Trade buyers from across the services landscape are acquiring MSPs to expand their menu of services, increase market share and diversify revenue streams.

Unsurprisingly the most active group with a focus on adding scale and margin, broadening the service offering (particularly across Microsoft, cloud enablement and cyber) and becoming a one-stop shop and also diversifying the customer base through moving into new industry verticals and geographies/regions.

As ever with services companies, location and the end-customer market is important. For location, customers typically favouring proximity meaning that in the short-term geographical expansion can only really be achieved through acquisition. With regards to end-customer market, those companies focussed on the enterprise will still rarely if ever buy an MSP focusing on the SME market as the economics and sales commission model just do not work. Wipro for instance have tried and failed! Likewise, the same is true for the SME market

These drivers are all showcased in recent European M&A:

1. Accenture acquired Sentor (Jun-21) to enhance its enterprise managed security services in Sweden 2. TiG (backed by Business Growth Fund) acquired ThirdSpace (Mar-21) to add Microsoft managed security services to its mid-market portfolio 3. AirIT (backed by August Equity) acquired Oxford-based Riverbank IT Management and Coventry-based Nexus GS (both in Dec-20) as it continues to broaden its mid-market reach across the West Midlands and Thames Valley

Convergence between telecoms and IT services businesses has been a topic of industry discussion for quite some time and long before the pandemic.

For many years, Telcos have been grappling with the declining use of the handset and evolving their offering to include additional service lines such Microsoft 365 and cybersecurity meaning that the lines between what was traditionally seen as either a comms or IT services business have become blurred. Covid-19 and virtual working has of course accelerated this convergence even further and given customers are reluctant to have two suppliers, Telco Services providers need to offer the full suite of comms and cloud enablement services.

Telefonica is a good example of this, having launched its tech division in late 2019 to provide services across cybersecurity, cloud, IoT, big data and blockchain. The strategy is to grow this division both organically and through M&A and in July 2021 acquired Cancom, a German-based VAR and MSP, to bolster its cloud capabilities. Results had previously sold OCSL, a UK-based MSP, to Cancom to add more strategic services revenues to its VARs heritage.

Arrow, backed by MML Capital, with a heritage in unified comms has also used M&A in recent years to broaden its service offering to include IT services. Acquisitions have included AIMES Management Services (Sep-21) to add hosting, backup and colocation services and Click Networks (Sep-20) to add Microsoft cloud capability and Scotland.

Really one about revenue model and providing end-to-end services across the digital transformation ecosystem.

Project services businesses with lumpier time and materials and fixed price models often long for more predictable recurring revenue streams. Likewise it makes sense for IT Consultancies who have close relationships with the C-suite, and therefore budget influence, to own more of the customer journey and increase wallet share.

Indeed, the ANS and UKFast merger, which was announced in Oct-21, is testament to this with the combination bringing together the more strategic components of ANS’ offering, namely public cloud, digital go-to-market and Microsoft, with UKFast’s private cloud and hosting heritage. Both ANS and UKFast were majority controlled by Inflexion Private Equity, and the merged entity will carry the ANS name and become one of the UK’s leading independent digital transformation businesses.

The adage of how do you maximise lifetime value from your very large customer base? You move upstream and at the same time cross-sell stickier and more strategic revenues. Ultima have been on this journey since taking money from APSE capital in 2019 and is now intent on becoming a next-gen MSP focussed on three core propositions – cloud, security and digital. The acquisition of Just After Midnight, in Mar-21, is crucial to Ultima’s cloud-play in adding strong Azure and AWS capabilities and global 24/7 support.

The MSP space remains a highly attractive investment opportunity: predictable recurring revenue streams, meaningful whitespace with many SMEs in particular still yet to outsource their IT, high fragmentation to drive returns from a buy & build consolidation play, and then clear tangible benefits of scale from combining a fixed cost base and supplier pricing agreements.

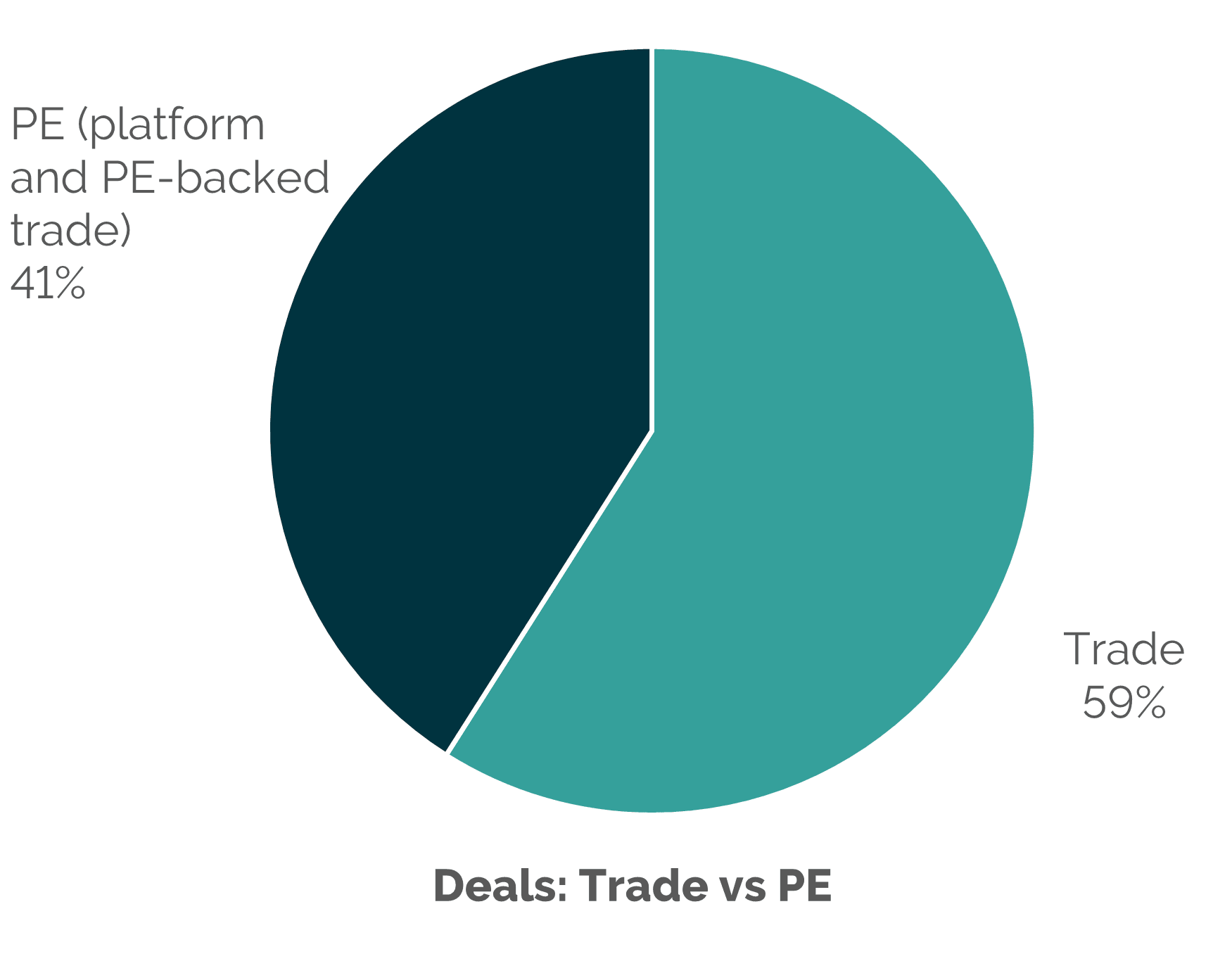

All this is borne out through the numbers – 41% of all deals in the space since 2018 have either been acquisitions directly by PE or bolt-ons through existing portfolio companies. Indeed, a PE-backed acquisition can present an interesting hybrid with the ability to both share in any future upside but also benefit from the inevitable synergies from a larger platform.

So, all in all multiple options with all trade buyers offering something slightly different. The key considerations will be a factor of: Is the culture aligned? Is the strategy aligned? What will be the future role of the management team? What is the M&A track record?

At Results, we pride ourselves in maximising the options that meet shareholder objectives and then constructing a process that finds the very best home for the business at the very best price and we would generally always recommend including private equity (PE) as well.

Investors are increasingly a match for their trade counterparts on price and will always help build competitive tension. Also, if you want to retain some control and share in any future upside, then PE will certainly be the preferred route.

Notable recent European PE deals include:

Livingbridge’s investment into managed cybersecurity business Quorum (Jan-22); Results supported Livingbridge on this transaction

Palatine’s investment into UK-based MSP Fournet (Jun-21)

Providence’s investment into UK-based hosting provider Node4 (Mar-21). Node4 then subsequently bought Dynamics consultancy The Nav People (Jul-21) to add strategic Microsoft capability to the group