Technology services sector market review - Q1 2020

Welcome to the Q1 2020 edition of our Technology Services Perspective – Results International’s quarterly market update of the technology services sector. In the last 18 months, Results International has advised on high-value transactions across all of these disruptive subsectors (performance marketing, data & analytics, software development, automation, cloud services etc.).

The subsectors we track include (i) Customer Engagement (marketing & eCommerce, website UX and performance marketing), (ii) Applications (key vendor systems integrators, software development, data & analytics and mobile), (iii) Infrastructure (managed services, automation, cloud services and VARs), (iv) AI and (v) cybersecurity services. Separately, we cover the security software in our quarterly CyberScope which you can navigate to by clicking the button below.

Read the Cyberscope

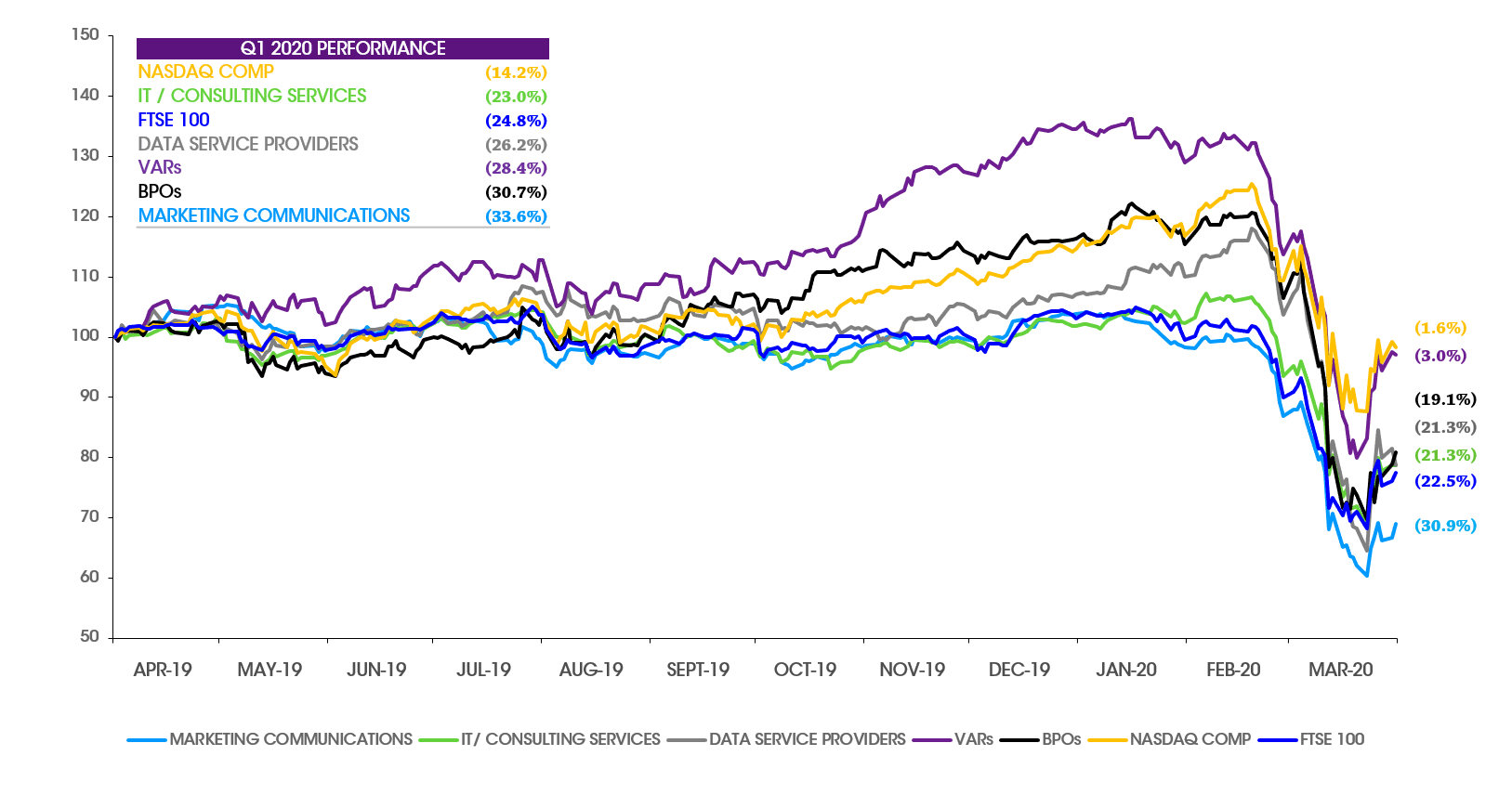

1. Covid-19 has had a short-term negative impact on the public market comps with stocks and valuations in the sectors that we track all down 25%+ in Q1; although all these indices have risen by 5%+ since the end of the quarter.

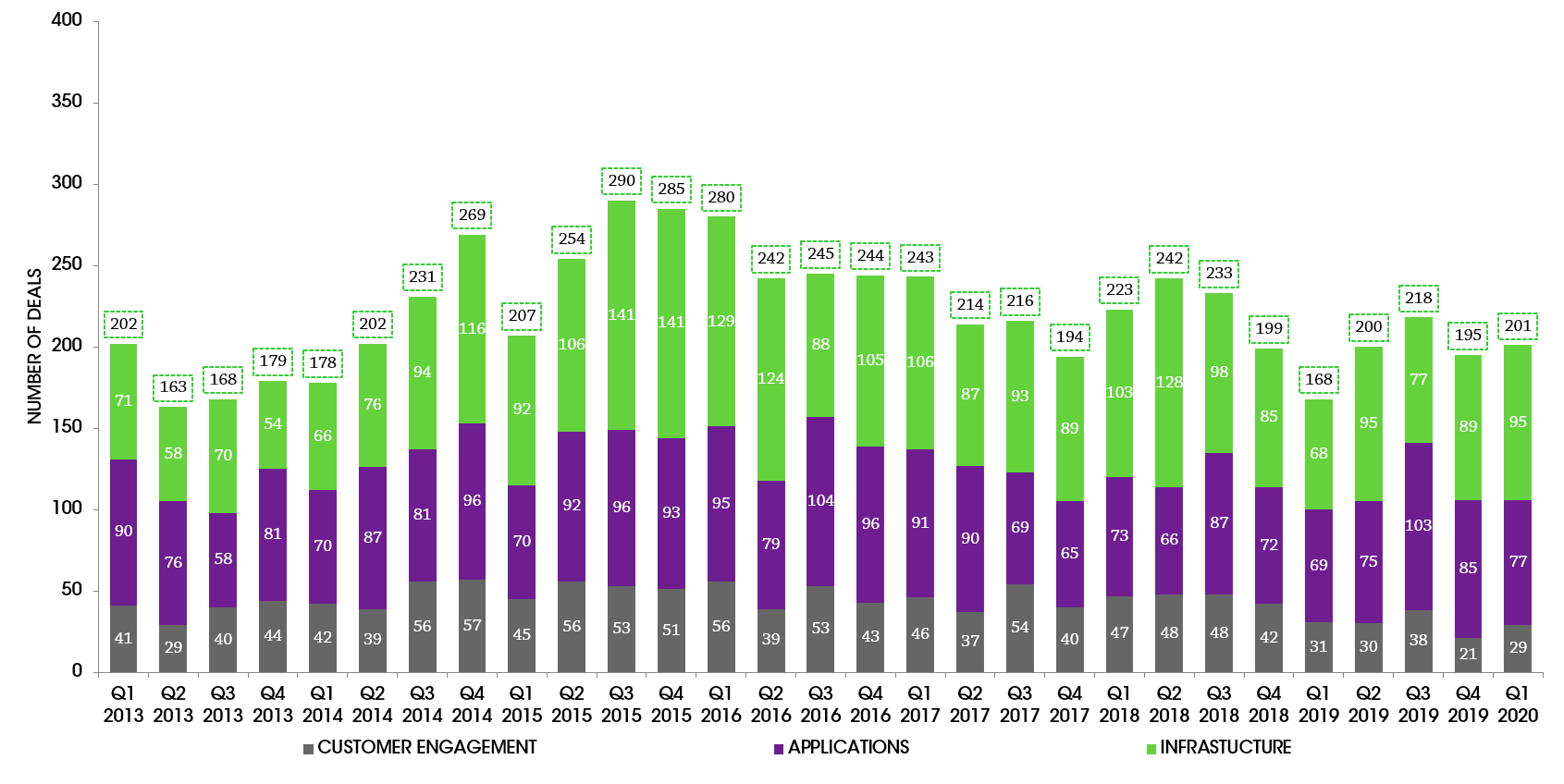

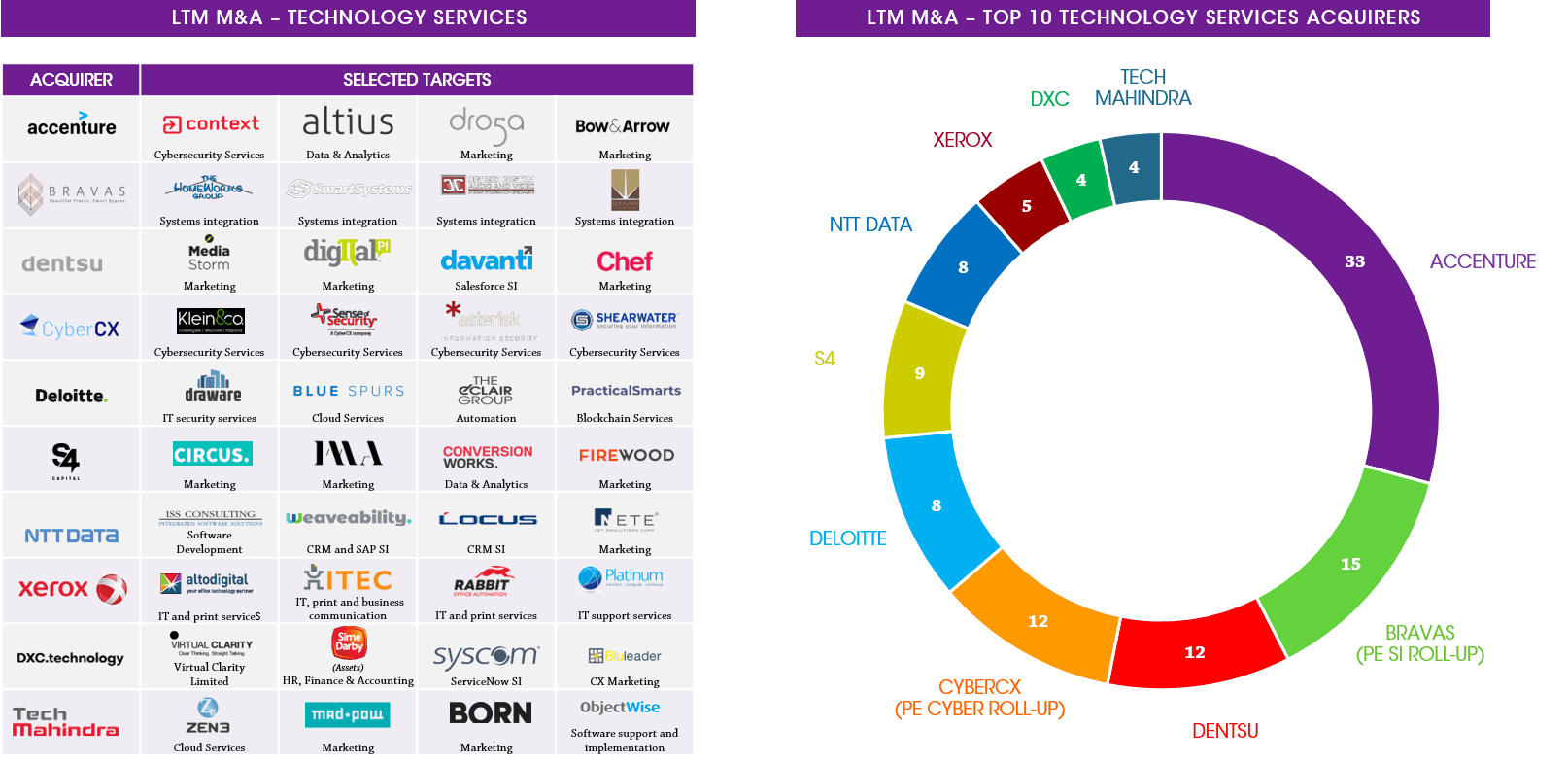

2. Conversely, deal activity does not yet seem to have been impacted, with volume up quarter on quarter to 201 and March being the largest single month with 71 transactions (April is on course for a similar number), even after the widespread outbreak of the virus. Although it should be pointed out of course that many of these transactions would have been well progressed before the pandemic. See overleaf for specific transactions of note.

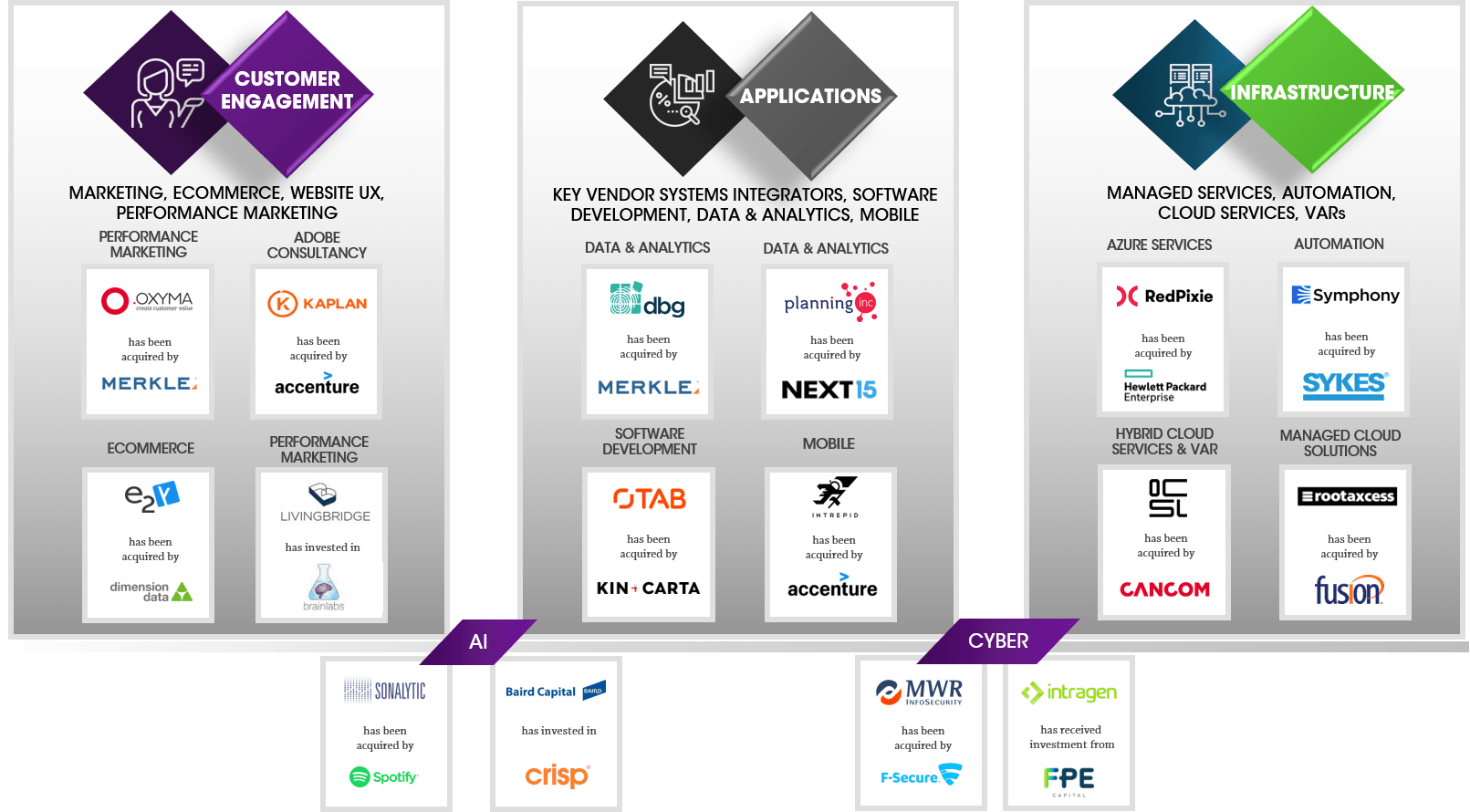

Company focus:

Accenture was once again the busiest, making nine acquisitions in the quarter adding capability across data analytics, cyber, ERP and Mulesoft systems integration. All reflecting its continued focus on high-growth, transformative areas across the technology services landscape.

Capgemini and Cognizant made a couple of acquisitions a piece with data analytics, digital marketing and Mulesoft capability once again featuring prominently. Given Mulesoft’s fundamental remit is to enable analytics and integration of data sources across multiple environments (on-premise, public cloud, hybrid cloud), this is the perfect example of the type of the business that will do very well with the current heightened focus on increasing digitisation and remote working.

1. We expect public markets to slowly recover and based on the financial crisis in 2008, this will take at least a couple of quarters.

2. There is likely to be some Covid-19 impact on M&A, but we believe that activity will bounce back strongly:

Despite current market turbulence, 2020 will remain a good year to contemplate fundraisings, exits or acquisitions in the technology service space. Please do get in touch to discuss.

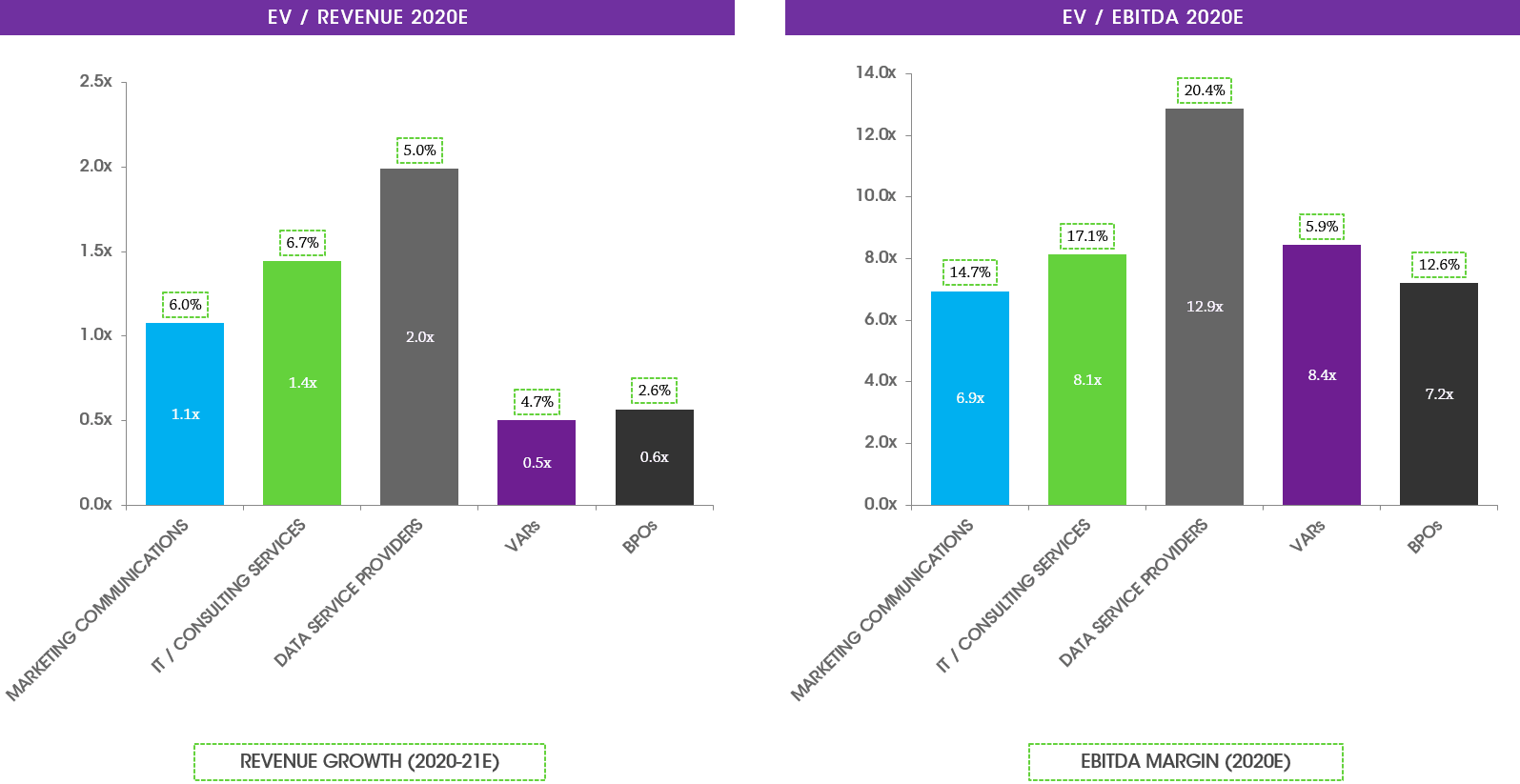

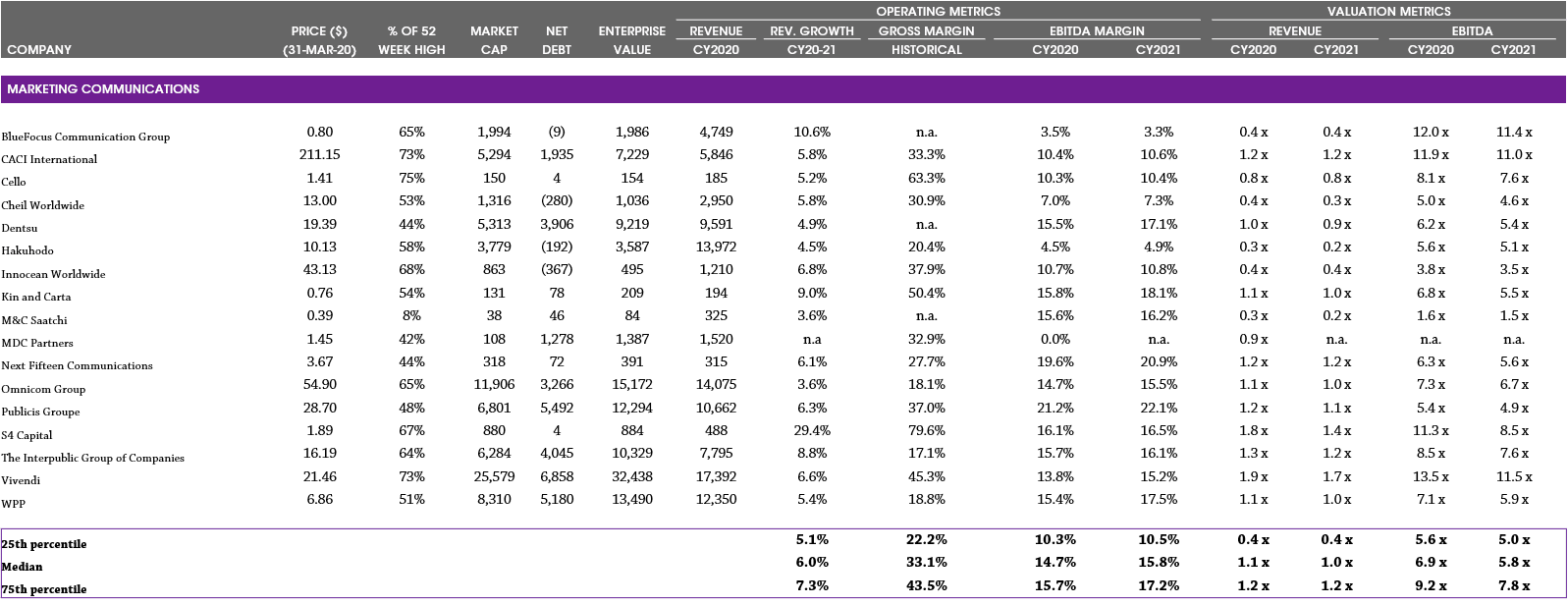

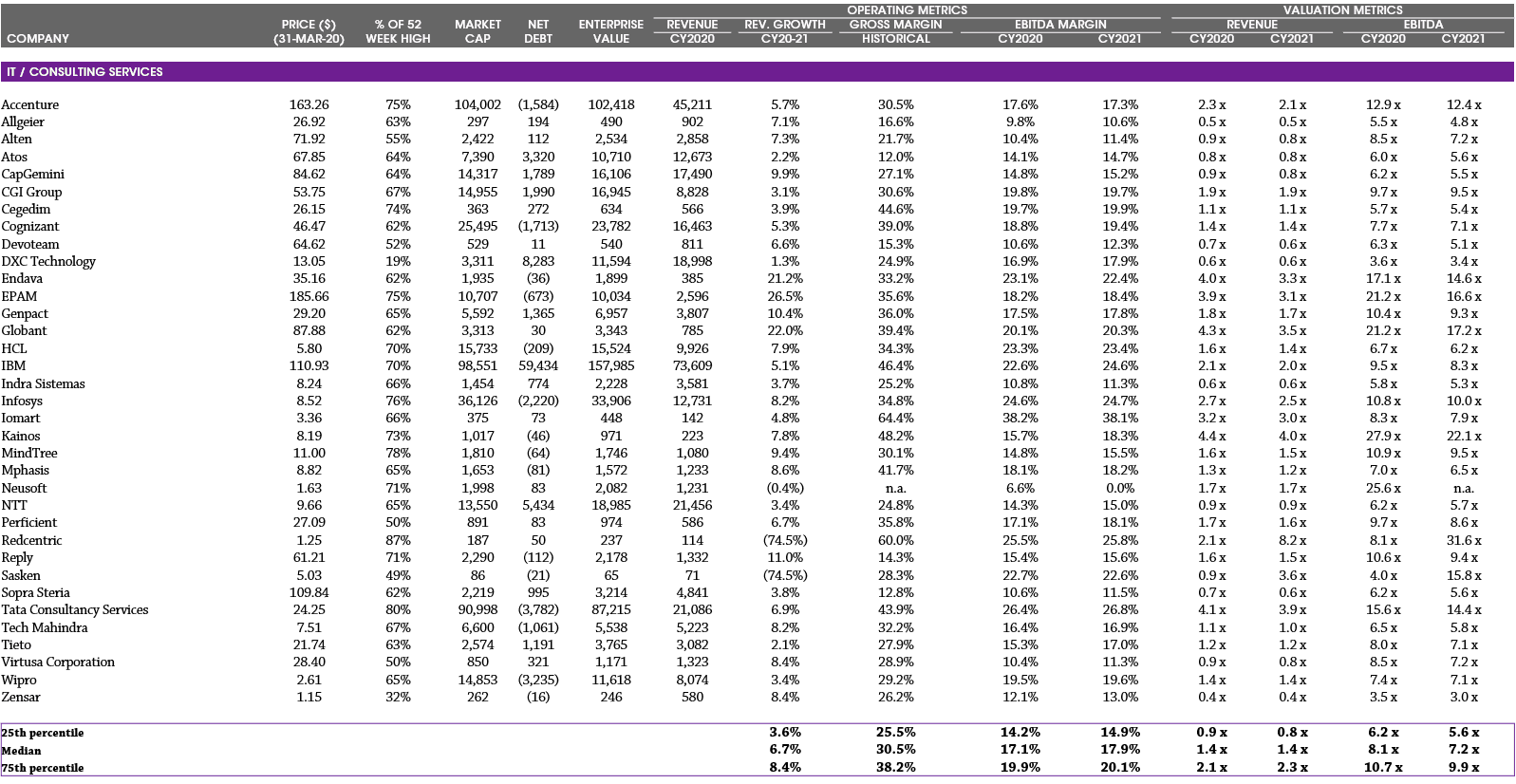

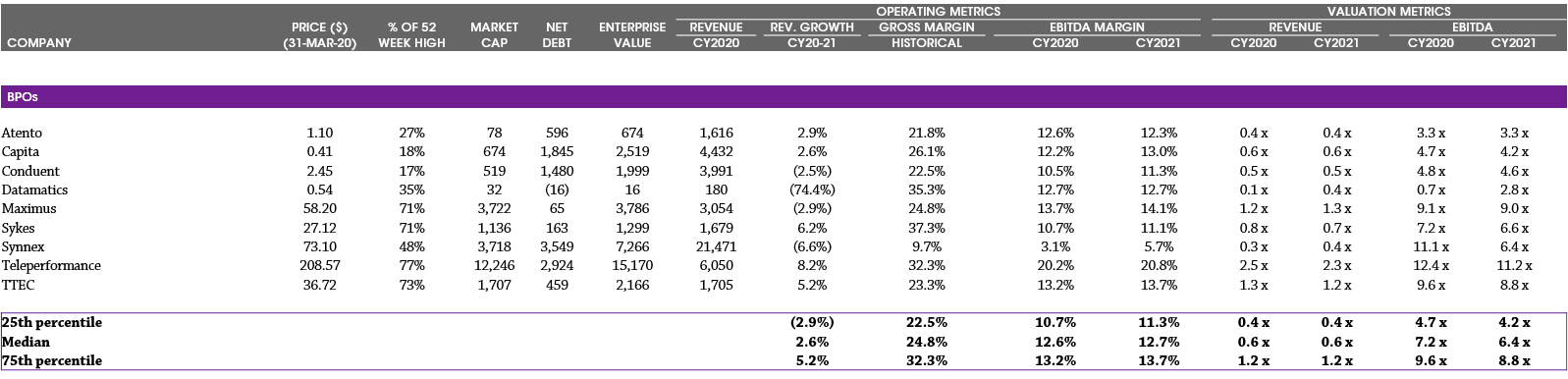

Note: EV = Enterprise Value; financials calendarised to December year end; median values reported. See the Selected Publicly Traded Companies section of this document for details of companies included in each category. Source: Capital IQ.

Notes: Based on share prices as at 31st March 2020; indices weighted by market capitalisation. Sources: Capital IQ and Results International analysis.

Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results International analysis.

Note: PE also shown as acquirer when acquisitions made through portfolio company; Parent also shown as acquirer when acquisition made through group subsidiary/ group. Sources: Press releases, Capital IQ, Mergermarket, 451 Research and Results International analysis.

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ.

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ. *Altran will delist once Capgemini acquisition completes.

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ.

Note: Calendarised to December year end; $ millions, except share price data; multiples capped at 20x EV / Revenue and 50x EV / EBITDA; net debt includes minority interest. Source: Capital IQ.