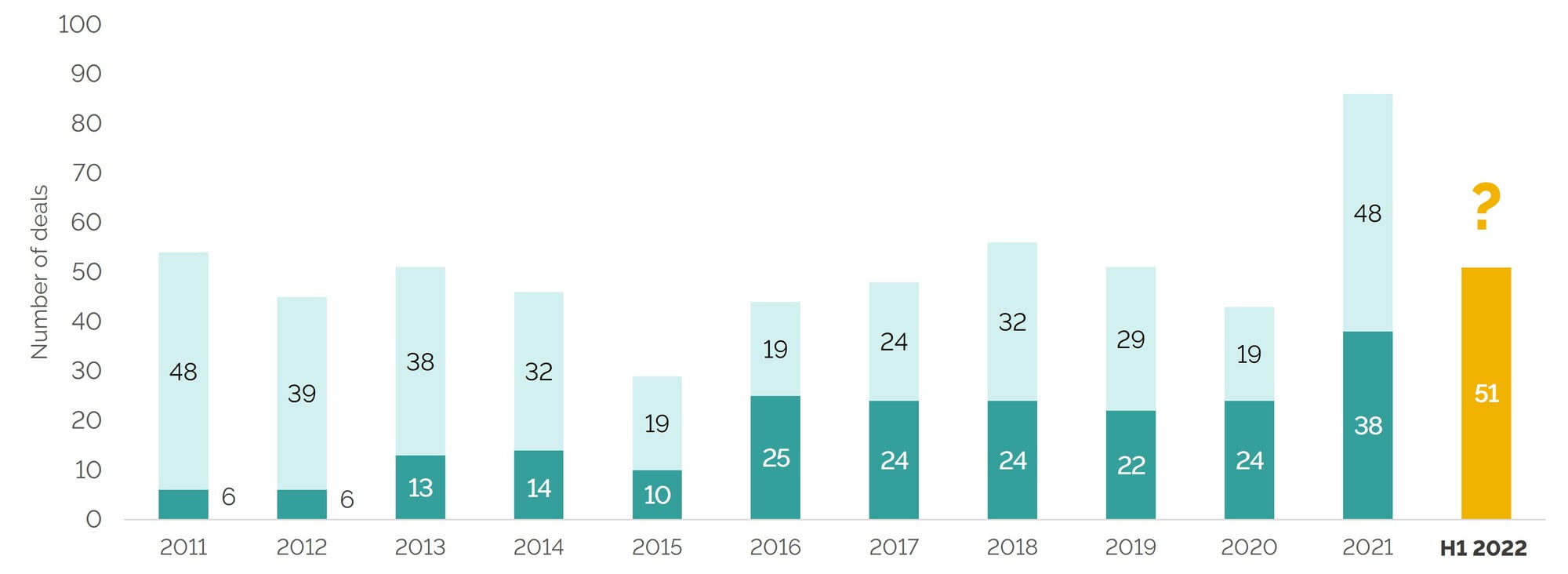

The landmark increase in deal flow seen in 2021 continued through into H1 2022

There was a significant increase in deal volumes in H1 2022 vs. the same period in 2021

Whether this momentum will continue through to the end of 2022 remains to be seen…

Sources: Results analysis, CapitalIQ, Mergermarket

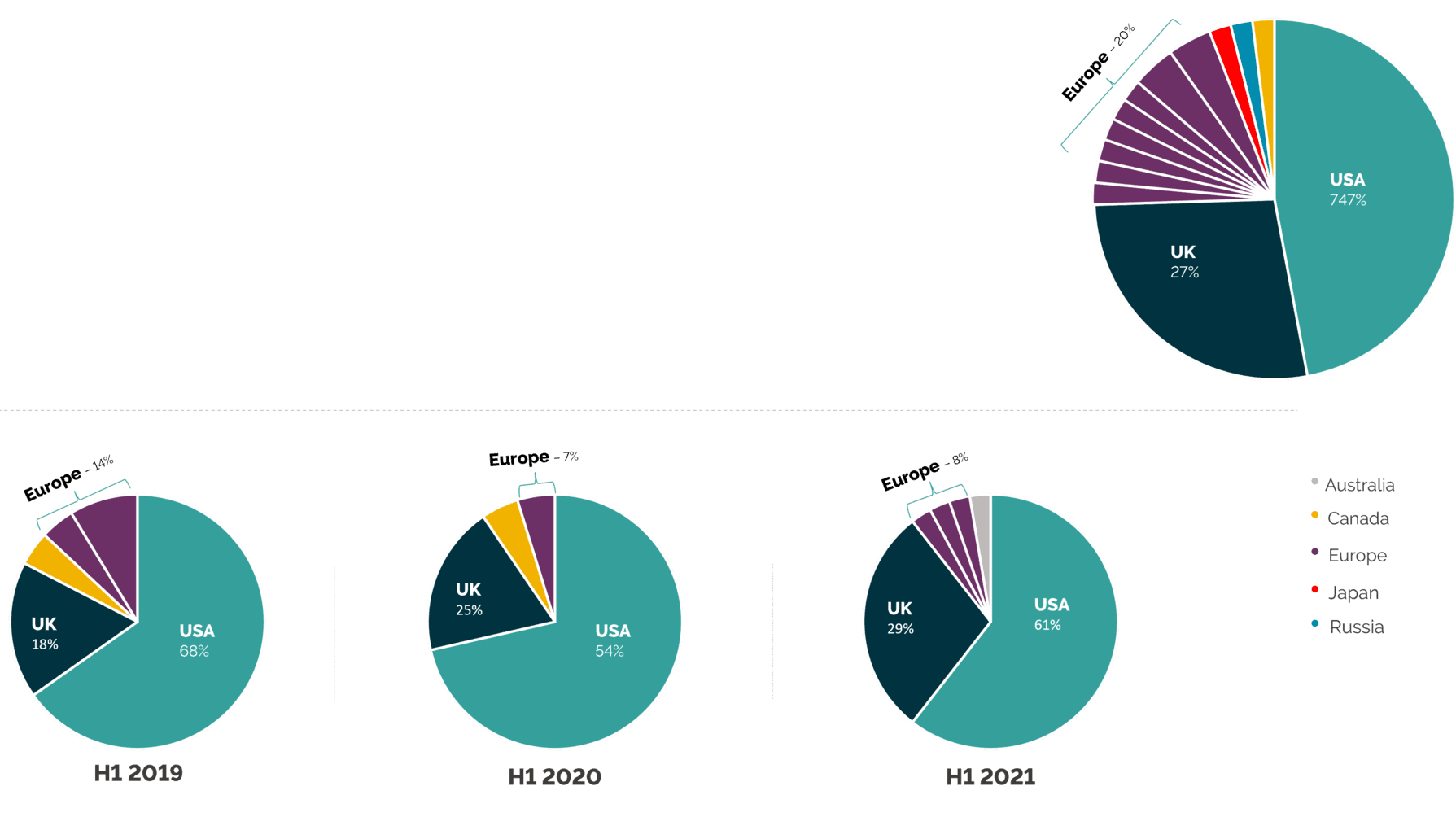

There was a noticeable shift in the geographic distribution of deals that took place in H1 2022, vs. the same period in previous years

The US accounted for a significantly smaller percentage of deals than usual - down below 50% for the first time in a decade

Europe saw the largest growth in deal activity, up almost three times what it was in H1 2021

Despite the macroeconomic backdrop, the % of deals done in the UK was largely consistent with the previous two years

Sources: Results analysis, CapitalIQ, Mergermarket.

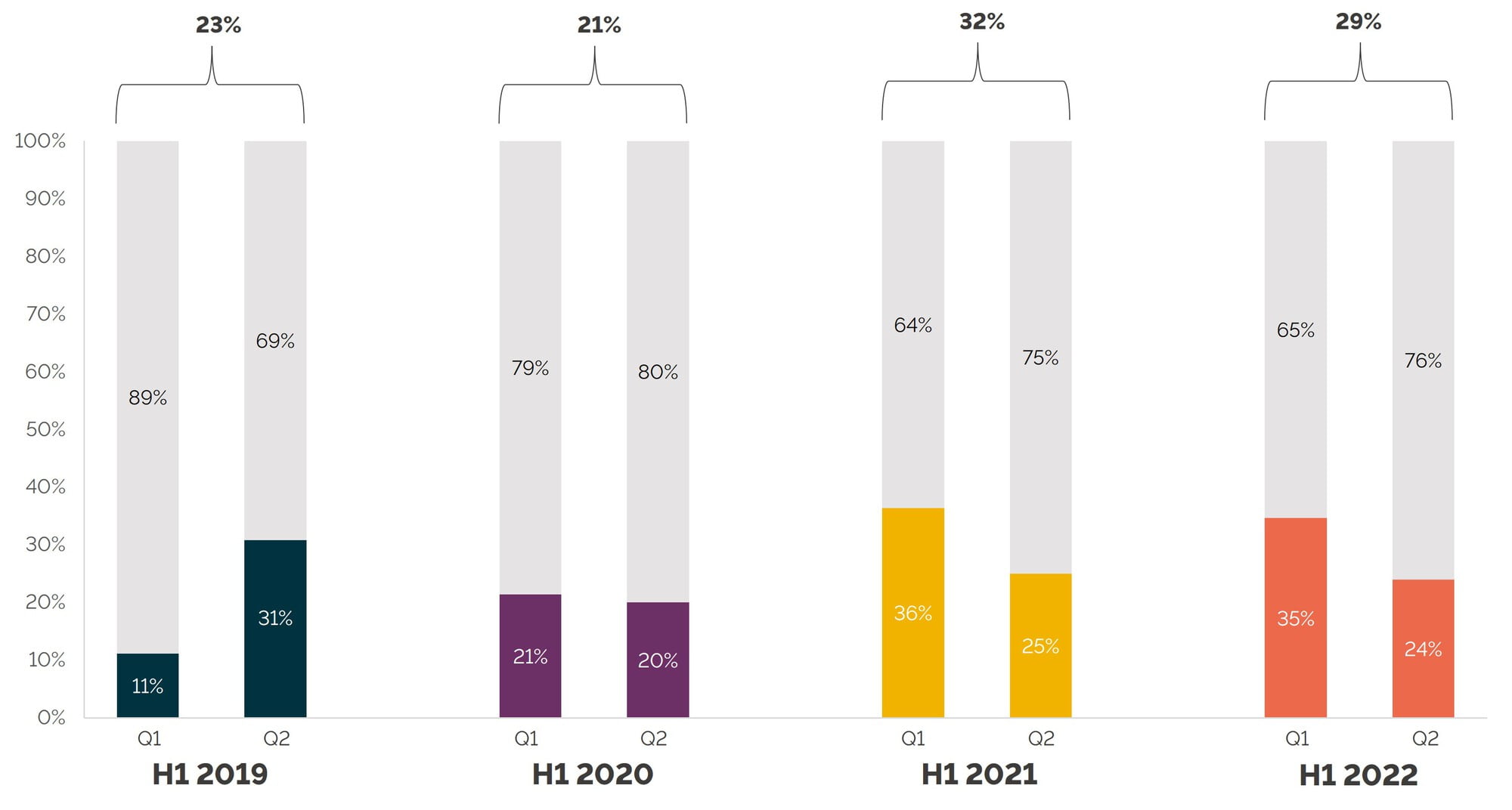

Interest among PE within the Pharma Commercialisation Services sector remained elevated in H1 2022, with PE deal activity levels in line with H1 2021 and FY2021 – at 29%

Whilst we initially attributed this elevation to delayed activity and post-COVID bounce backs, figures would suggest that PE’s interest in Pharma Commercialisation Services is lasting, much like the wider healthcare sector

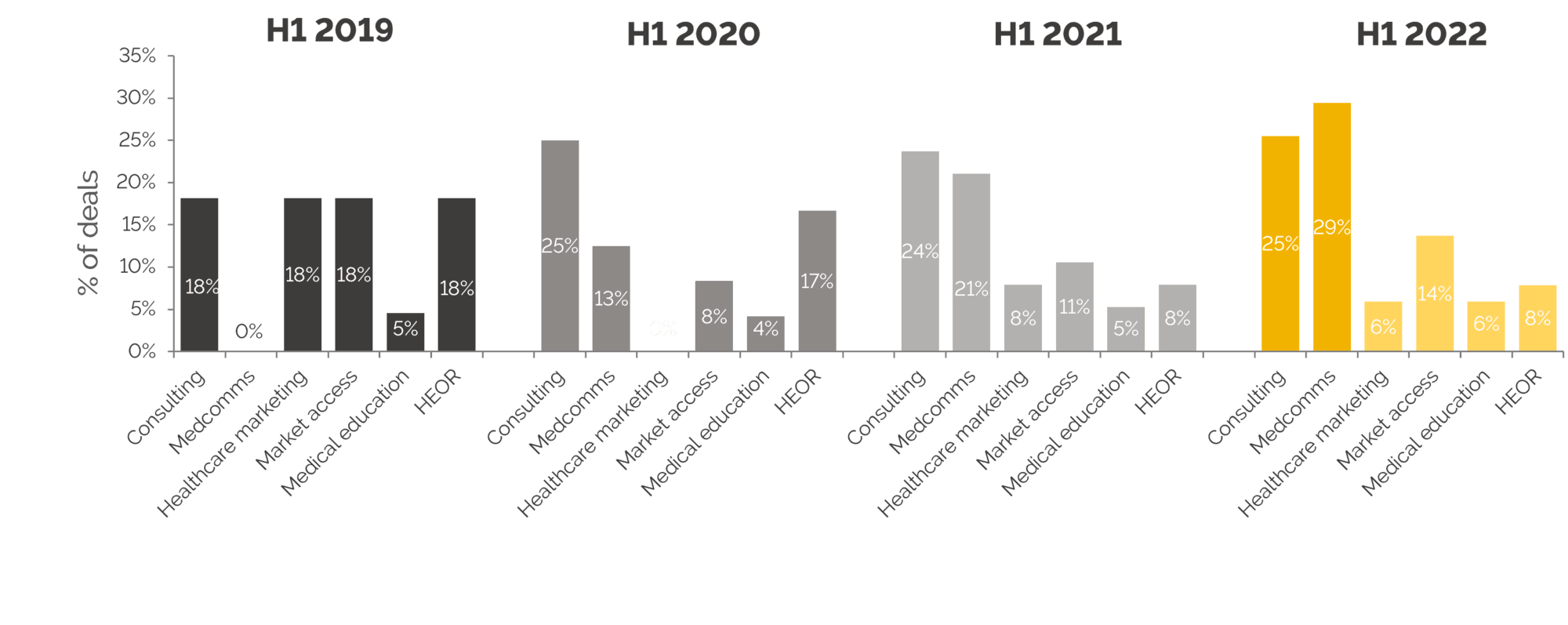

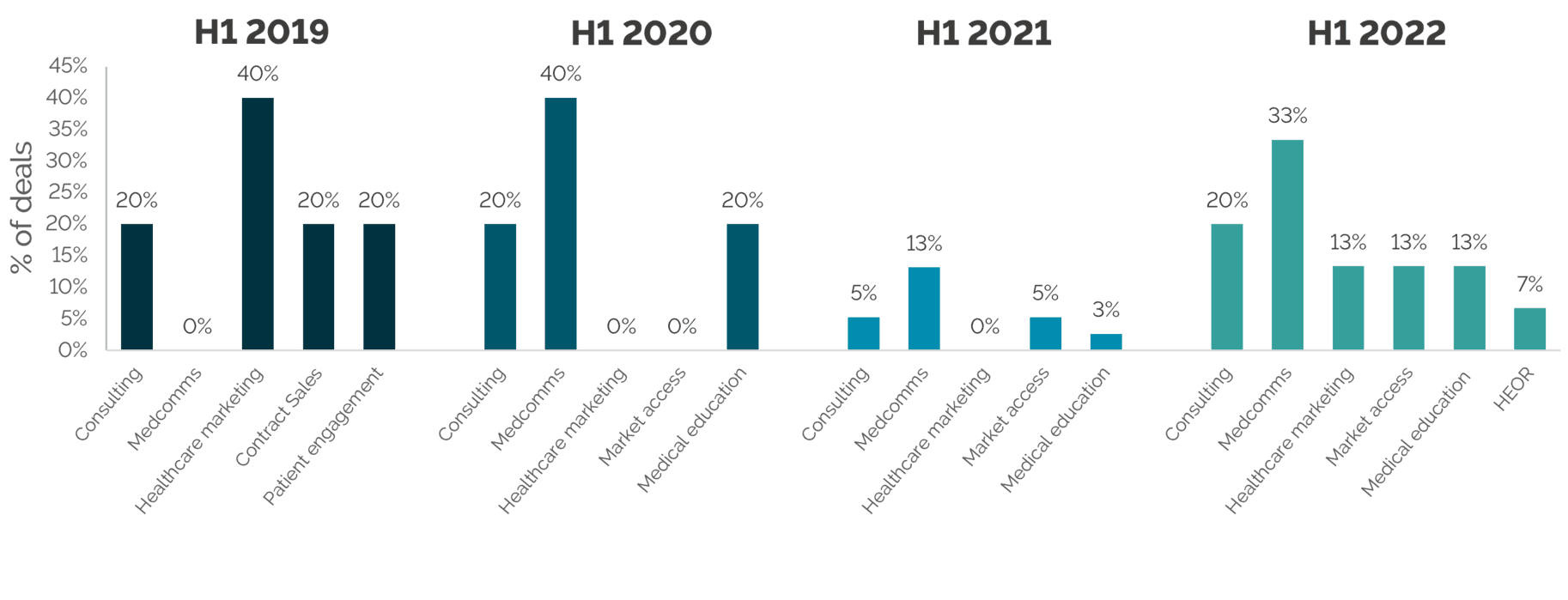

In line with H1 2021, Consulting and Medcomms were the most active sub-sectors in H1 2022, and the proportional spread across other sub-sectors was largely similar too

Similarly, Medcomms was the dominating sub-sector amongst PE in 2022 – in line with the trend of the last few years, even if exact proportions have varied

Market access: Pricing reimbursement market access HEOR: Health economics and outcomes research Sources: Results analysis, CapitalIQ, Mergermarket

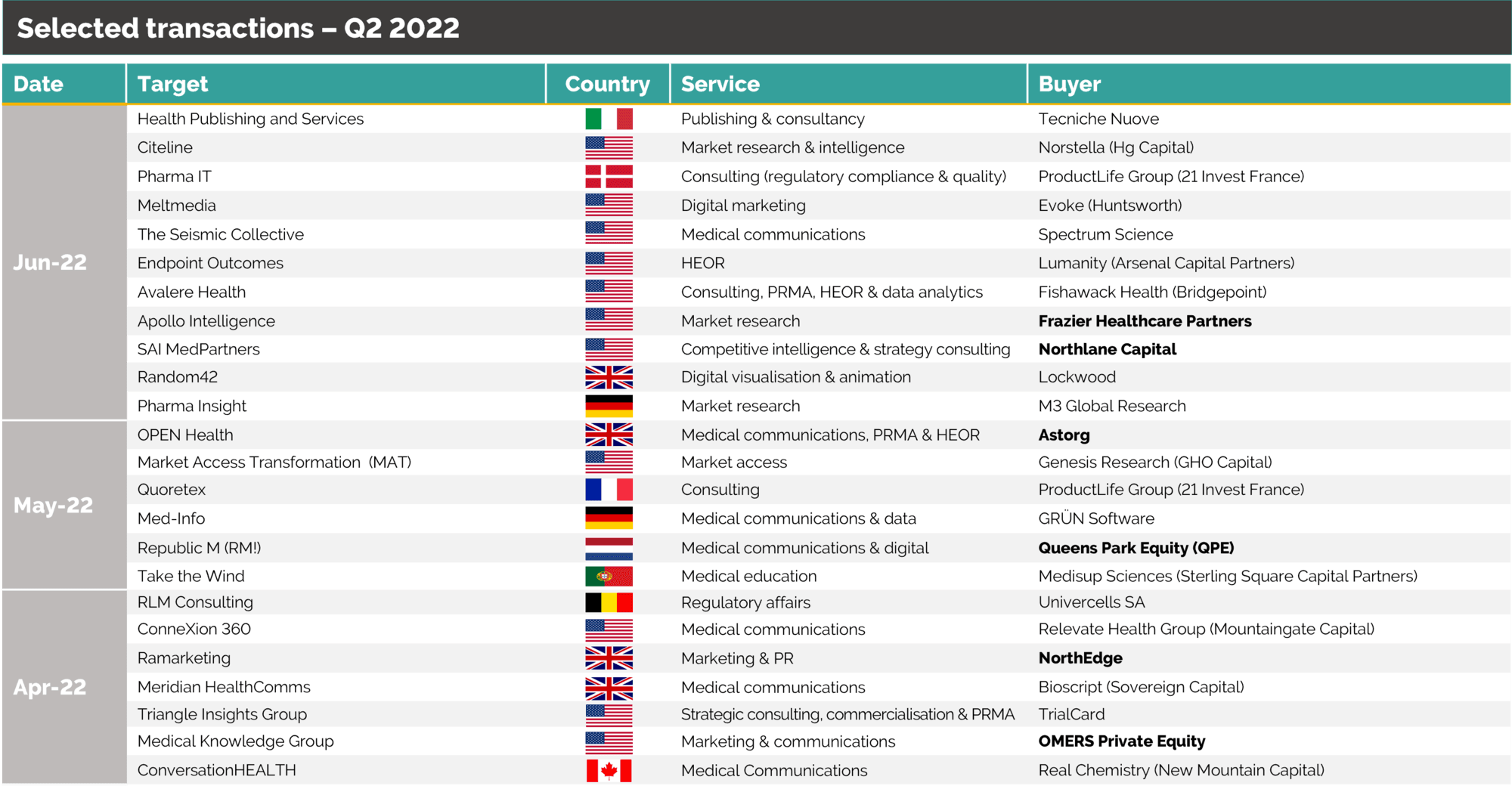

Companies in bold represent private equity firms Sources: Public data, CapitalIQ, Mergermarket = only publicly disclosed deals are shown

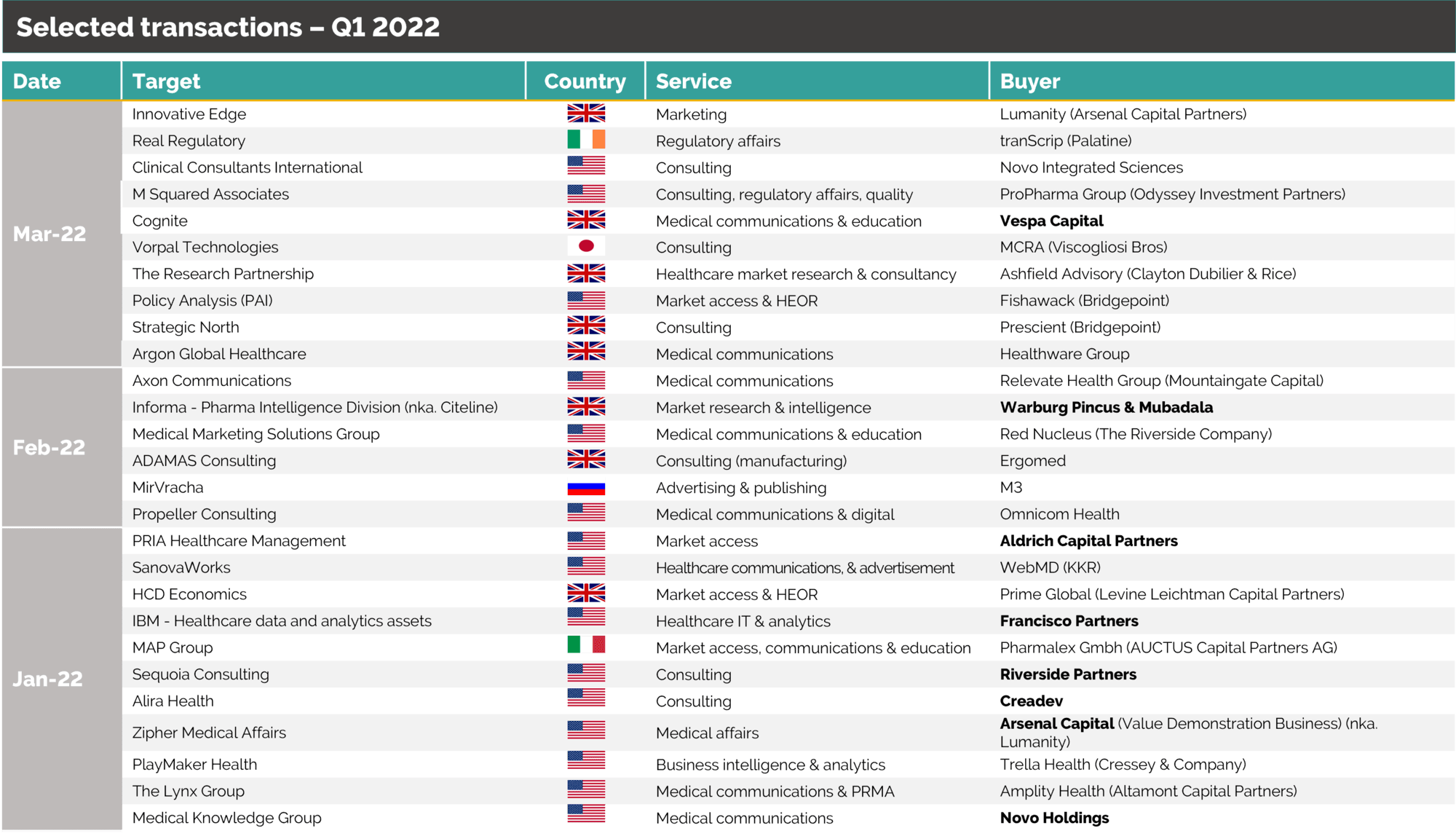

Companies in bold represent private equity firms Sources: Public data, CapitalIQ, Mergermarket = only publicly disclosed deals are show