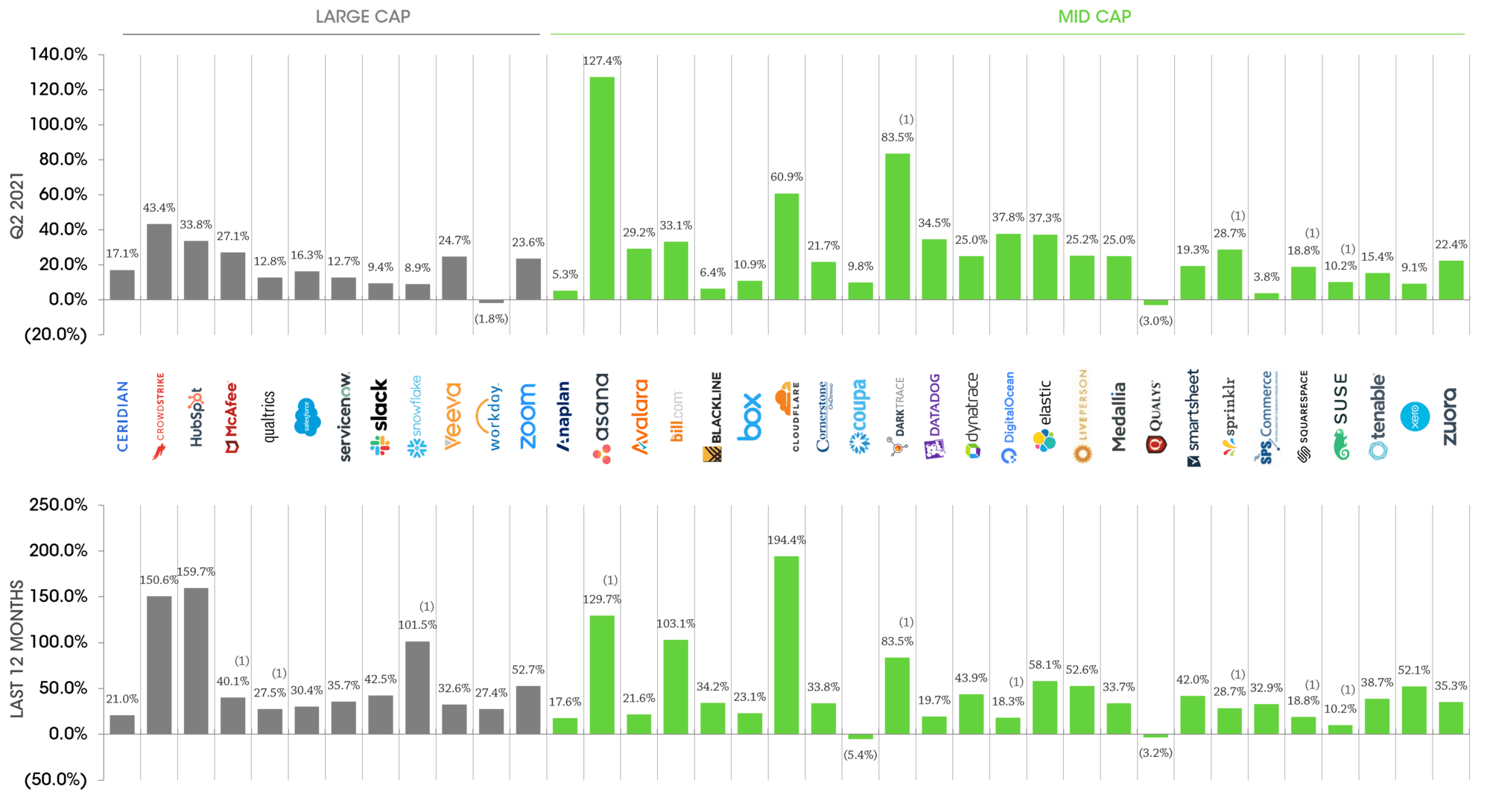

1) These companies IPO’d within the last 12 months/last quarter, the share price movement represents the change between the stock’s IPO date and 30th June 2021. Note: Based on share prices as at 30th June 2021. Sources: Capital IQ and Results International analysis.

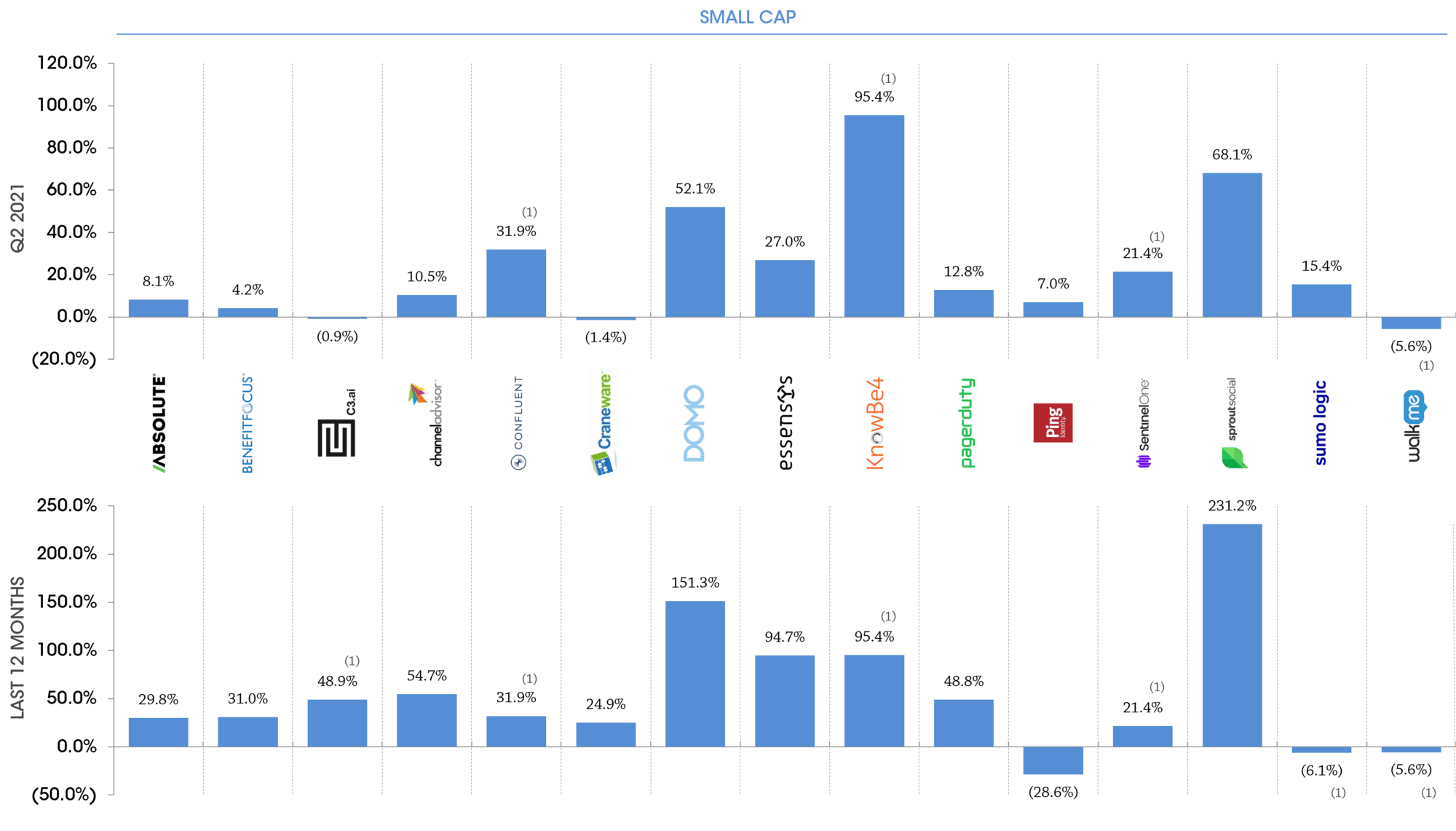

(1) These companies IPO’d within the last 12 months, the share price movement represents the change between the stock’s IPO date and 30th June 2021. Note: Based on share prices as at 30th June 2021. Sources: Capital IQ and Results International analysis.

(1) All SaaS represents the median of all stocks in Large Cap, Mid Cap and Small Cap, with no weighting applied. Notes: EV = Enterprise Value; financials calendarised to December year-end; median values reported. See Selected Publicly Traded Companies (click here) for details of companies included in each category. Sources: Capital IQ and analyst reports.

(1)Number of companies with applicable multiples in Q2 2021 index. Notes: EV = Enterprise Value; financials calendarised to December year-end, which can impact the multiples at the start of each year as the base is shifted forward; weekly tracking of valuation multiples commenced in July 2015, October 2014 – June 2015 tracked on a quarterly basis, therefore a linear progression has been assumed between quarters up to July 2015. Dotted line represents median since data has been tracked. Source: Capital IQ.

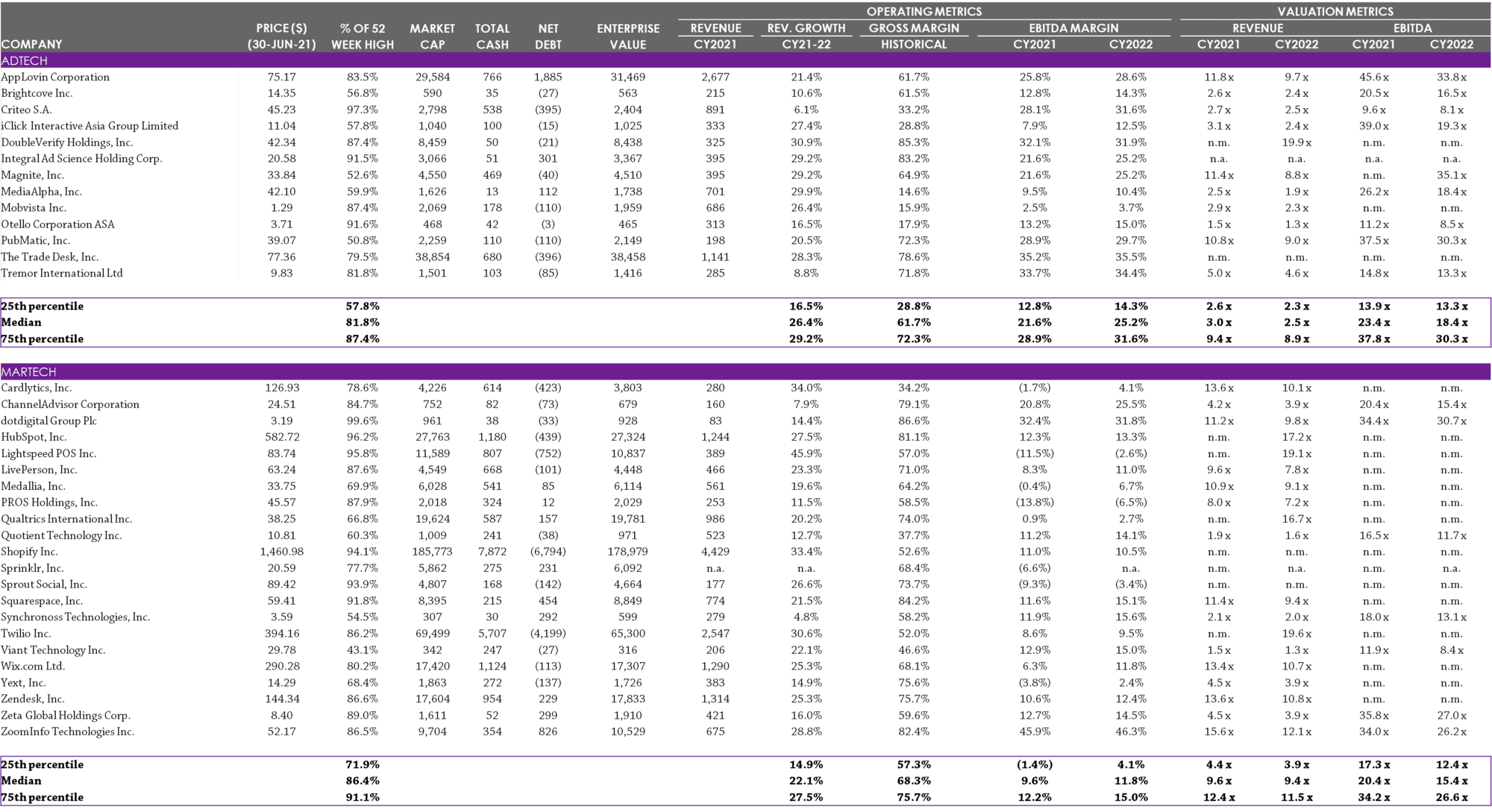

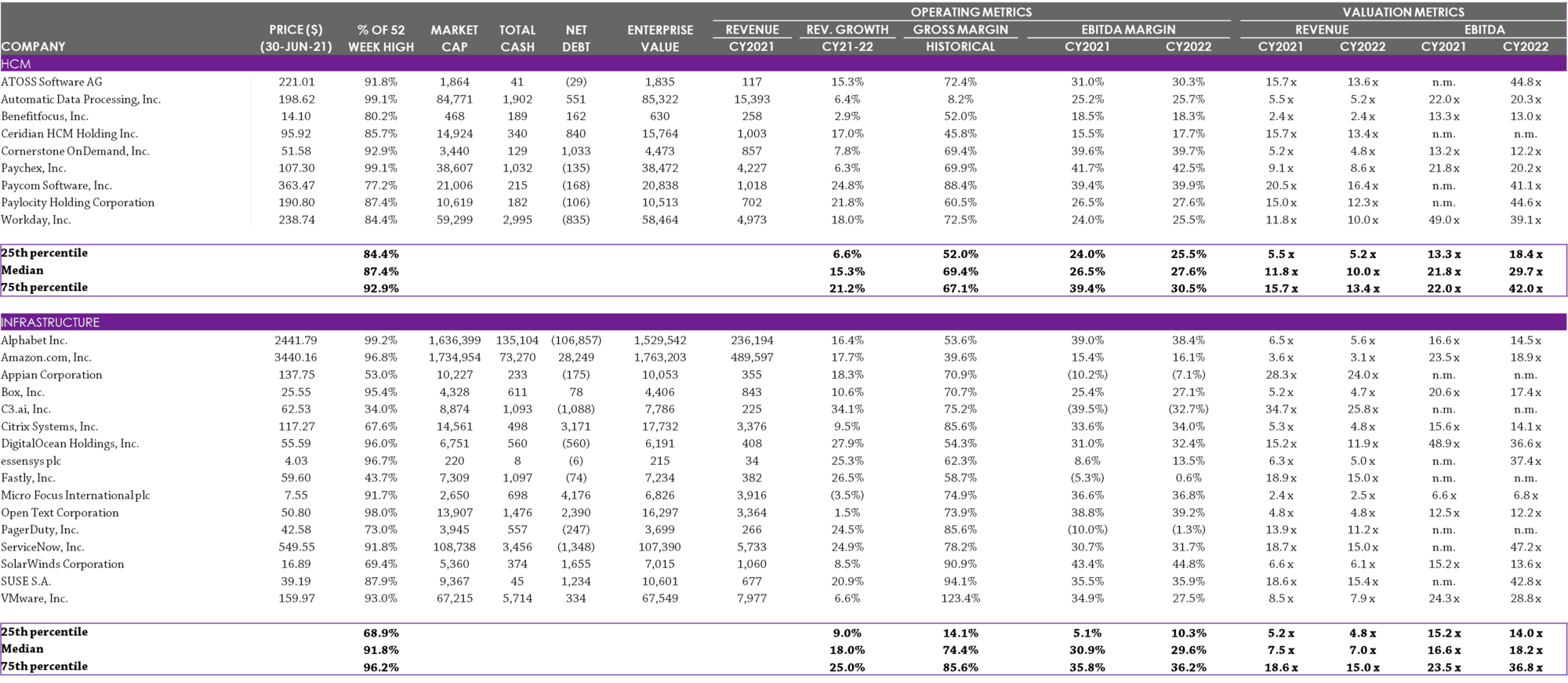

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ, broker reports.

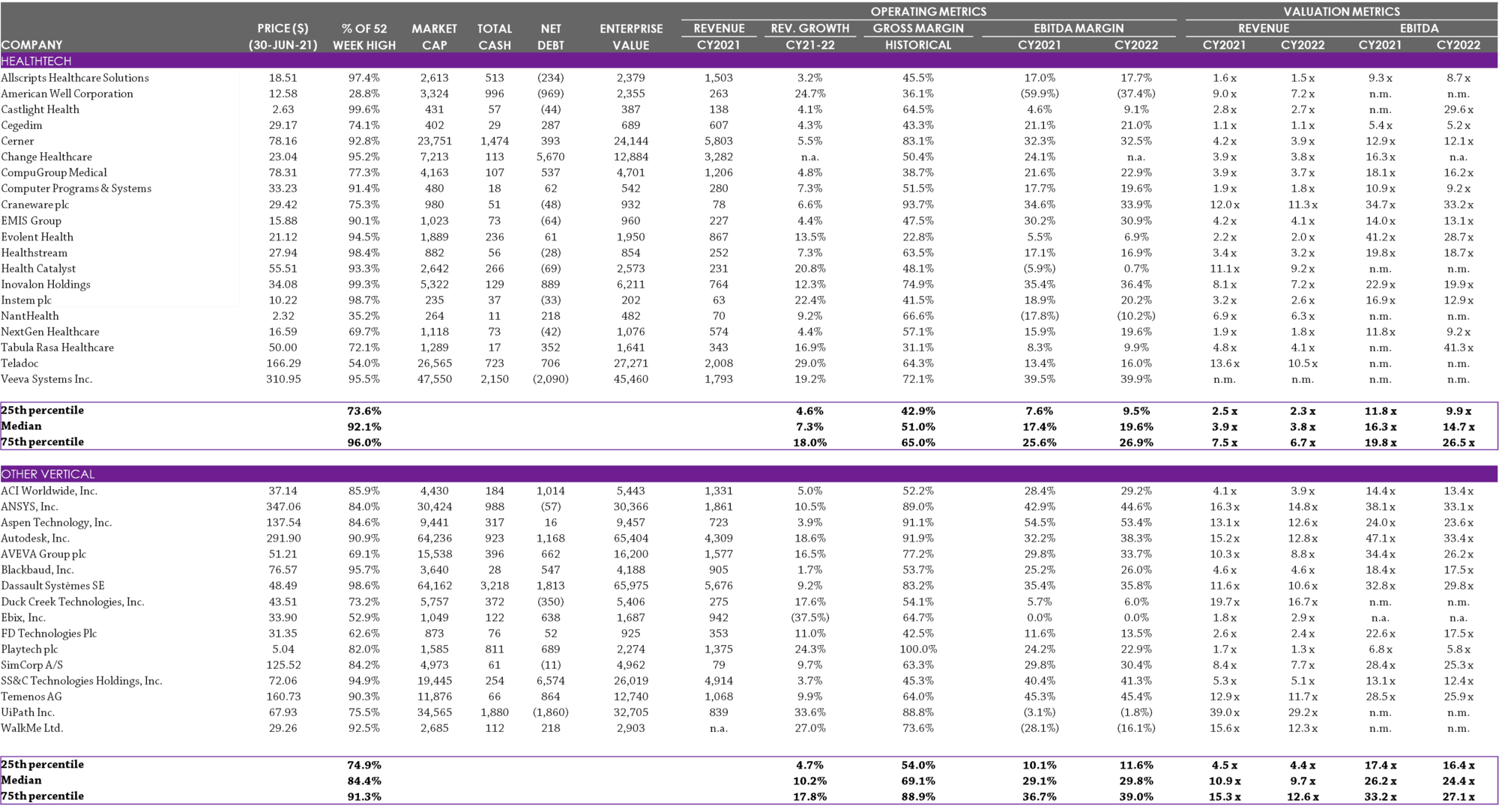

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ.

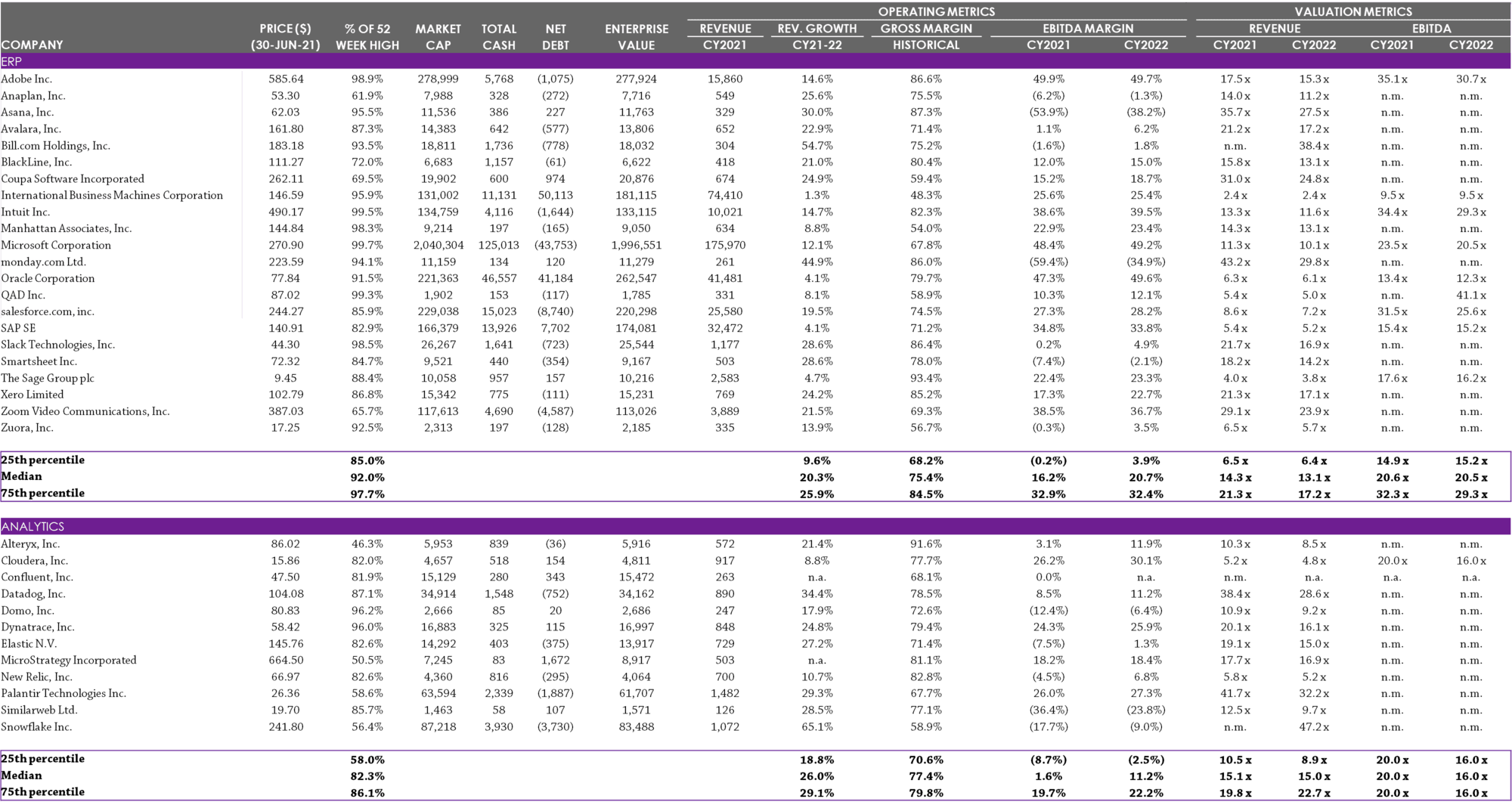

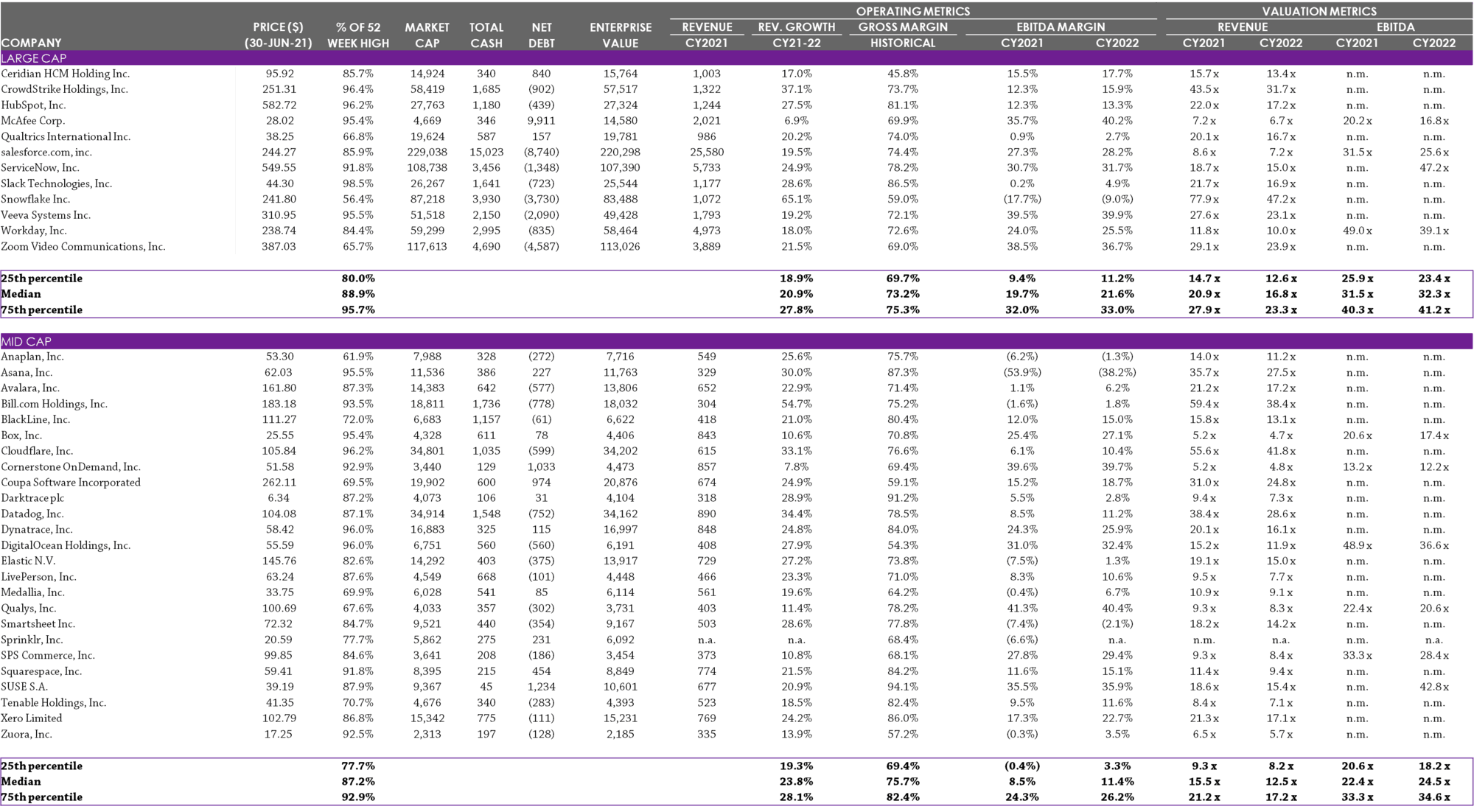

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 25x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ.

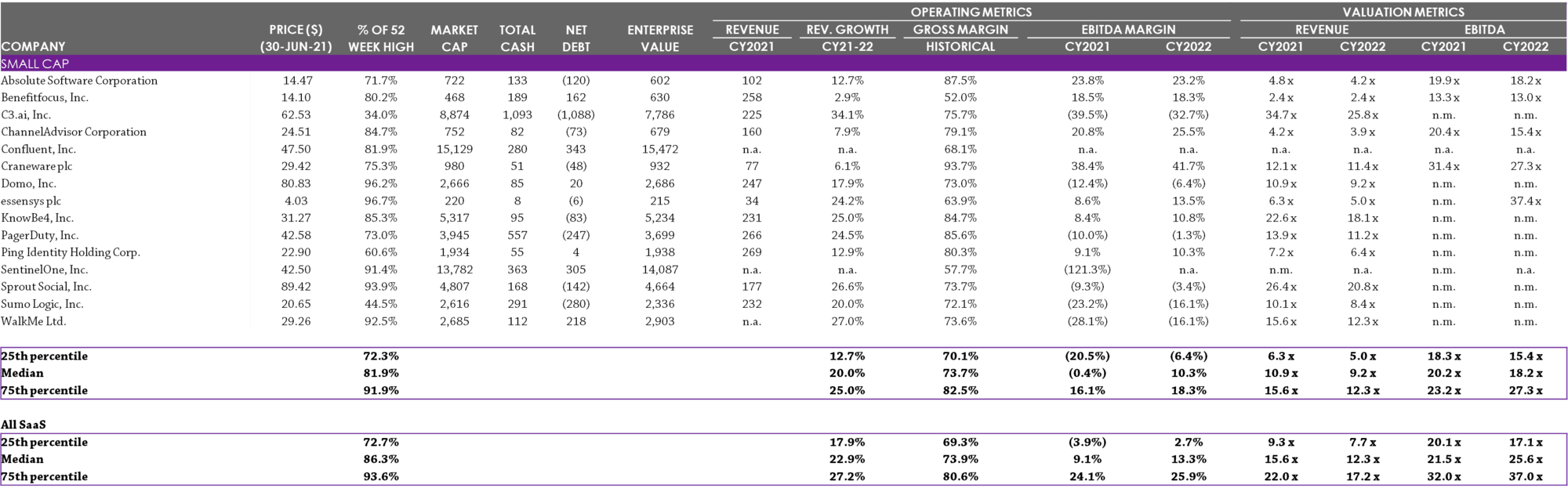

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 100x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Note: Market cap classifications categorised by CY2021E revenue: Large Cap: revenues greater than $900m; Mid Cap: revenues between $300m and $900m; Small Cap: revenues less than $300m. Source: Capital IQ.