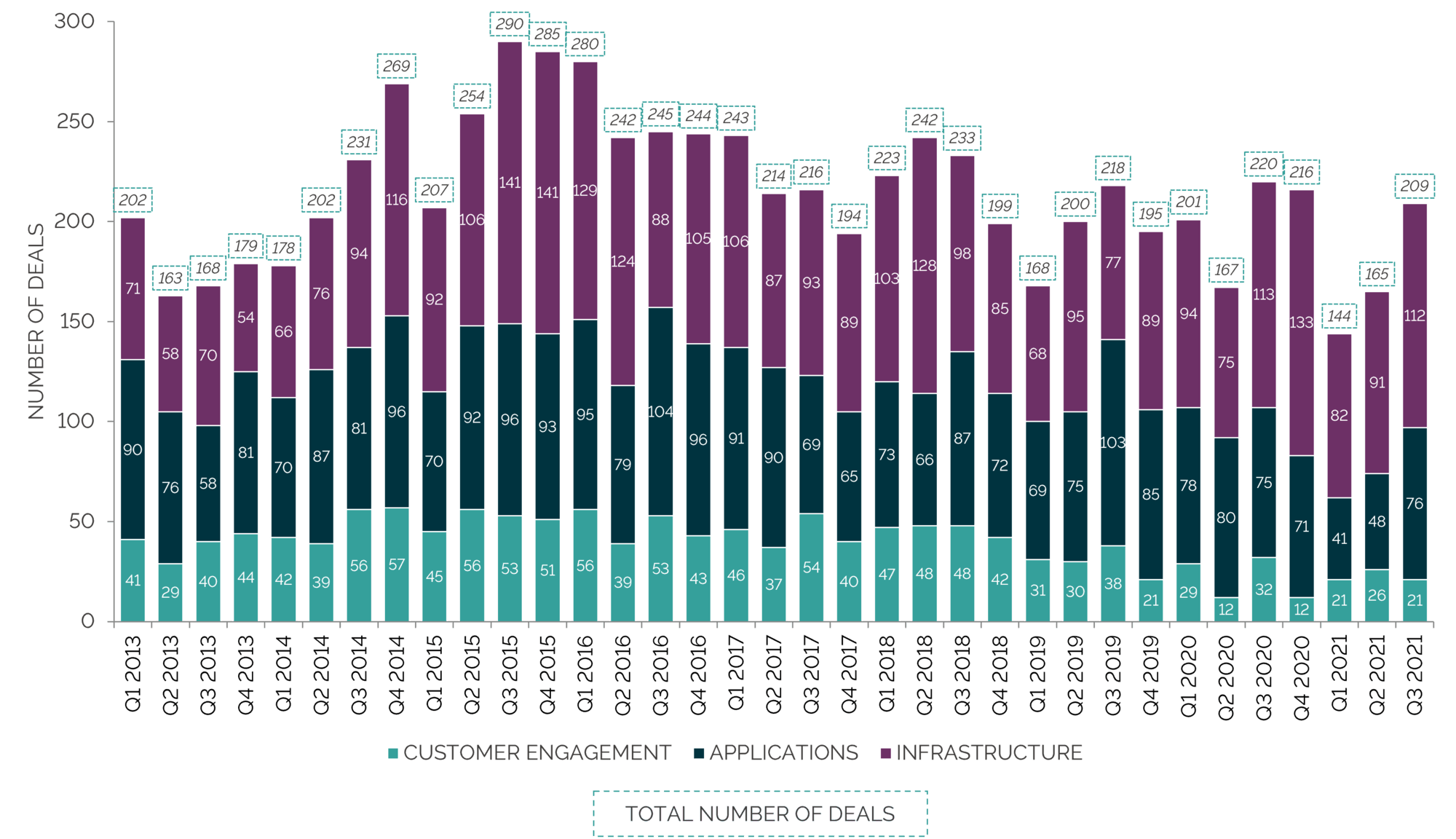

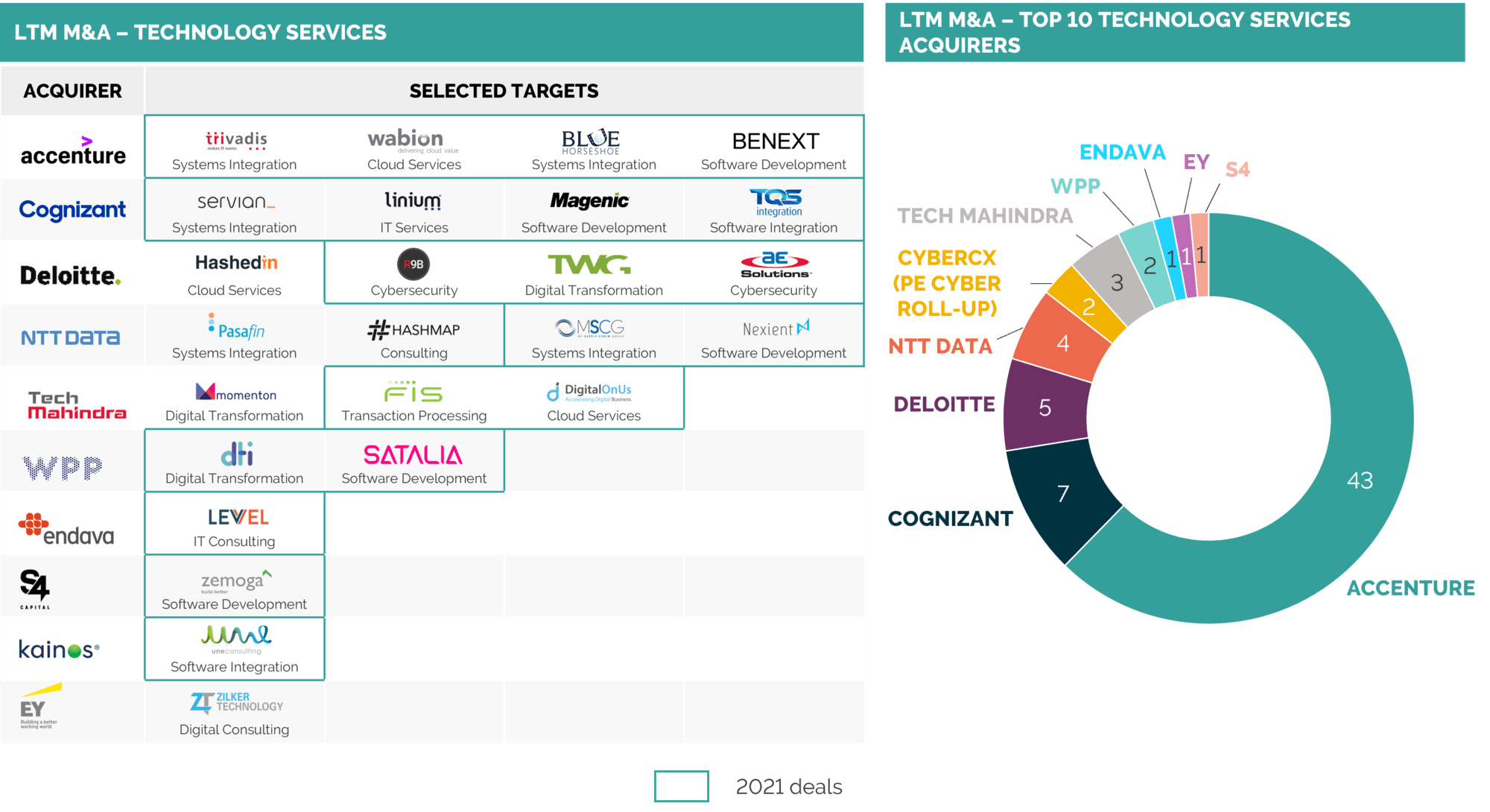

Deal activity this quarter continues to be driven by strong confidence in acquiring capability in next gen, modernisation and cloud-first tech stacks, and premium services. Equally, capturing the end-to-end digital transformation value chain continues to be a key M&A theme to become the strategic operator and engineering partner of choice for large-scale budgets

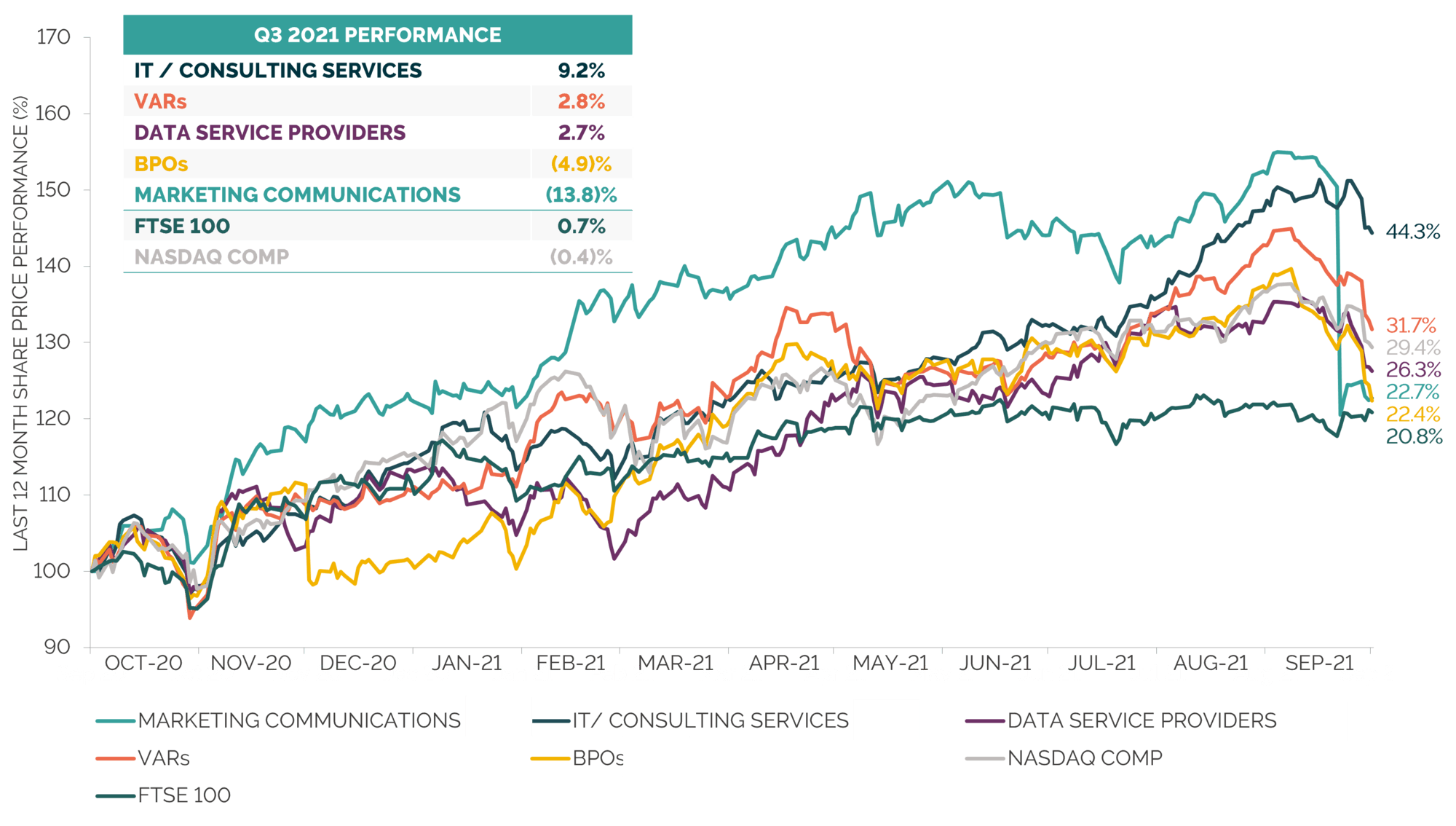

Public tech companies continue to track the NASDAQ’s trajectory over the past 12 months. Despite a small dip towards the end of the quarter, driven by macro factors, rising rates and concerns over inflation, the indices have outperformed the FTSE 100 by up to c.20% and are overall tracking c.20%-45% ahead of the share price in September 2020

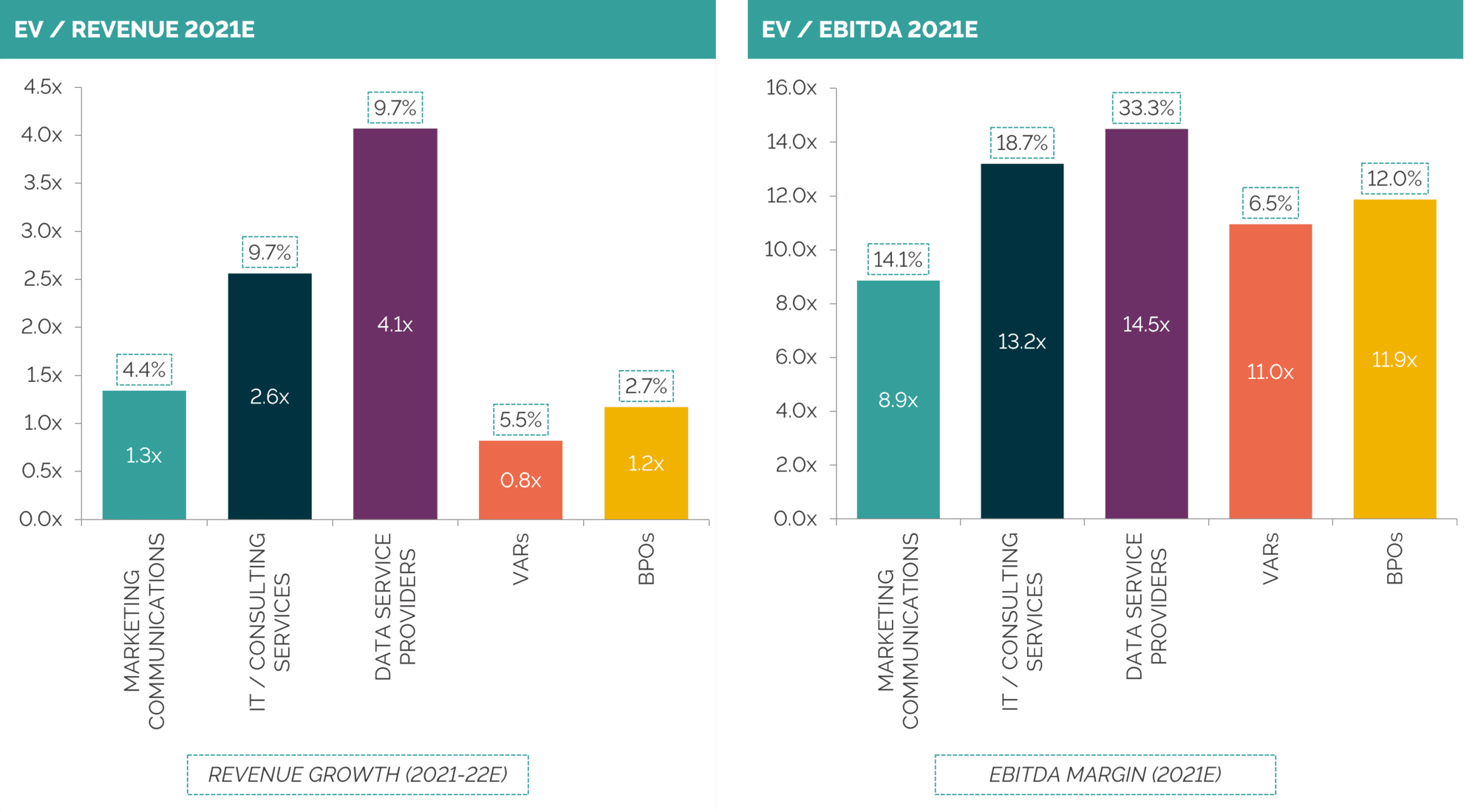

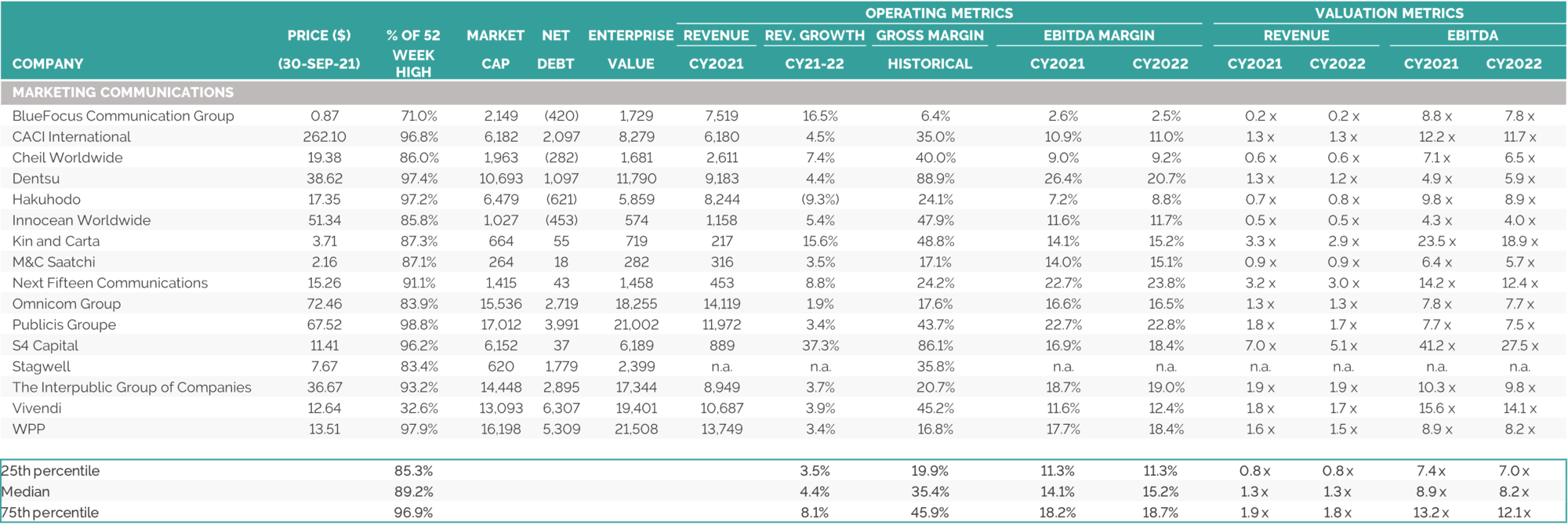

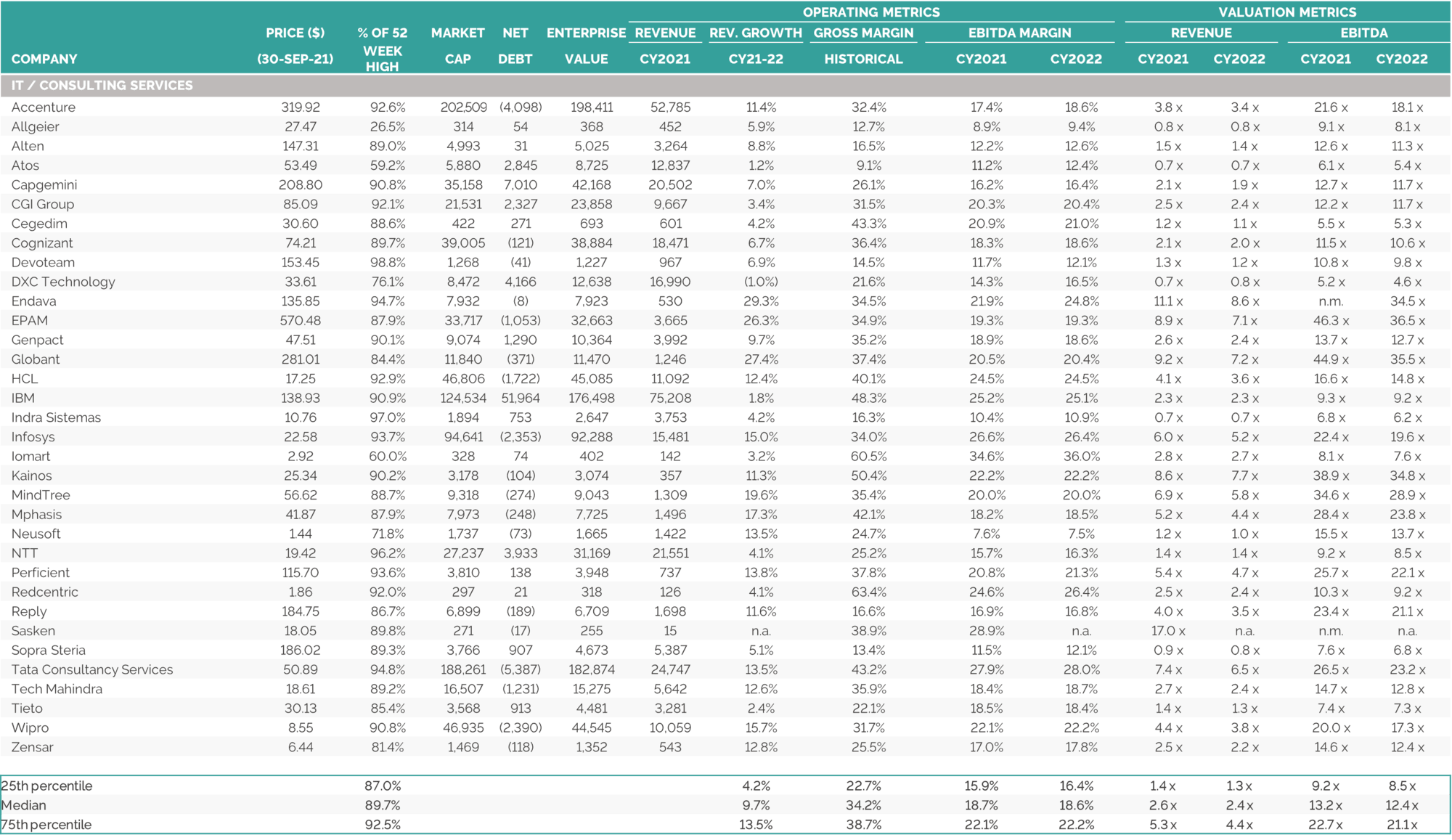

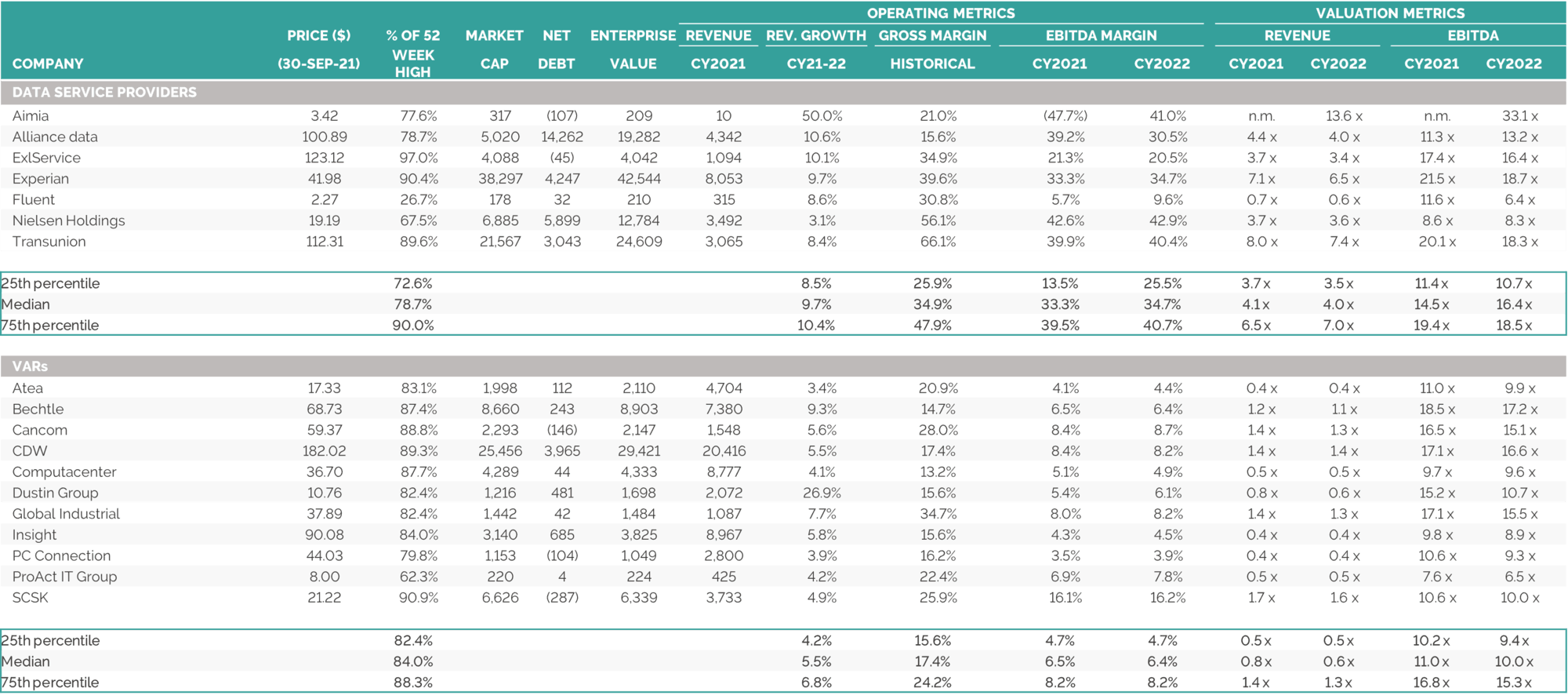

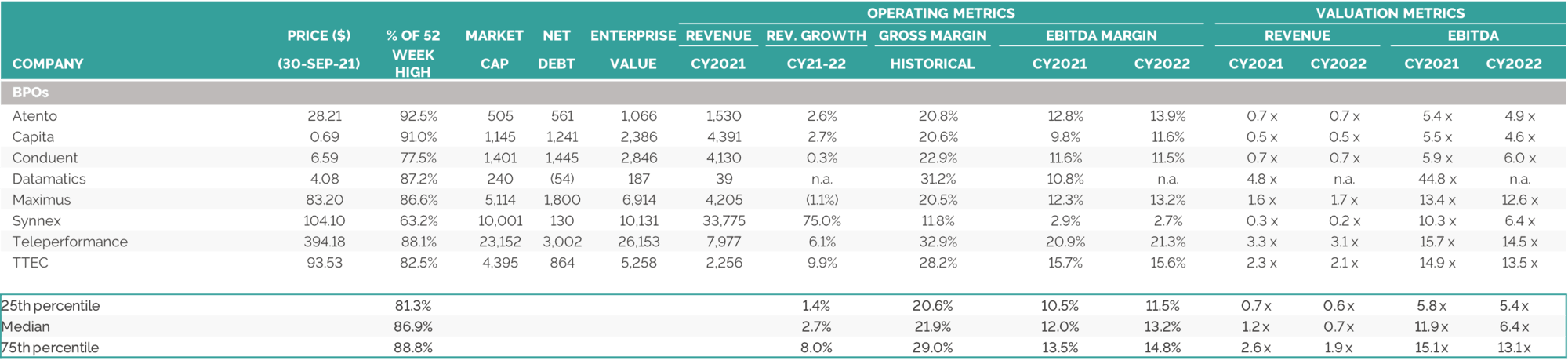

Median EV/EBITDA multiples have remained strong in Q3, largely trading in excess of 10x, with Data Service Providers (14.5x), IT / Consulting Services (13.2x) and BPOs (11.9x) indices leading the trend

Q3 finished strong with 209 M&A transactions, up 27% from Q2, with the application and infrastructure segments representing the bulk of M&A activity. Notably, this quarter saw remarkably more capability-focused tuck-in deals than significant multi-billion dollar transactions we have seen in other quarters

-

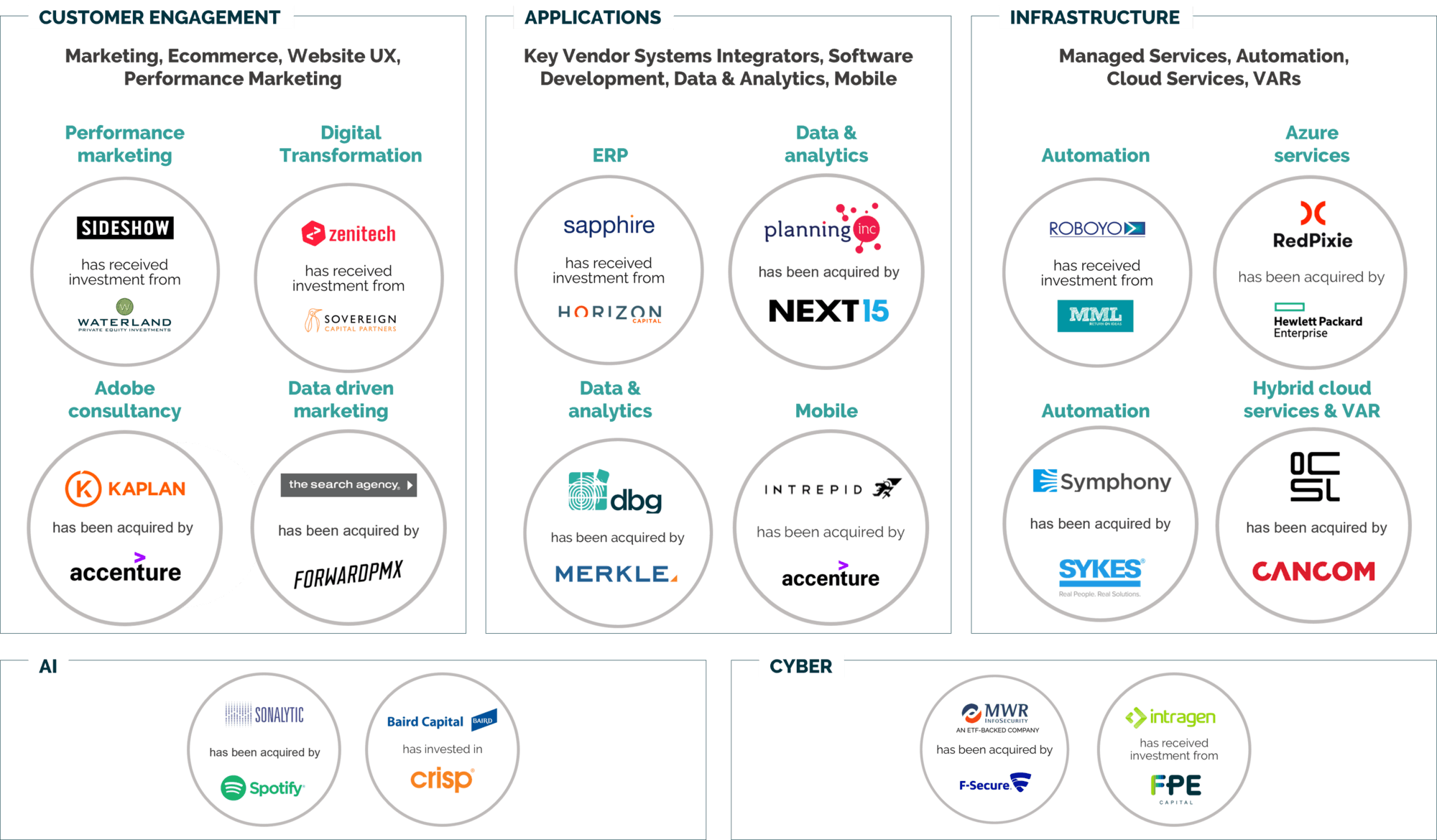

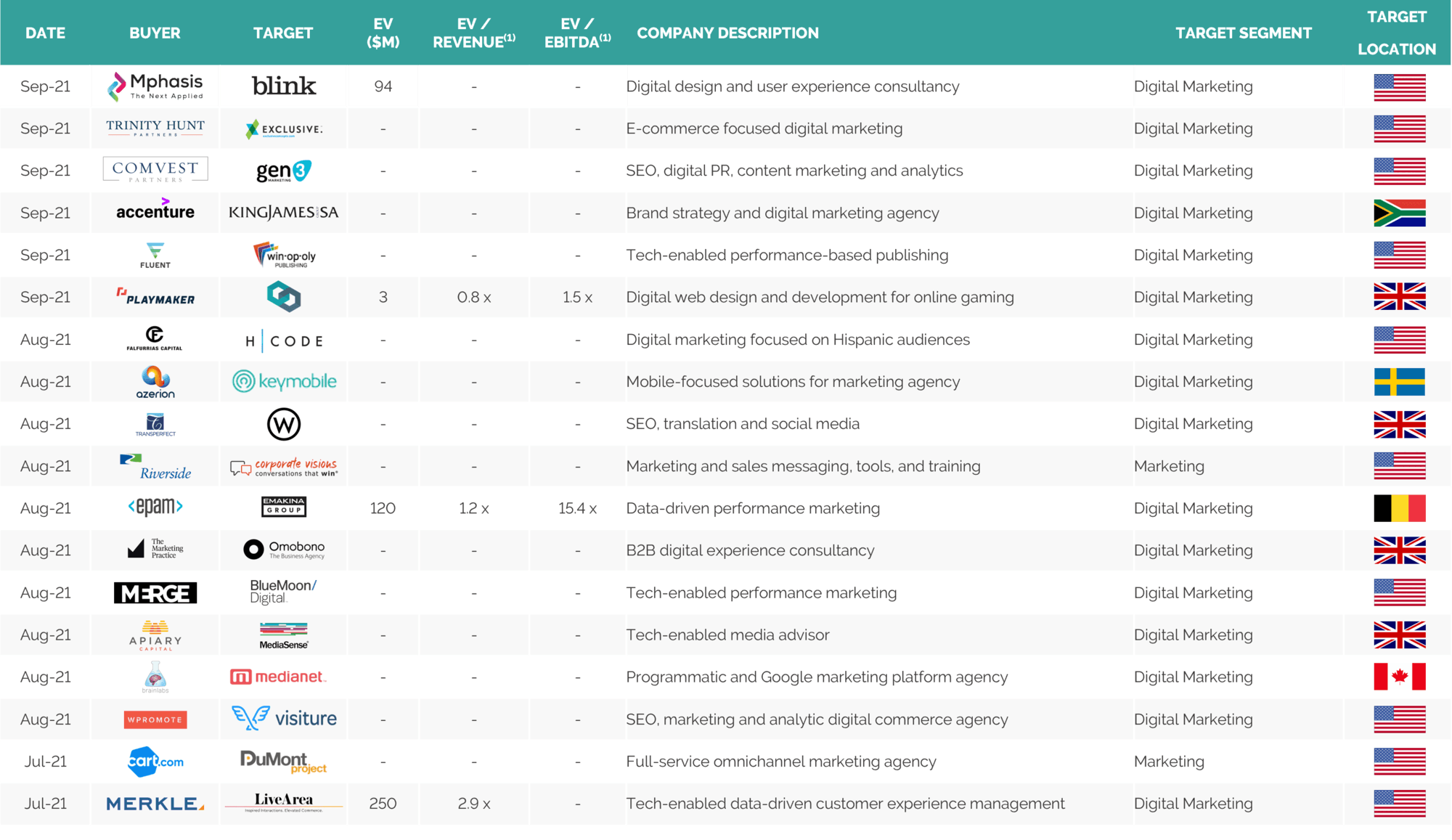

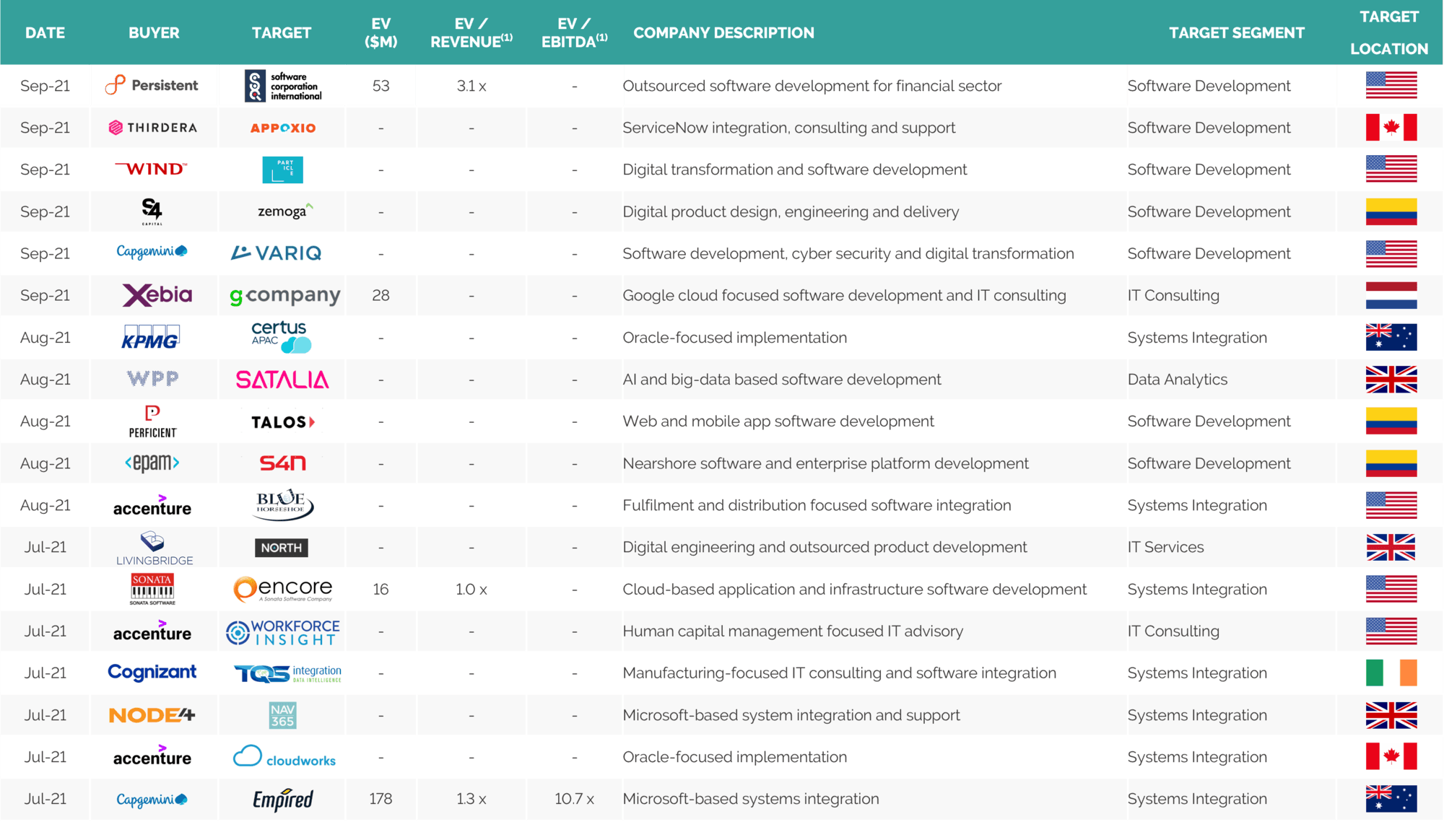

Digital acceleration continues to be pervasive throughout the third quarter, as demonstrated by S4 capital’s acquisition of Zemoga, a first step into tech services to offer clients an integrated solution covering marketing, sales and now IT, Capgemini’s acquisition of Empired, strengthening their end-to-end cloud and data capabilities to enable digital transformation for key industries, and Xebia’s acquisition of g-company, to expand its Google suite offering

-

Interestingly, this quarter we saw three acquisitions of nearshore software development capabilities in Columbia: Epam’s acquisition of S4N, Perficient’s acquisition of Talos Digital as well as S4 Capital’s acquisition of Zemoga detailed above; nearshoring is now seen to be the optimal delivery model, combining cost-effectiveness with proximity and real-time interactions, to deliver agile tech innovation

-

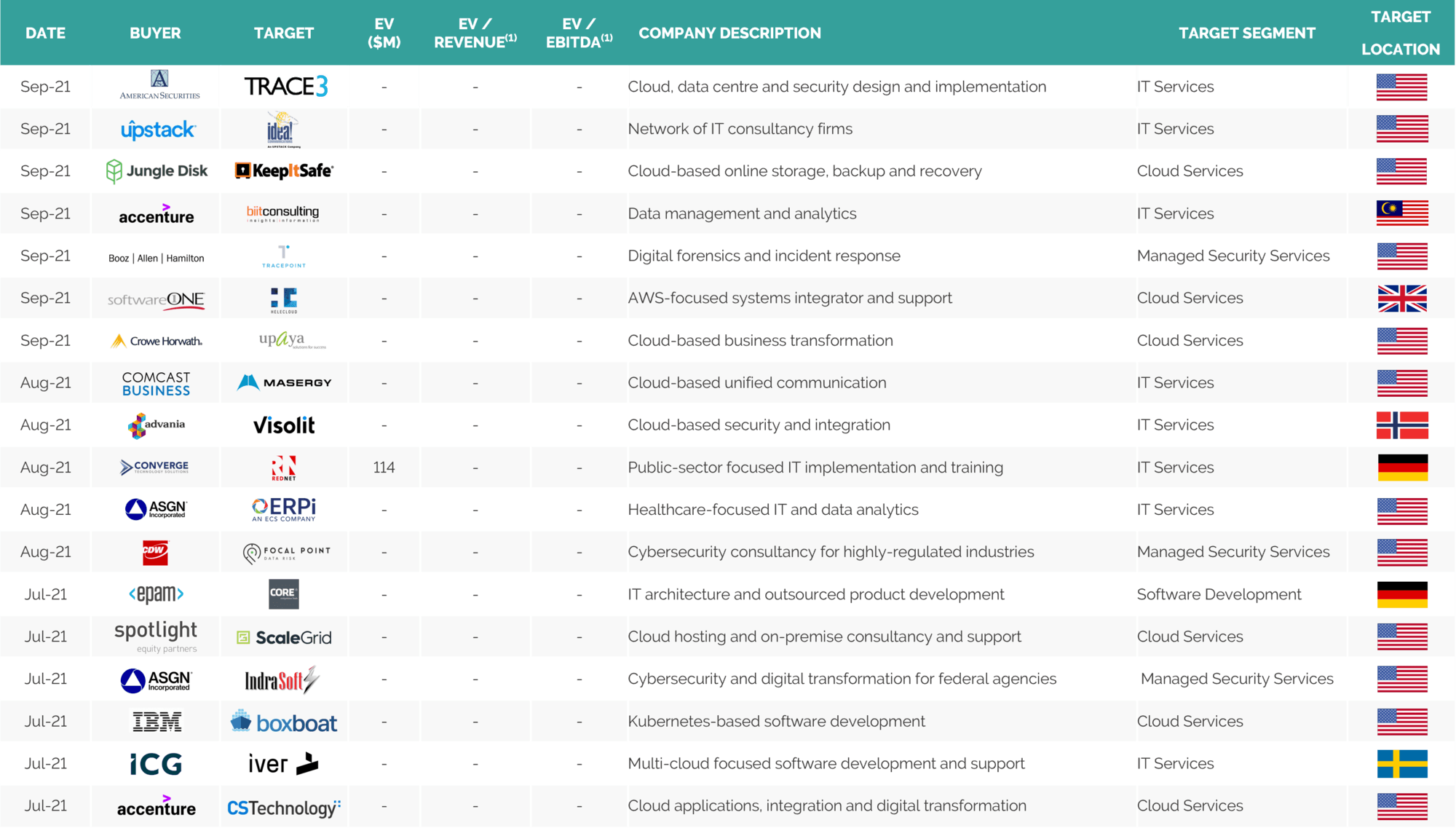

Elsewhere, IBM acquired BoxBoat, a Kubernetes-based software development consultancy, to continue its drive into the open-source software environment, whilst Accenture remains the most prolific acquiror across geographies and capabilities, with another 14 acquisitions this quarter

-

UK mid-market private equity continues to be active with Livingbridge’s acquisition of North, a provider of end-to-end networking and IoT solutions, and Apiary Capital’s acquisition of MediaSense, a tech-enabled media advisor